Mixing business expenses with your personal credit card creates a financial nightmare that threatens your livelihood and peace of mind. You can protect your family budget and simplify your tax filing by establishing strict boundaries between your personal and professional spending today. When you launch a side hustle or small enterprise, reaching for the familiar plastic in your wallet feels convenient and harmless. However, this common shortcut exposes your personal credit score to unnecessary risk and complicates your cash flow. By understanding exactly which business costs should never touch your personal accounts, you safeguard your middle-income household from sudden liabilities. Protecting your financial foundation requires recognizing the difference between a simple convenience and a costly misstep.

The State of Your Wallet and Small Business Finances

Middle-income households increasingly rely on freelance work, side gigs, and small businesses to outpace inflation and build generational wealth. If you operate a growing business out of your home office or manage a local storefront, you already juggle enormous mental loads. Unfortunately, relying on personal credit lines to fund operational costs masks your true profitability and artificially inflates your household spending profile. According to Federal Reserve survey data, a significant percentage of small business owners lean on personal credit, exposing their private assets to commercial volatility.

When you swipe a personal card for business costs, you drain your personal liquidity. This leaves you vulnerable when actual family emergencies strike, such as a broken water heater or an unexpected medical bill. A maxed-out personal credit card heavily impacts your debt-to-income ratio, making it incredibly difficult to secure an auto loan or refinance your mortgage at favorable rates. Establishing a clear wall between your household finances and your commercial enterprise transforms how you manage money, offering you clarity and profound peace of mind.

