Managing retirement budgeting requires shifting your focus toward strategic price comparisons, ensuring your fixed income covers everyday necessities while preserving your desired lifestyle. By evaluating ten specific household expenses, you can immediately capture savings that stretch your monthly paycheck further than you might expect. When you transition from a regular salary to a fixed pension or Social Security check, inflation often erodes your purchasing power faster than your income adjusts. Taking a few extra minutes to compare prices for groceries, medications, and insurance policies transforms a stressful financial situation into a comfortable retirement. Stop accepting the first price tag you see and start treating your consumer choices as a powerful tool for safeguarding your hard-earned financial independence.

The State of Your Retirement Wallet

Stepping away from the workforce radically alters how you interact with money. While you were building your career, a surprise expense or a price hike at the supermarket could often be absorbed by an upcoming bonus, a raise, or a few extra hours on the clock. Today, your income parameters are rigidly defined. You are drawing from a finite pool of resources, meaning every dollar spent on overpriced necessities is a dollar stolen from your leisure, travel, or legacy goals.

Recent data underscores the urgency of proactive spending management. According to annual spending averages from the Bureau of Labor Statistics, consumer units headed by someone aged 65 or older spend over $61,000 annually. Meanwhile, separate annual findings released by the Federal Reserve on household economic well-being reveal that a vast majority of adults nearing retirement feel anxious about their financial trajectory. Only about 35 percent of non-retirees believe their retirement savings are on track. This widespread uncertainty highlights a critical reality for middle-income households: you cannot control the macroeconomic forces driving inflation, but you have absolute control over where and how you spend your monthly budget.

Adopting a diligent comparison strategy bridges the gap between financial anxiety and lasting comfort. You do not have to sacrifice the quality of your life or retreat into extreme frugality. Instead, optimizing your budget requires a systematic review of your largest and most frequent expenses. By identifying the specific consumer categories where loyalty penalties and hidden markups thrive, you can reclaim thousands of dollars each year.

Strategy Pillar 1: Reassessing Your Daily Necessities

Your first opportunity to recapture cash flow lives right inside your home. Daily necessities represent a massive portion of the average retirement budget, and these frequent, seemingly small transactions compound rapidly over a calendar year. Performing a routine cash-flow audit on your household staples reveals exact patterns where convenience might be costing you a premium. By challenging your habitual shopping routines, you can uncover immediate savings without altering your dietary preferences or living standards.

Grocery Staples and Bulk Purchases

Supermarkets engineer their floor plans and pricing models to maximize impulse buys and brand loyalty, often at your expense. When purchasing pantry staples like rice, pasta, canned goods, and coffee, the price variations between local grocery chains, warehouse clubs, and discount retailers can be staggering. You must compare the unit price rather than the retail price; looking at the cost per ounce or per hundred sheets exposes the true value of an item. Switching your primary grocery run to a more competitive retailer—or intentionally purchasing non-perishable staples in bulk—lowers your average weekly grocery bill significantly.

Household Maintenance and Cleaning Supplies

Cleaning supplies, laundry detergents, and paper products are infamous for their high profit margins. Name-brand chemical cleaners rely on heavy marketing budgets, passing those advertising costs directly to the consumer. Comparing prices for these items across different platforms, including online delivery services and big-box stores, routinely uncovers massive discrepancies. Store brands utilize nearly identical chemical formulations to their premium counterparts, yet they sell for a fraction of the cost. Evaluating these products objectively allows you to stock your utility closet without draining your checking account.

Pet Care and Nutrition

Your furry companions bring immeasurable joy to your retirement years, but their upkeep can quietly devour your budget. Pet food, treats, and veterinary medications fluctuate wildly in price depending on the retailer. Many seniors blindly purchase these items from their local veterinarian or a boutique pet store, completely unaware that major online pet pharmacies and warehouse clubs offer identical brands at steep discounts. Establishing a habit of comparing prices for specialized kibble or recurring flea treatments prevents you from overpaying for your pet’s health and happiness.

