Managing your money in your seventies requires a clear understanding of typical senior expenses to stretch your retirement budget without sacrificing your quality of life. Knowing whether you spend more than average helps you pinpoint where your cash flow might be leaking and allows you to adjust your financial strategy immediately. As you transition deeper into retirement, healthcare costs predictably rise while housing and transportation expenses shift in surprising ways. Comparing your own monthly outflow against national benchmarks provides the ultimate reality check for middle-income households navigating fixed incomes. By aligning your spending with practical financial data, you gain the confidence to cover unexpected bills, fund meaningful experiences, and preserve your nest egg for the long haul.

State of the Wallet: Navigating Retirement Budget Realities

Retirement spending rarely follows a flat line; instead, it often resembles a smile. In your early seventies, you typically sit at the bottom of this spending curve. Your discretionary expenses likely taper off compared to your highly active sixties, yet you have not quite reached the steep, unavoidable healthcare costs that often characterize your eighties. Understanding this natural progression helps you frame your current budget realistically and prevents you from panicking over normal financial shifts. Middle-income households often feel a unique pressure during this decade because they hold too much wealth to qualify for extensive assistance programs, but not enough to ignore inflation or market volatility.

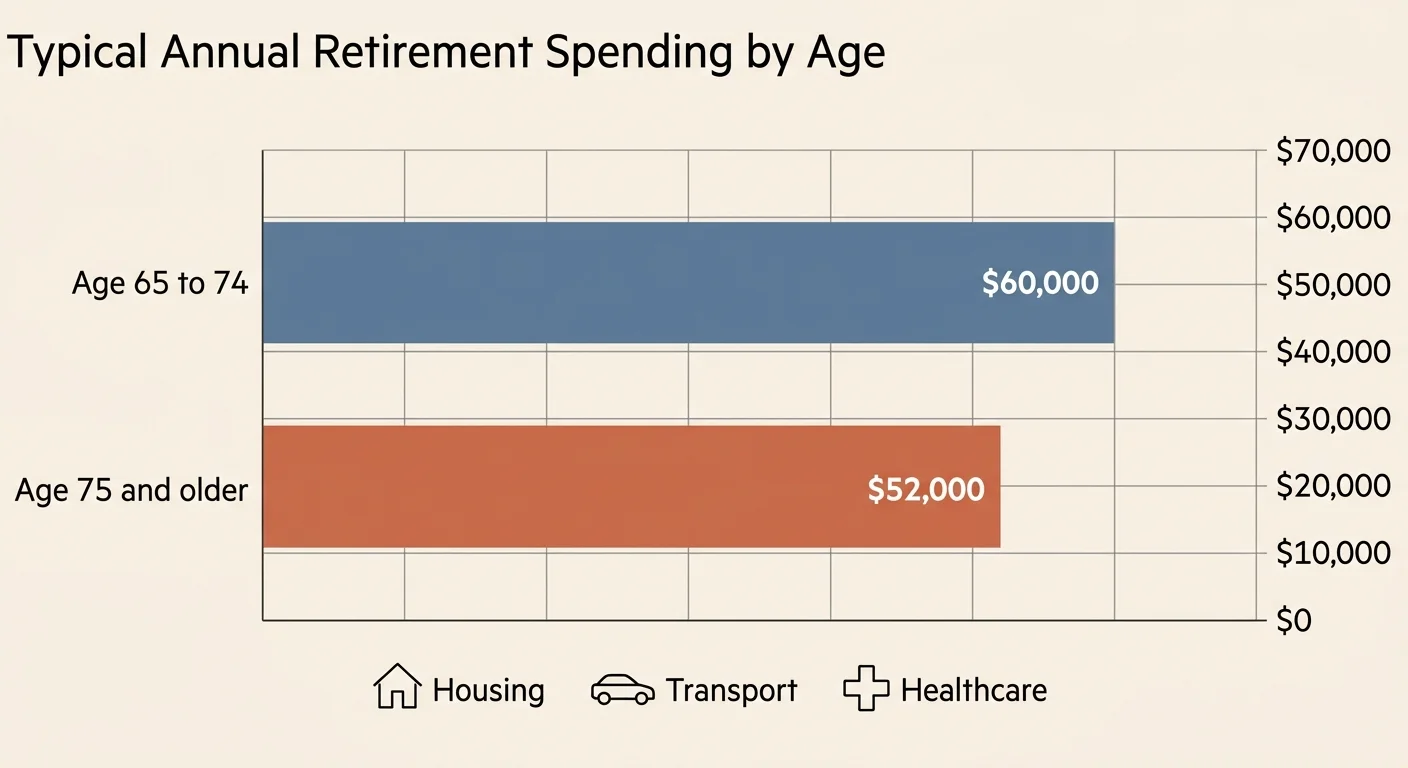

The numbers reveal exactly where the money goes during this stage of life. According to annual spending surveys published by the government, the average household headed by someone aged 65 to 74 spends approximately $60,000 annually, while those 75 and older spend roughly $52,000 a year. Housing consistently consumes the largest slice of this pie, demanding nearly a third of the typical senior budget. Even if you paid off your mortgage years ago, property taxes, home insurance premiums, and routine maintenance costs never retire. Transportation and healthcare fight for second place, each demanding a significant portion of your fixed monthly income.