Strategy Pillar One: Cash-Flow Audits and Financial Boundaries

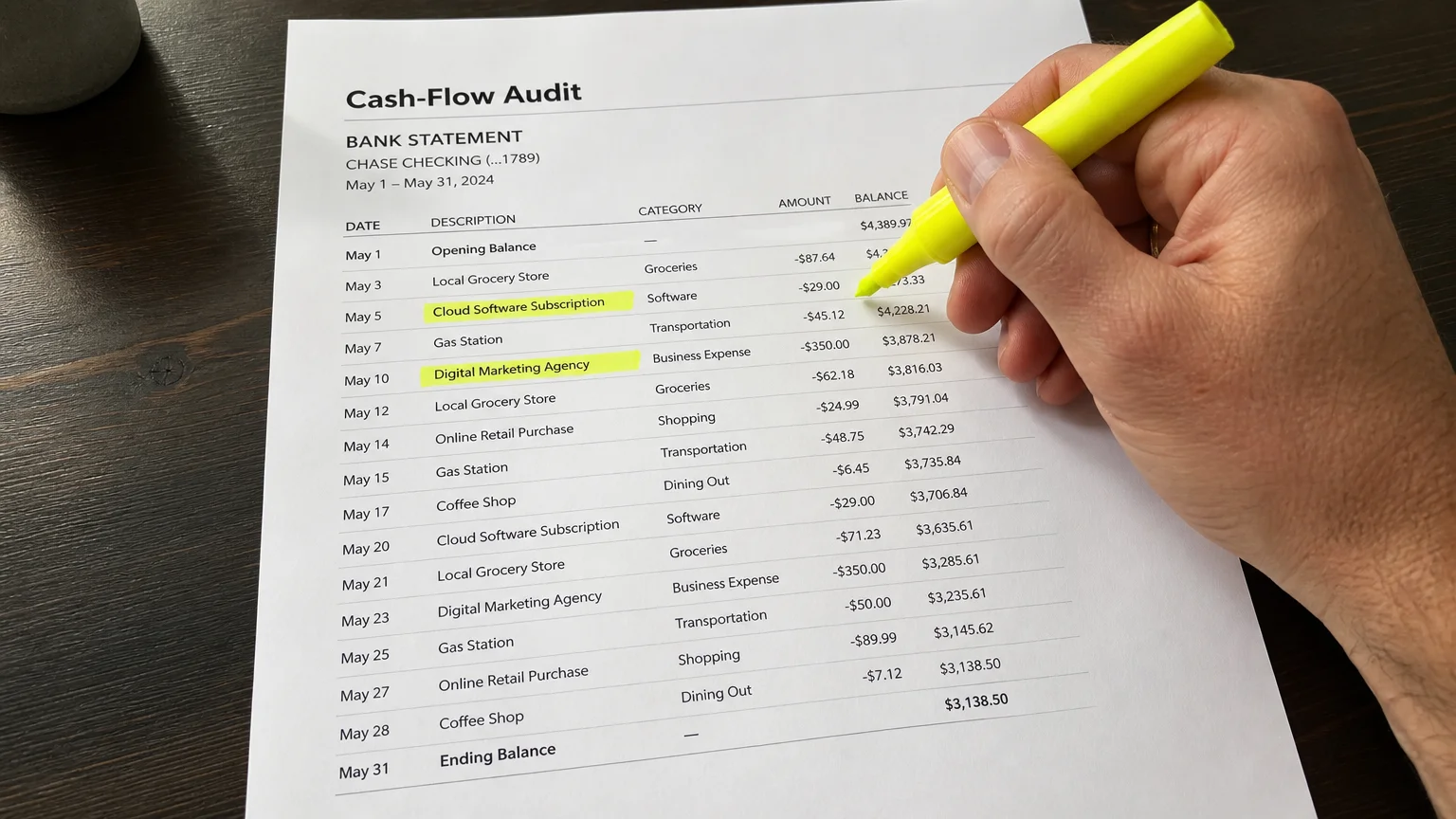

You cannot manage what you do not measure. Conducting a comprehensive cash-flow audit serves as your first line of defense against mingled finances. You must sit down with your last three months of personal credit card statements and highlight every single transaction related to your business. Seeing the exact dollar amount of commercial spending hidden inside your personal budget often provides a necessary shock to the system. Once you calculate this total, you recognize how much of your family credit utilization currently subsidizes your business operations.

Drawing firm financial boundaries requires opening dedicated business checking accounts and securing a designated business credit card. This simple infrastructure upgrade prevents you from accidentally piercing the corporate veil—a legal concept that protects your personal assets from business liabilities. If you operate an LLC but treat your personal card as a business slush fund, a judge can revoke your liability protection during a lawsuit, placing your family home and personal savings at immediate risk. Set the boundary today.

7 Specific Things Business Owners Should Never Charge on a Personal Card

1. Recurring Software Subscriptions and Digital Services

Modern businesses run on software, from customer relationship management platforms to accounting software and email marketing tools. Charging these automated monthly fees to your personal card guarantees an accounting headache at the end of the year. Because these charges auto-renew silently, they easily blend in with your personal streaming services and digital subscriptions. Come tax time, you will waste countless hours trying to isolate your professional software expenses from your household entertainment. Moving all commercial subscriptions to a dedicated business card ensures a clean, automated digital paper trail that you can hand directly to your tax professional.

2. Large Equipment Purchases and Hardware Upgrades

Purchasing heavy machinery, commercial printers, or high-end laptop computers demands significant capital. Dropping a five-thousand-dollar equipment charge onto your personal credit card creates an immediate and severe spike in your credit utilization ratio. The Consumer Financial Protection Bureau provides strict credit utilization guidelines, noting that utilizing more than thirty percent of your available credit aggressively lowers your credit score. Furthermore, business credit cards often provide superior extended warranties and purchase protections specifically designed for commercial hardware, which you forfeit entirely when using consumer-grade plastic.