Strategy Pillar 2: Optimizing Health and Wellness Expenses

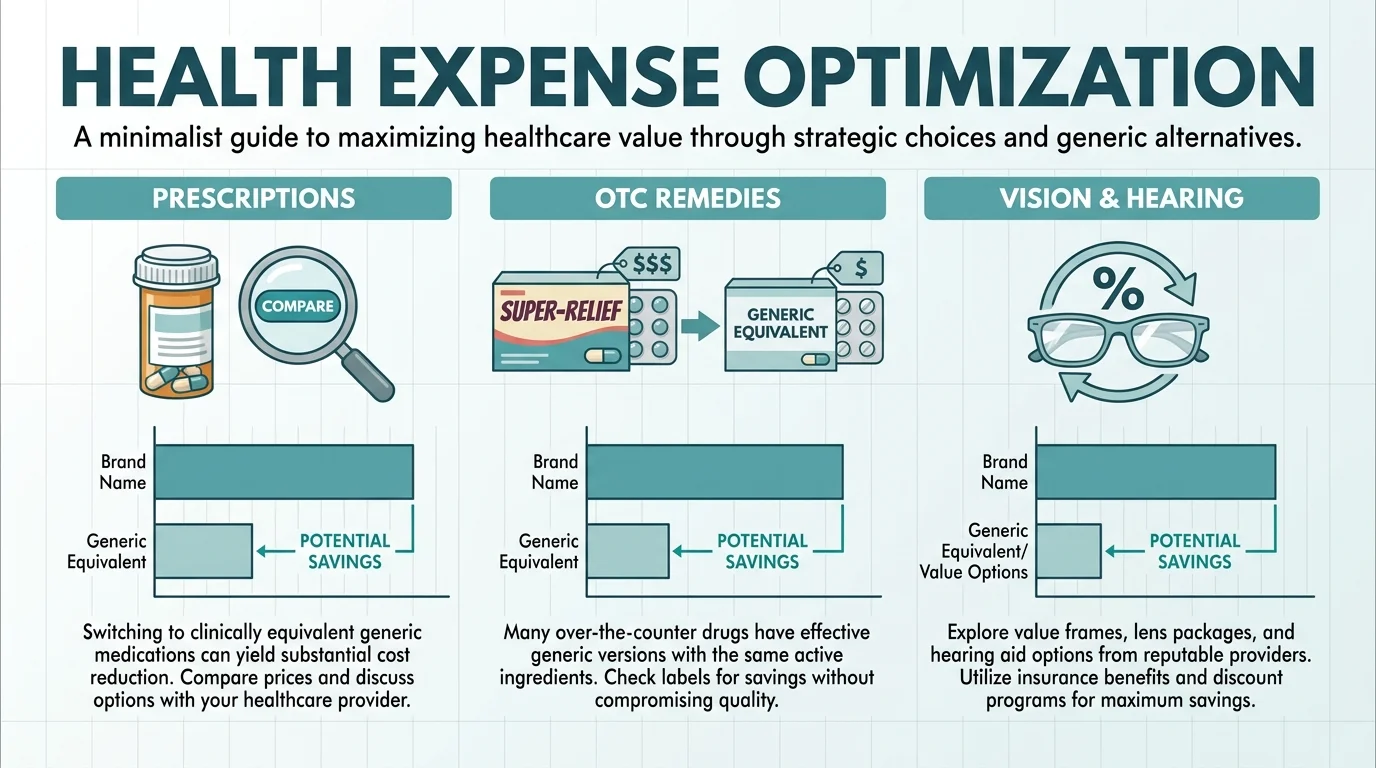

Healthcare costs consistently rank as the top financial concern for retirees. Even with robust Medicare coverage, out-of-pocket expenses for prescriptions, supplements, and wellness devices quickly accumulate. Treating your healthcare logistics with the same scrutiny you apply to buying a car or a home appliance is a vital component of smart shopping for seniors. You must advocate for your own wallet in a medical marketplace that rarely advertises its cheapest options.