Inflation complicates these benchmarks further. When your income relies heavily on Social Security and fixed pension payments, rising prices at the grocery store and the gas pump erode your purchasing power. While cost-of-living adjustments help, they frequently fall short of covering the specific goods and services older adults need most. Acknowledging these national averages gives you a sturdy baseline. If you discover your housing costs consume fifty percent of your income, or your transportation costs far exceed the typical senior average, you instantly know exactly which categories require your immediate attention.

Strategy Pillar 1: Conducting a Cash-Flow Audit for Fixed Incomes

You cannot fix a budget if you do not know exactly what you spend. Conducting a comprehensive cash-flow audit empowers you to reclaim control over your outflow. Start by printing out your bank and credit card statements from the past ninety days. A three-month window smooths out the anomalies, capturing the seasonal utility spikes alongside your routine grocery trips. Grab two highlighters; use one color for absolute necessities like housing, groceries, and medical copays, and use the second color for discretionary spending such as dining out, streaming services, and travel.

As you review these transactions, hunt relentlessly for subscription creep. Middle-income households frequently bleed hundreds of dollars a year on auto-renewing charges for magazines, premium cable channels, or gym memberships they no longer utilize. Cancel anything you have not actively used in the last month. Next, scrutinize your essential bills to find hidden negotiation opportunities. You can often lower your internet bill simply by calling your provider and asking for a senior loyalty discount; similarly, you should shop your auto and home insurance policies annually to ensure you are receiving the best possible rates.

Finally, categorize your spending into percentages and compare them against the national averages mentioned earlier. If your discretionary spending consistently outpaces your essential savings and healthcare reserves, you must rebalance your outflow. This exercise is not about restricting your joy or forcing you to live a life of deprivation. Rather, a cash-flow audit eliminates mindless spending so you can intentionally direct your hard-earned money toward the experiences and security you truly value.