3. Inventory Orders and Wholesale Supplies

If you run an e-commerce brand or a retail shop, purchasing inventory represents the lifeblood of your cash flow. Running wholesale supplier invoices through your personal card creates a perilous cycle of debt. If a product line fails to sell quickly, you remain personally on the hook for the balance, accumulating high personal interest rates while the merchandise sits in your garage or warehouse. Tracking your exact cost of goods sold becomes incredibly convoluted when inventory purchases sit next to your weekly grocery runs on a personal statement. You must keep inventory expenses entirely isolated to accurately gauge your profit margins.

4. Professional Services and Independent Contractor Fees

Paying freelance web developers, graphic designers, or legal consultants requires meticulous record-keeping. The Internal Revenue Service mandates specific reporting procedures for independent contractors, including the issuance of 1099 forms for services exceeding specific dollar thresholds. When you pay these professionals using your personal credit card, you blur the lines of your commercial operation, raising immediate red flags during an audit. Maintaining strict deducting business expenses protocols requires you to demonstrate that contractor payments strictly serve business purposes, a task made infinitely harder when the payment originates from a personal consumer account.

5. Business Travel Flights and Hotel Accommodations

Booking flights, securing rental cars, and reserving hotel rooms for industry conferences generate substantial expenses. Business credit cards generally offer specialized travel multipliers, lounge access, and commercial travel insurance that far exceed the perks of standard personal cards. By charging a business trip to your personal account, you miss out on valuable business-tier reward points that could fund future corporate travel. More importantly, isolating your travel expenses on a business card provides irrefutable proof to tax authorities that the journey served a strictly professional purpose, protecting you from accusations of writing off personal vacations.

6. Client Entertainment and Expensive Dining

Taking a prospective client out for dinner or buying coffee for a vendor meeting represents a valid business development strategy. However, the IRS examines meal and entertainment deductions with intense scrutiny. If your commercial dining expenses live on the same personal credit card statement as your family restaurant outings, you invite a painful and detailed audit. You must demonstrate exactly who attended the meal and the specific business discussed. Using a business card creates an automatic categorization system, allowing you to quickly write the client’s name and business purpose directly on the physical receipt before matching it to a clean, commercial ledger.

7. Online Advertising Campaigns and Marketing Spend

Digital marketing costs on platforms like Facebook, Google, or local advertising networks scale rapidly. A successful ad campaign might quickly jump from fifty dollars a day to five hundred dollars a day as you capture more leads. Personal credit card issuers often flag these rapid, high-volume digital ad charges as suspicious consumer behavior, resulting in sudden card freezes. A frozen card halts your marketing momentum instantly. Business credit cards anticipate high-volume vendor charges and offer appropriate commercial limits, ensuring your lead generation engine never shuts down due to an overly sensitive consumer fraud algorithm.