Prescription Medications

The cost of a single prescription can vary by hundreds of dollars between pharmacies located just miles apart. Utilizing digital tools to compare prices before you hand your script to a pharmacist is no longer optional; it is a financial necessity. Furthermore, taking advantage of official Medicare plan comparison tools during the annual open enrollment period ensures your specific formulary is covered at the lowest possible premium. Always ask your physician if a generic alternative exists, as generics undergo strict regulatory scrutiny to guarantee they perform exactly like the costly name brands.

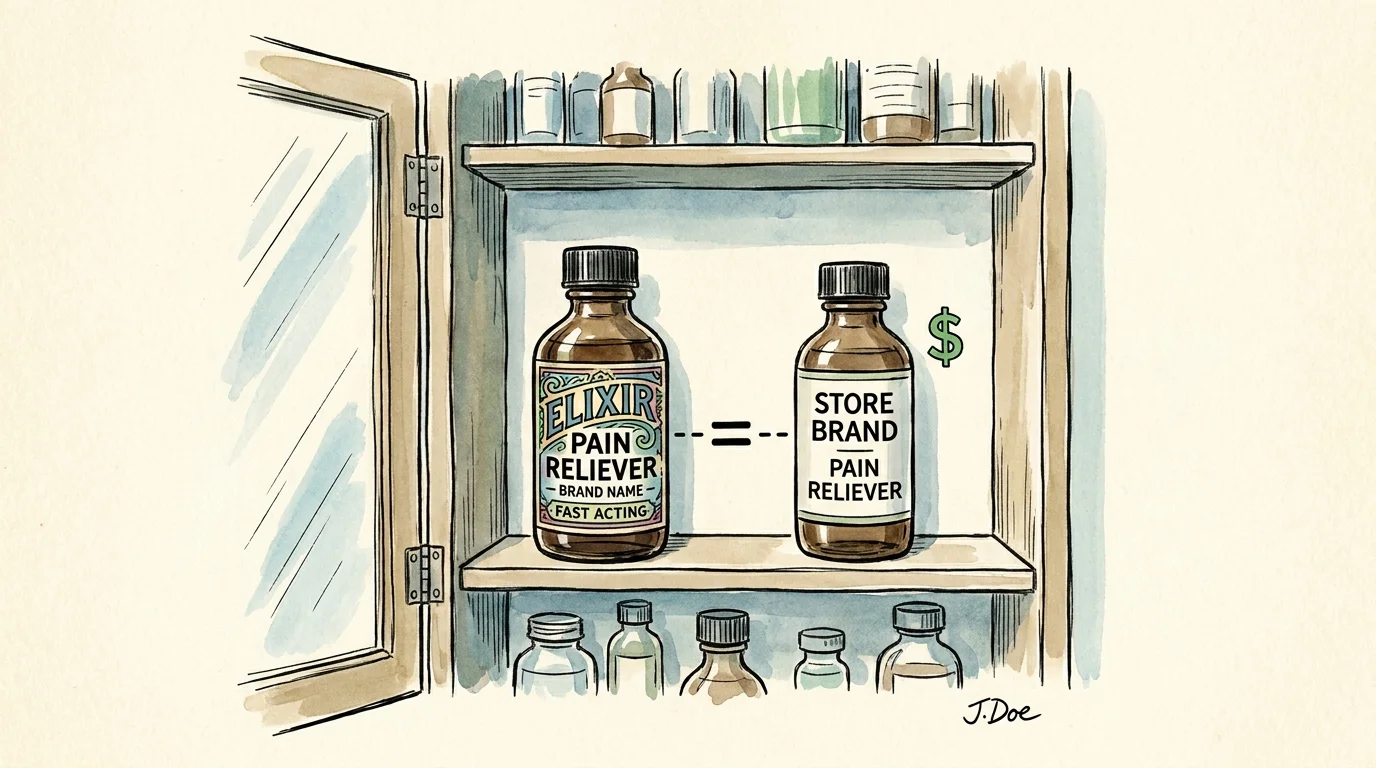

Over-the-Counter Remedies

A stroll down the pharmacy aisle presents you with a dizzying array of pain relievers, allergy medications, and digestive aids. Pharmaceutical companies design flashy packaging to convince you that their specific pill acts faster or works better. However, federal regulations mandate that store-brand over-the-counter medications contain the exact same active ingredients in the exact same dosages as the expensive national brands. Comparing the active ingredient labels rather than the colorful boxes empowers you to pay for the actual medicine rather than the marketing campaign.