Strategy Pillar 2: Automating Your Savings and Essential Bill Payments

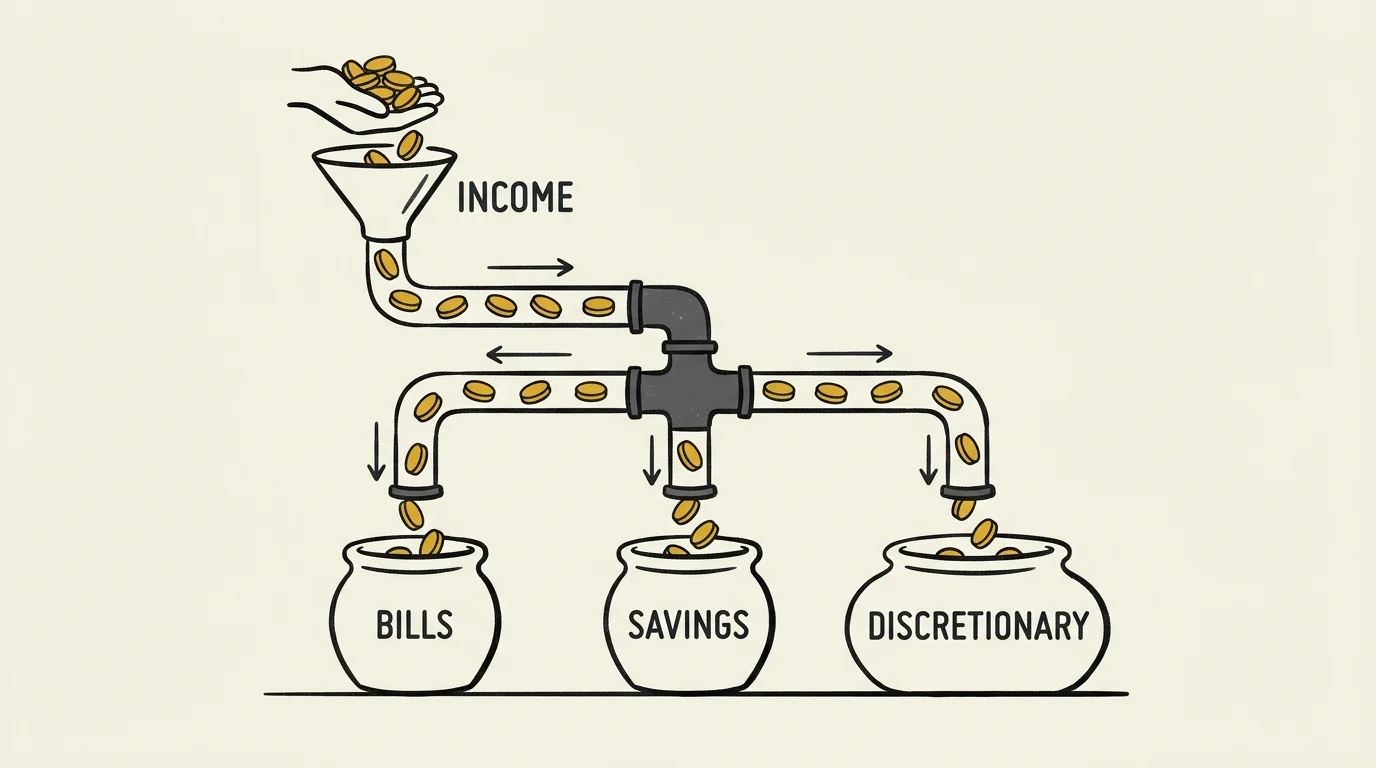

Many retirees falsely believe they no longer need to save once they stop working. In reality, maintaining a robust cash reserve in your seventies remains crucial for navigating sudden home repairs or unexpected medical diagnoses. Automating your finances removes the emotion from saving and ensures your most critical bills are always paid on time, protecting your credit score and your peace of mind.

Begin by setting up an automated transfer from your primary checking account to a high-yield savings account. Treat your Social Security deposit or pension check just like a paycheck; schedule a small, mandatory transfer of fifty or one hundred dollars to move into your emergency fund the day after your income arrives. Over time, these automated contributions rebuild the cash reserves you deplete when life throws you a curveball. By keeping this emergency fund in a high-yield account, you force your idle cash to outpace basic inflation.

