Busy families caring for aging parents can immediately reclaim their vanishing monthly cash flow by combining a total budget refresh with targeted government assistance. You face mounting grocery bills and healthcare costs, leaving your own household budget stretched incredibly thin. Millions of older adults qualify for programs that drastically reduce prescription costs, property taxes, and utility bills, yet they never apply. By integrating these overlooked senior benefits into a structured budgeting framework, you can permanently eliminate cash leaks and restore financial peace of mind. Discover how to capture that missing extra support and build a money management system that actually works for your entire family, protecting both your retirement goals and your immediate daily needs.

Diagnosing the Leak in Your Household Cash Flow

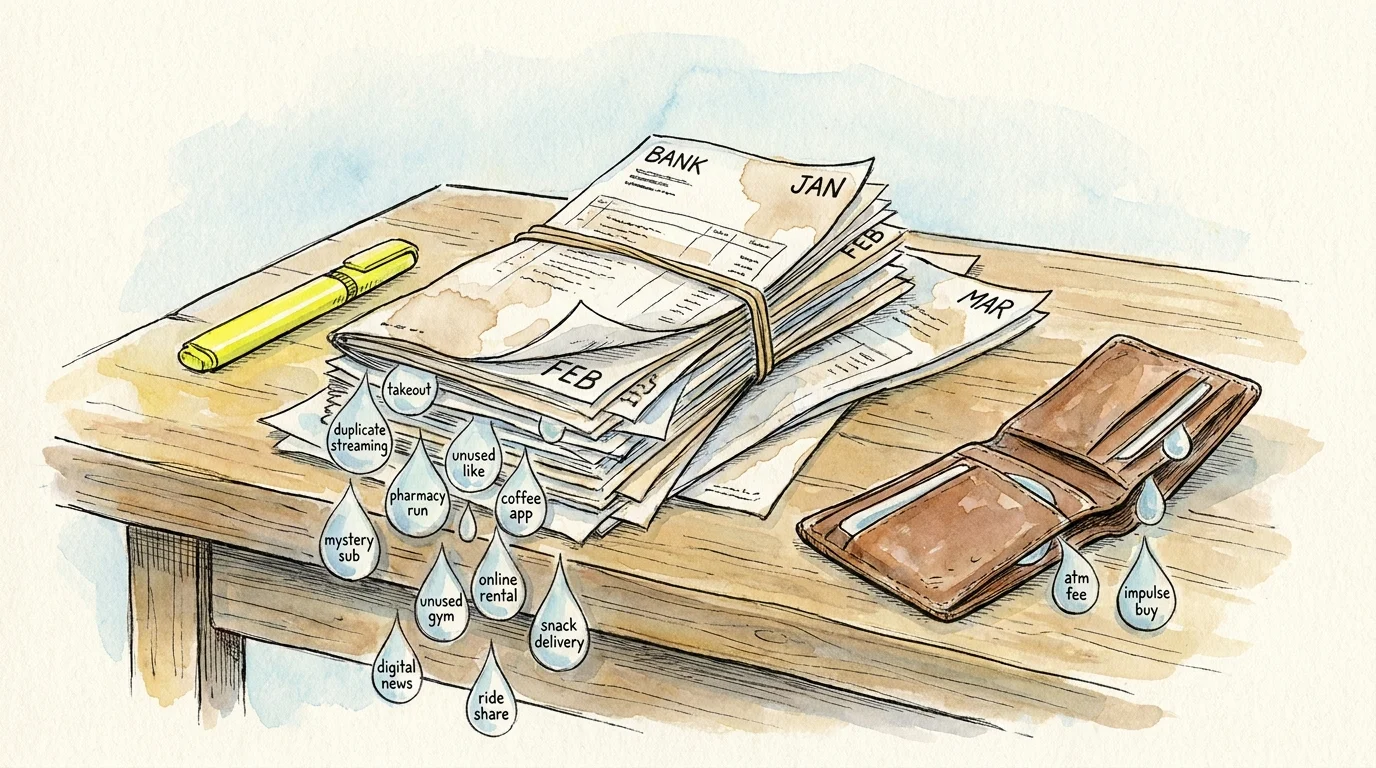

The first step to fixing a broken cash flow involves facing your numbers head-on. Many families unwittingly subsidize their aging parents’ living expenses, absorbing routine costs that quietly drain their own checking accounts. You must gather three months of bank statements and highlight every recurring charge, subscription, and everyday purchase. This granular exercise frequently reveals hidden costs, such as convenient takeout meals purchased when you feel too exhausted to cook, or duplicate streaming subscriptions spread across multiple family members. Once you map out your exact outbound cash flow, you need to assess your income streams with absolute honesty. This is precisely where identifying available financial assistance changes the entire landscape of your family budget.