Strategy Pillar Two: Smarter Saving Automations for the Self-Employed

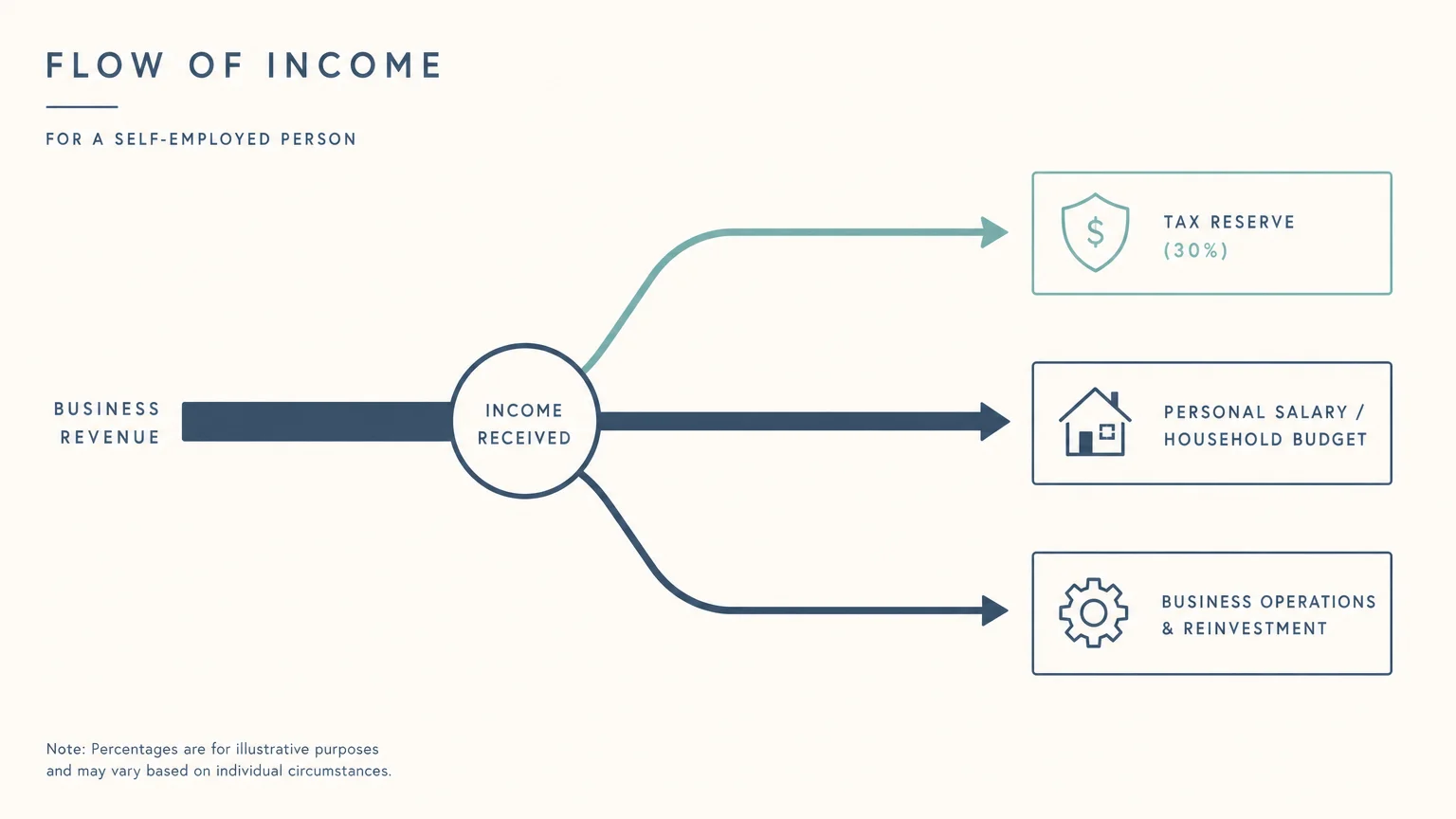

Separating your spending habits clears the path for intelligent savings automations. When your business card handles all operational expenses, your business checking account reflects your true net revenue. You can then establish an automated transfer rule that moves twenty-five to thirty percent of every incoming client payment directly into a dedicated business tax savings account. This proactive strategy entirely eliminates the dreaded springtime tax panic.

You also gain the ability to pay yourself a predictable, structured salary. Instead of treating your business revenue as a personal piggy bank, you transfer a set amount from your business checking to your personal checking twice a month. This system allows your middle-income household to budget accurately based on a reliable paycheck, rather than riding the unpredictable rollercoaster of fluctuating monthly business sales.

Real-World Voices: Insights from Financial Planners

Financial planners and behavioral economists frequently highlight the psychological burden of mingled finances. Experts note that humans struggle with cognitive load; when you constantly force your brain to separate personal survival money from business operational money, you experience decision fatigue. Financial advisors routinely see talented entrepreneurs stunt their business growth simply because they fear their personal credit card bill.

By splitting these entities entirely, you liberate your mental bandwidth. You stop viewing a necessary business investment—like upgrading your marketing software—as a threat to your family grocery budget. Advisors stress that treating your side hustle with the structural respect of a Fortune 500 company, starting with basic card separation, fundamentally shifts your mindset from a scrappy amateur to a confident chief executive.