You should also automate your mandatory expenses. Set your utilities, insurance premiums, and property tax payments to auto-draft from your checking account. This strategy prevents late fees and relieves you of the mental burden of tracking due dates. If you receive Required Minimum Distributions from your retirement accounts, automate those withdrawals to funnel directly into your core spending account, simulating a reliable monthly salary. Leveraging these financial resources for older adults ensures your financial engine hums smoothly in the background while you focus on enjoying your retirement.

Strategy Pillar 3: Mastering Mindful Spending Without Sacrificing Joy

Stretching your retirement dollars does not mean sitting at home staring at the walls. Mastering mindful spending allows you to fund an incredibly rich lifestyle on a middle-income budget. The secret lies in substitution and optimization, rather than outright elimination. When you shift your mindset from purchasing physical goods to investing in meaningful experiences, you often find that your money stretches significantly further.

Optimize your travel and entertainment by embracing the flexibility that retirement provides. Since you no longer contend with a traditional work schedule, you can book flights on quiet Tuesday mornings and secure lodging during the off-season when prices plummet. Take full advantage of age-based discounts at state parks, museums, and local theaters. Many cultural institutions offer drastically reduced admission for seniors, allowing you to stay active and engaged within your community for a fraction of the standard cost.

Apply this same mindful approach to your daily routines. Rethink your grocery habits by planning meals around seasonal produce and bulk staples, which drastically reduces food waste and lowers your weekly grocery bill. If dining out represents a major source of joy, shift your restaurant visits from expensive weekend dinners to heavily discounted weekday lunches. These subtle adjustments preserve the core experience you desire while keeping your spending firmly aligned with your fixed-income realities.

Insights from the Experts: Real-World Voices on Senior Expenses

Financial planners who specialize in retirement transitions routinely observe a distinct psychological barrier when clients reach their seventies. For decades, you trained your brain to save aggressively, stockpile resources, and delay gratification. Transitioning from saving to spending often triggers immense anxiety, leading many retirees to live far below their means and miss out on the experiences they worked so hard to afford.

Behavioral economists note that retirees frequently miscalculate the cost of remaining in an oversized family home. Experts urge seniors to look beyond the paid-off mortgage and calculate the true carrying costs of their property. Heating a four-bedroom house, paying soaring property taxes, and hiring help for lawn care or snow removal can silently drain a retirement portfolio. Downsizing is not merely a financial transaction; it represents a strategic lifestyle choice that frees up significant monthly cash flow while reducing physical maintenance burdens.

Furthermore, consumer advocates warn against the dangers of the silent inflation that impacts healthcare. Industry professionals emphasize that Medicare does not cover everything, and out-of-pocket costs for dental care, vision, and hearing aids can easily shock an unprepared budget. By listening to these expert perspectives, you can anticipate these structural shifts and adjust your financial blueprint long before an emergency forces your hand.

Action Lab: A Step-by-Step Budget Tweak

To demonstrate how quickly you can improve your monthly cash flow, let us walk through a practical budget tweak designed to uncover three hundred dollars in savings without impacting your lifestyle. Start by isolating your transportation expenses. If your household maintains two vehicles but you only drive one regularly, you possess a massive opportunity for optimization. Calculate the annual cost of the second vehicle by adding up its insurance premiums, registration fees, maintenance, and depreciation.

Next, evaluate your grocery spending. Switch to store-brand staples for items where brand names do not impact quality, such as rolled oats, canned beans, and paper products. Dedicate just twenty minutes a week to reviewing the digital coupons offered by your local supermarket before you build your shopping list. This simple habit routinely shaves ten to fifteen percent off a standard grocery bill. Combine this with batch cooking to ensure you maximize the ingredients you purchase.

Finally, tackle your telecommunications bill. If you currently pay for a premium bundled cable and internet package, call your provider to strip away the channels you never watch. Switch to a lower-tier internet speed; most households do not require gigabit speeds to check email and stream the occasional movie. By executing these three straightforward steps, you easily reclaim hundreds of dollars a month, giving your retirement budget tremendous breathing room.