When you sit down to map out your income and expenses, identifying missed government programs can radically shift your monthly baseline. If your family currently pays out of pocket for an older relative’s medications, discovering available relief programs frees up critical capital. Millions of retirees leave money on the table simply because the application processes feel overwhelming or they incorrectly assume their income disqualifies them.

You can instantly improve your cash flow by helping your parents claim seven commonly overlooked benefits. First, Medicare Savings Programs directly help cover burdensome premiums and deductibles. Second, the Extra Help program for prescription drugs easily saves a household hundreds of dollars every month on pharmacy runs. Third, the Supplemental Nutrition Assistance Program provides essential grocery relief; reviewing recent USDA spending data shows that food costs consume a massive portion of family income, yet many seniors assume they earn too much to qualify. Fourth, the Low Income Home Energy Assistance Program offsets staggering utility bills during peak summer and winter months. Fifth, local property tax freezes keep housing costs manageable for older homeowners living on fixed incomes. Sixth, Supplemental Security Income delivers vital cash assistance for those with strictly limited resources. Finally, the Veterans Affairs Aid and Attendance benefit provides substantial monthly payouts for veterans requiring personal care. By verifying eligibility through resources like the National Council on Aging, you effectively inject new, dependable income into your household ecosystem.

Selecting a Budgeting System That Fits Your Life

Now that you have maximized your household income and mapped your historical expenses, you need a resilient framework to govern your money. Not every system works for a busy family managing multigenerational costs. The zero-based budget requires you to assign every single dollar a specific job before the new month even begins. If your total household income equals $6,000, your planned expenses, savings contributions, and debt payments must equal exactly $6,000. This method works brilliantly for families who need total control over tight margins and want to track exactly where their elder care subsidies go.

Alternatively, the 50/30/20 rule offers a broader, slightly less restrictive approach to money management. You allocate 50 percent of your income to absolute needs like housing and medication, 30 percent to discretionary wants like dining out or entertainment, and 20 percent to debt repayment and future savings. According to financial experts at Bankrate, this specific framework perfectly suits households possessing a comfortable cash cushion who simply need high-level guardrails rather than daily micro-management. It allows you to absorb occasional price fluctuations in groceries or utility bills without feeling compelled to rewrite your entire financial plan.

Finally, the digital envelope system forces hard spending limits on troublesome, variable categories. Traditionally, you would partition cash into physical envelopes for groceries, entertainment, and miscellaneous expenses; once the physical cash runs out, you stop spending. Modern families typically prefer replicating this strategy through specialized banking applications. This digital boundary actively prevents the incredibly common habit of overspending at the supermarket, ensuring you always have enough liquidity reserved for essential health and housing costs.