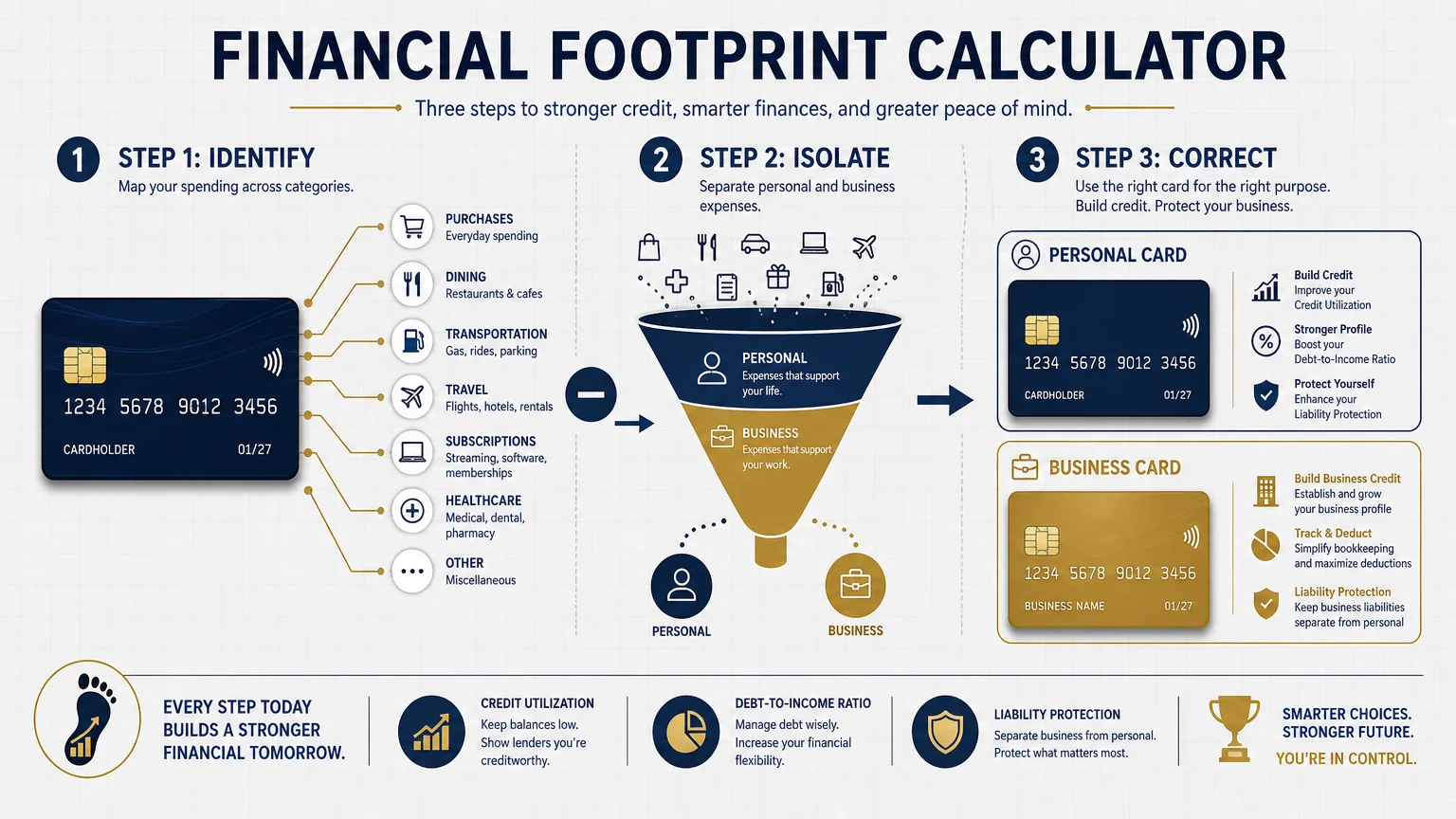

Action Lab: Calculating and Correcting Your Financial Footprint

You can execute a financial correction tonight by following a straightforward, actionable process. First, log into your personal credit card portal and download your transaction history for the past ninety days in a spreadsheet format. Create a new column and label it “Business Use.” Go line by line, marking every software, travel, or supply charge dedicated to your enterprise. Sum this column to discover your true commercial footprint.