Vision and Hearing Gear

Historically, seniors were forced to purchase eyeglasses and hearing aids directly through an audiologist or optometrist, paying massive retail markups in the process. The modern marketplace has fundamentally disrupted this model. Direct-to-consumer websites now offer high-quality prescription eyewear and FDA-approved hearing aids for significantly less than traditional brick-and-mortar clinics. While you should always secure a professional exam to determine your exact prescription, you hold the power to take that prescription and shop around for the hardware that fits both your lifestyle and your budget.

Strategy Pillar 3: Managing Services and Insurances

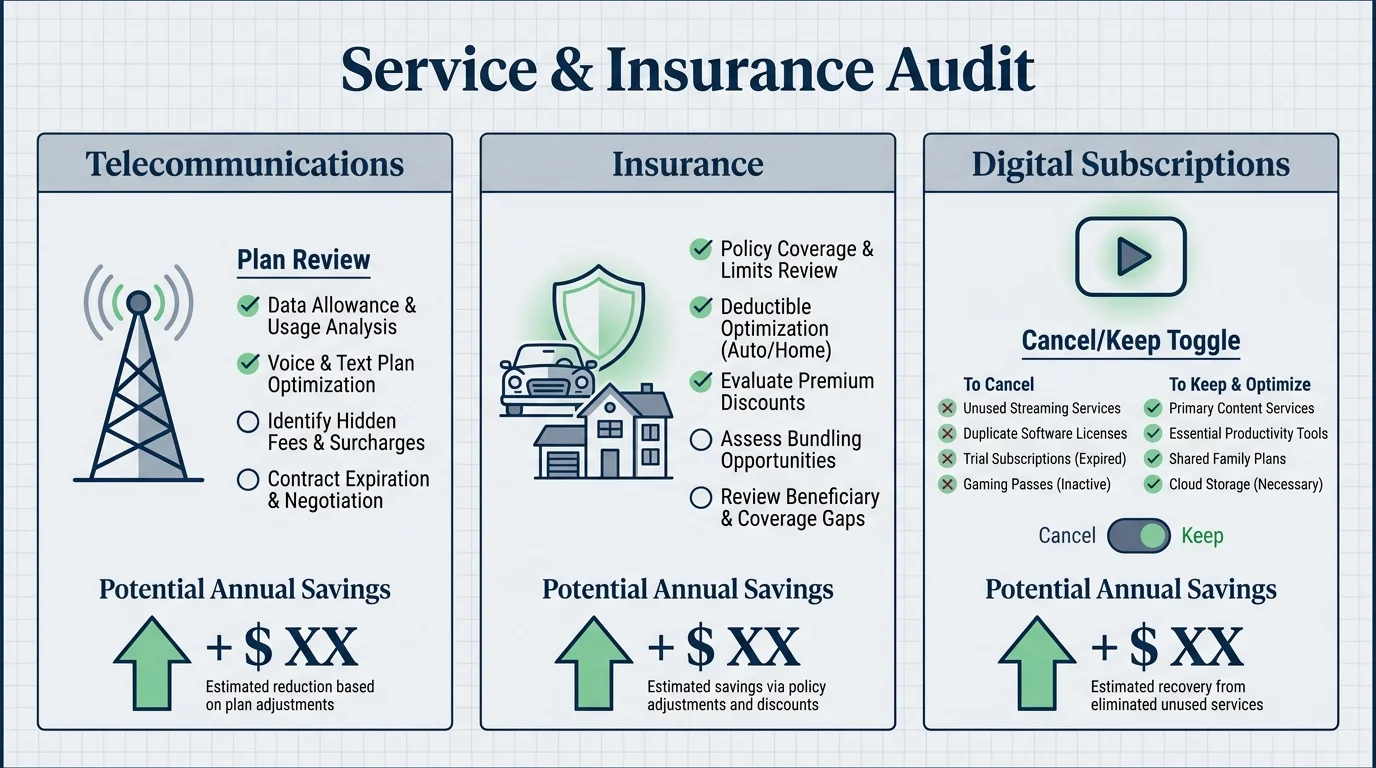

Service contracts and insurance policies operate on a business model known as the loyalty penalty. Companies offer spectacular introductory rates to acquire new customers, only to quietly inch those premiums and subscription fees upward year after year. If you simply auto-pay these bills without a second thought, you are actively subsidizing the discounts given to new clients. Implementing a yearly review of your digital and protective services ensures your money stays in your pocket.

Telecommunications and Cell Phone Plans

Cell phone carriers aggressively market limitless data plans that the average senior rarely utilizes. If your smartphone usage consists primarily of checking email, navigating maps, and texting family, you are likely overpaying for an unlimited tier. Alternative mobile virtual network operators lease cell tower space from the major telecom giants, providing the exact same coverage for significantly lower monthly fees. Taking the time to compare cellular plans specifically tailored to low-data users will effortlessly trim excess spending from your monthly budget.

Auto and Homeowners Insurance Policies

Insurance companies bank on consumer inertia. They understand that most policyholders dread the paperwork involved in switching providers, which gives them the leverage to implement creeping rate hikes. You must secure multiple quotes for your auto and homeowners insurance every single year. Frequently, a competitor will offer identical or superior coverage limits for a noticeably lower premium. Furthermore, consolidating your policies with a single provider often unlocks bundling discounts that dramatically reduce your total annual liability.

Entertainment and Digital Subscriptions