Guardrails and Pitfalls: Avoiding Common Financial Mistakes in Your 70s

Even the most meticulously crafted budget can collapse if you fail to implement appropriate financial guardrails. One of the most common pitfalls retirees face is functioning as a family bank. While helping your adult children or grandchildren is a noble desire, doing so at the expense of your own financial security creates long-term disaster. Middle-income retirees must firmly prioritize their own solvency. You cannot secure a loan to fund your retirement, but your children can secure loans to buy homes or fund their education.

Another major vulnerability involves sophisticated financial scams. As you accumulate wealth over a lifetime, you become a prime target for fraudsters. Scammers frequently use high-pressure tactics involving fake IRS debts, compromised bank accounts, or grandchildren in distress. Guard your personal information fiercely. Never provide your social security number, bank details, or credit card numbers to incoming callers. If you receive a suspicious call claiming to be from your bank, hang up immediately and dial the number printed directly on the back of your debit card.

Finally, you must avoid the trap of ignoring long-term care planning. A significant portion of adults will require some form of assisted living or in-home care later in life. Failing to plan for these expenses leaves you completely exposed. Review the economic well-being of households data, which consistently shows that medical shocks create the highest financial distress for seniors. Consult with an elder law attorney or a financial advisor to understand how you can shield your assets and cover potential care costs down the road.

Frequently Asked Questions About Retirement Spending

How much should I realistically budget for healthcare in my 70s?

Healthcare will likely be one of your largest expenses, even with Medicare. You must budget for your Part B premiums, a Medicare Supplement or Advantage plan, Part D prescription drug coverage, and out-of-pocket costs for dental and vision care. Recent healthcare cost estimates suggest that a 65-year-old couple retiring today will need hundreds of thousands of dollars to cover health expenses throughout their retirement. A safe rule of thumb is to allocate at least fifteen percent of your monthly income specifically toward healthcare premiums and out-of-pocket medical reserves.

Is it normal to carry a mortgage into my 70s?

While previous generations aimed to burn their mortgages before retiring, an increasing number of middle-income seniors today carry mortgage debt into their seventies. It is completely normal, though it does restrict your monthly cash flow. If your mortgage interest rate is incredibly low, it often makes mathematical sense to maintain the loan rather than liquidating a large chunk of your retirement portfolio to pay it off. However, you must ensure your fixed income comfortably covers the monthly payment alongside rising property taxes.

How do I adjust my budget for inflation on a fixed income?

Combatting inflation requires vigilance and flexibility. Start by leaning heavily into categories you can control, such as food and entertainment, when fixed costs like utilities rise. Use generic brands, negotiate your service bills annually, and take advantage of all available senior discounts. Additionally, explore high-yield savings accounts and certificates of deposit to ensure your liquid cash earns interest that helps offset the rising cost of consumer goods.

Should I financially support my adult children during my retirement?

You should only offer financial support if you can do so without jeopardizing your own long-term security. Many retirees drain their nest eggs to help children with down payments or grandkid tuition, only to find themselves destitute when they need in-home care a decade later. Secure your own oxygen mask first. If your budget is tight, offer non-financial support like childcare or career mentorship. Protect your core assets ruthlessly to ensure you never become a financial burden to those same children later in life.

Moving Forward with Financial Confidence

Navigating your spending in your seventies does not have to be an exercise in anxiety. By understanding the typical expenses for this stage of life, you gain a powerful framework to measure your own financial health. You possess the tools to audit your cash flow, automate your essential savings, and optimize your spending so that every dollar serves a clear purpose. Remember, a well-structured budget is never a cage; it is a roadmap that grants you permission to spend joyfully on the things that matter most.

Your action item for tonight is simple. Log into your primary checking account and review your transactions from the past thirty days. Find just one recurring expense that no longer brings you value and eliminate it immediately. By utilizing budgeting resources and taking small, decisive actions, you will confidently protect your nest egg and build a deeply fulfilling, financially secure retirement.