Next, apply for a basic business credit card. You do not need massive revenue to qualify; many issuers evaluate your personal credit history and projected business income if you operate as a sole proprietor. Once the new physical card arrives in your mailbox, dedicate two uninterrupted hours to logging into your various vendor portals—your website host, your email provider, your wholesale suppliers—and update your billing profiles. Finally, cut up the sticky notes or delete the saved personal card numbers you previously used for these accounts. You have now established a fortified firewall around your household assets.

“A credit card road divides family security from business growth, protected by yellow mindful spending guardrails.”

1. A

2. credit

3. card

Strategy Pillar Three: Mindful Spending Guardrails and Pitfalls

Transitioning to a business card requires vigilance to ensure you do not simply transfer bad habits to a new piece of plastic. The most dangerous pitfall you face involves treating your new business credit limit as free money. You must institute strict mindful spending guardrails, treating the business credit card exactly like a debit card. If your business checking account lacks the cash to pay off the balance in full at the end of the month, you should pause the purchase.

Avoid the trap of financing long-term business losses on short-term high-interest credit. If your enterprise cannot sustain its operational costs without carrying a balance, you need to audit your pricing structure or significantly cut overhead. The Small Business Administration guidelines frequently warn against leveraging credit cards for long-term capital, suggesting instead that owners seek proper business term loans for major expansions.

Frequently Asked Questions About Business Expenses

Can I use a personal card for business if I pay the balance off immediately every week?

No, you should still avoid this practice entirely. Even if you pay the balance to zero every Friday, you continue to mingle the accounting records. This behavior actively threatens your corporate liability protection if you operate an LLC and creates a highly convoluted paper trail that frustrates accountants during tax season. Fast repayment does not solve the underlying legal and organizational issues.

Do I need an Employer Identification Number to get a business credit card?

While possessing an Employer Identification Number simplifies the application process, you do not strictly need one. If you operate as a sole proprietor or a freelance independent contractor, you can legally apply for most small business credit cards using your personal Social Security Number. However, obtaining an EIN from the IRS takes only a few minutes online and adds another excellent layer of separation between you and your commercial entity.

Will opening a business credit card negatively impact my personal credit score?

When you initially apply, the issuer will typically perform a hard inquiry on your personal credit profile, which may cause a temporary, minor dip in your score. However, most commercial card issuers report your ongoing business purchasing activity strictly to the commercial credit bureaus, keeping your business debt utilization completely off your personal credit report. You only risk your personal score if you default on the commercial account.

How do I qualify for a business card if my side hustle generates very little revenue?

Card issuers understand that new businesses require capital before they generate massive profits. When applying, you can usually list your projected revenue alongside your existing personal household income. Banks primarily rely on your personal creditworthiness to approve the account, requiring you to sign a personal guarantee. Start with a card offering a modest limit and build your commercial credit history through responsible, on-time payments.

Your Next Step Toward Financial Clarity

Untangling your personal livelihood from your commercial ambitions requires a deliberate commitment, but the peace of mind you gain is immeasurable. You possess the power to protect your household budget, streamline your tax filings, and build a resilient enterprise starting today. Take one hour this evening to audit your personal statements and initiate the application for a dedicated business credit card. By constructing these vital financial boundaries, you transform stress into strategy, ensuring that your business growth never comes at the expense of your family’s financial security.