The streaming revolution promised to save consumers from expensive cable bills, but many households now subscribe to so many distinct digital platforms that their total costs exceed traditional television. You should conduct a comprehensive audit of your bank statements to identify every recurring subscription charge. Compare your actual viewership against the monthly cost of each service. Canceling the platforms you rarely watch and rotating your subscriptions throughout the year based on seasonal programming is a highly effective method for reigning in entertainment expenses.

Travel and Leisure Accommodations

Retirement finally affords you the time to explore the world, but navigating the travel industry requires a sharp eye for deals. Pricing for flights, hotels, and rental cars fluctuates based on search history, booking platforms, and seasonality. Since you no longer have to plan your vacations around a rigid corporate holiday schedule, you can leverage your flexible calendar to travel during off-peak windows. Comparing rates across various online travel agencies, and then calling the hotel directly to ask if they can beat that advertised price, often yields incredible discounts and complimentary upgrades.

Real-World Voices on Senior Shopping Tips

Financial planners routinely observe a fascinating behavioral shift when their clients enter retirement. The psychological transition from accumulating wealth to safely depleting it often triggers intense anxiety. According to guidance on fixed-income budgeting from the Consumer Financial Protection Bureau, establishing predictable spending patterns helps mitigate this deeply rooted stress. When you implement a structured approach to price comparison, you replace feelings of helplessness with a sense of decisive financial agency.

Behavioral economists point out that human beings are naturally wired to favor the path of least resistance. We return to the same grocery store, renew the same insurance policy, and utilize the same pharmacy purely out of habit. Breaking these ingrained patterns requires conscious effort, but the financial rewards are undeniable. Savvy households treat their comparison shopping as a lucrative part-time job. Spending just two hours a month reviewing your fixed expenses and researching better alternatives can easily yield a return of several hundred dollars, a tax-free gain that profoundly impacts your quality of life.

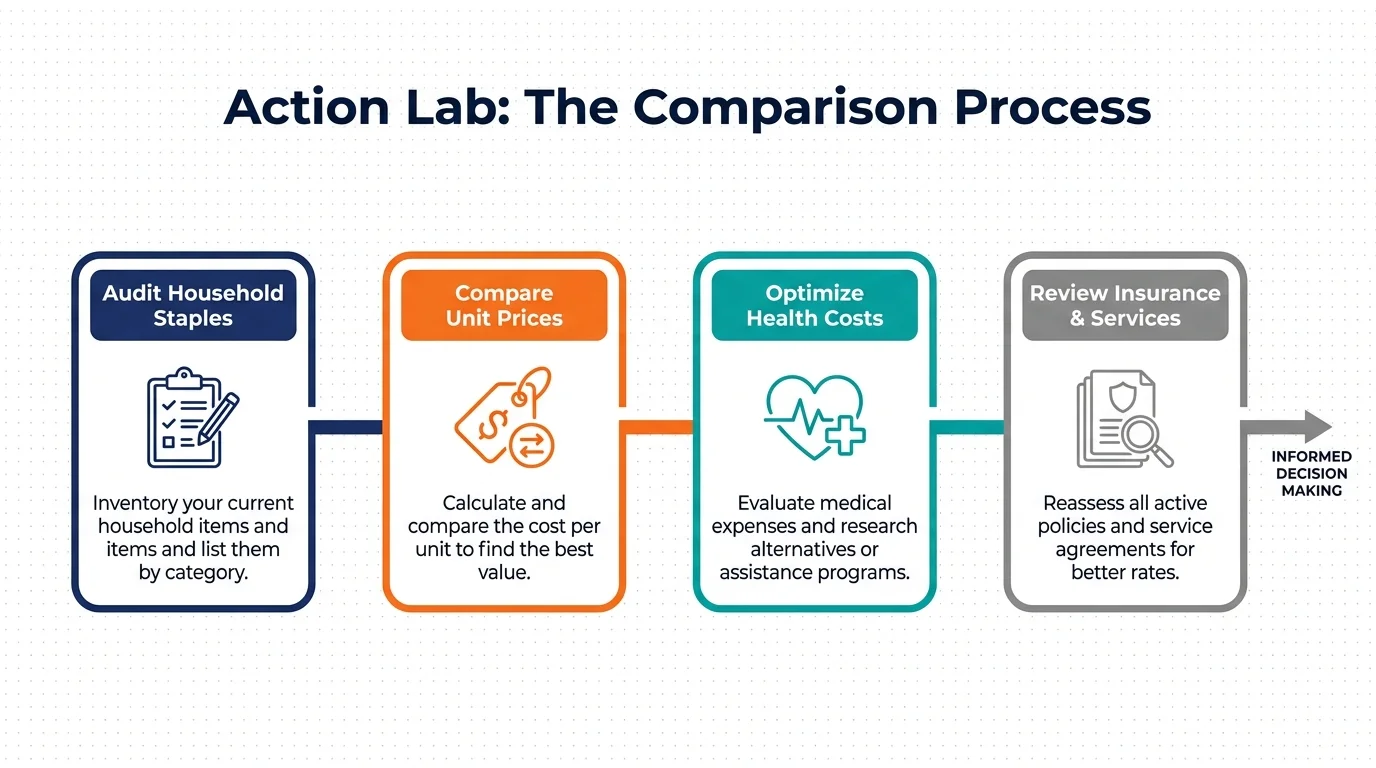

Action Lab: A Step-by-Step Price Comparison Walkthrough

Understanding the theory of comparison shopping is entirely different from executing it effectively. To translate these concepts into tangible results, you need a repeatable framework. Let us examine a realistic scenario: evaluating a costly recurring auto insurance premium. Your goal is to determine if your current provider still deserves your business without letting the process overwhelm you.

First, you must gather your baseline data by pulling your current policy declarations page. You need to know exactly what you are currently paying and the precise coverage limits, deductibles, and riders attached to your profile. Next, dedicate a quiet afternoon to requesting quotes from at least three competing insurance carriers. You can use an online comparison aggregator or contact independent insurance brokers in your area. Ensure you input the exact same coverage limits you currently hold so you are making a valid, equivalent comparison.

Once the quotes arrive, evaluate the bottom line numbers alongside the reputation of the carriers. Suppose you discover that a highly rated competitor offers the exact same coverage for forty dollars less per month. Your final step is to contact your current provider. Politely inform their retention department about the competitive quote you received. Frequently, your current provider will magically find a loyalty discount to match the competitor’s price, allowing you to capture the savings without the hassle of migrating your accounts. If they refuse to negotiate, you confidently initiate the switch, knowing you just secured nearly five hundred dollars in annual savings.

Guardrails and Pitfalls of Bargain Hunting

While stretching your retirement dollars is paramount, an obsessive pursuit of the lowest possible price can occasionally backfire. You must recognize the threshold where extreme frugality transforms into a false economy. A prime example involves warehouse club bulk purchasing. Buying a massive quantity of perishable goods at a steep discount is only a bargain if you actually consume the product before it spoils. Throwing away expired food negates any upfront savings and ultimately strains your budget further.

Another significant pitfall involves sacrificing quality for a minor price reduction, particularly regarding your health and safety. Purchasing ultra-cheap, poorly manufactured tires to save a few dollars jeopardizes your physical well-being. Similarly, falling prey to unbelievably low prices on unfamiliar websites often exposes you to counterfeit goods or digital scams. You must balance your desire for savings with a healthy dose of skepticism, ensuring that the businesses you patronize maintain strong consumer trust ratings and transparent return policies.

Frequently Asked Questions About Compare Prices for Seniors

How much time should I dedicate to price shopping each week?

You do not need to turn comparison shopping into a stressful daily chore. Dedicating just one or two hours every month to review your larger recurring bills—such as insurance premiums and subscription services—delivers the highest return on your invested time. For daily purchases like groceries, simply maintaining an awareness of unit prices during your standard weekly shopping trip is usually sufficient to capture meaningful savings.

Are warehouse club memberships actually worth the upfront cost for a two-person household?

The math heavily favors warehouse clubs if you are strategic about your purchases. While a two-person household might struggle to finish bulk perishables, the steep discounts on non-perishable items, over-the-counter medications, paper goods, and gasoline easily offset the annual membership fee. You must review your typical consumption habits to ensure you will actually utilize the specific categories where the club offers the deepest discounts.

Is it safe to buy prescription medications from online discount pharmacies?

Purchasing medications online is incredibly safe and cost-effective provided you use properly accredited pharmacies. You should exclusively utilize websites that display the Verified Internet Pharmacy Practice Sites seal, which indicates the pharmacy complies with strict state and federal regulations. Always consult your primary care physician before switching pharmacies to ensure your medical records remain properly consolidated.

Do loyalty programs really save money or just encourage me to spend more?

Retail loyalty programs are purposefully designed to gamify your shopping experience and encourage unnecessary spending. However, if you strictly harness these programs to purchase items you were already planning to buy, they provide excellent supplementary discounts. The key is to ignore the promotional emails urging you to buy extra products just to earn arbitrary points, treating the program solely as a passive discount mechanism at the checkout register.

Your Next Step Toward Smarter Retirement Budgeting

Transitioning into retirement empowers you to take absolute command of your financial ecosystem. The data is clear: relying on outdated habits and brand loyalty slowly drains your hard-earned nest egg. However, research published by major investment firms like Fidelity indicates that retirees who actively manage their spending require significantly less capital to maintain a joyful, secure lifestyle. You possess the time, the resources, and the wisdom to outsmart the marketplace.

Your challenge for this week is incredibly simple. Choose just one of the ten categories detailed above. Pull your latest statement, spend thirty minutes researching the competition, and negotiate a better rate. Once you secure that initial victory and watch your monthly expenses drop, the momentum will inspire you to tackle the rest of your budget. Seize control of your cash flow today, and build the financial peace of mind you absolutely deserve.