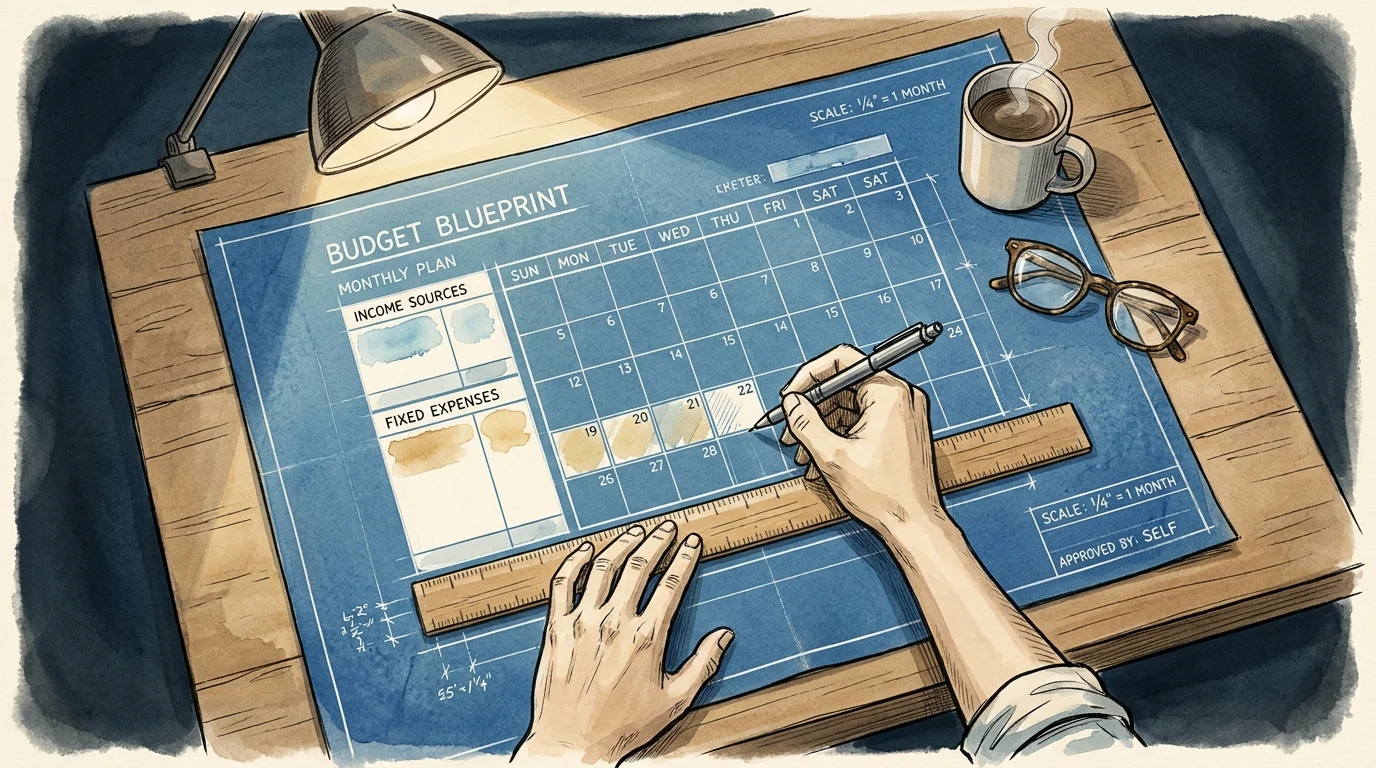

A Step-by-Step Guide to Building Your Blueprint

With your preferred system selected, you must build your actual budget blueprint using concrete numbers. Start by securing a clean spreadsheet or purchasing a physical ledger. First, list your fixed expenses. These represent the non-negotiable, highly predictable costs that hit your checking account every single month, such as your $1,800 mortgage, $400 car payment, and $150 internet bill. Do not guess these amounts; pull the exact figures directly from the bank statements you reviewed earlier. Fixed expenses form the unbreakable bedrock of your financial obligations, and knowing this total dictates how much freedom you have elsewhere.

Next, estimate your variable expenses. These categories fluctuate based on your behavioral habits and seasonal needs, encompassing groceries, vehicle fuel, and basic utility bills. Because variable costs can easily spiral out of control, you must set realistic monthly caps based on your historical spending data. If you typically spend $900 on groceries, do not arbitrarily cut that budget to $400 in a sudden burst of false optimism. Gradually reduce the target to $800, utilizing the savings generated by those newly claimed senior grocery benefits to bridge the financial gap comfortably.

The final and perhaps most crucial step involves establishing sinking funds. Sinking funds allow you to save incrementally for large, known expenses rather than panic-putting them on a high-interest credit card. For example, if you know your aging parent will require a $1,200 dental procedure in six months, you create a dedicated sinking fund and contribute exactly $200 each month. You can seamlessly apply this identical concept to annual property taxes, back-to-school shopping for your children, and holiday gifts. Separating these funds from your primary checking account ensures the money remains completely untouched until the specific need arises.

Leveraging Automation and Fintech Tools

Maintaining your budget requires unyielding consistency, and modern automation serves as your strongest ally in this pursuit. Busy families rarely have the spare time or mental energy to manually input every single transaction into a ledger at the end of an exhausting workday. Fintech budgeting applications connect directly to your bank accounts, automatically pulling in daily transactions and categorizing them according to your predetermined rules. The primary advantage of these applications lies in their immediate, real-time visibility. You can glance at your smartphone while standing in the checkout line and instantly see that you only have $45 left in your dining out category for the week. However, the notable downside of full automation is the potential for behavioral disconnection; you might stop paying close attention to your spending habits simply because the software handles all the heavy lifting.

If you prefer a more tactile approach to money management, dedicated budgeting spreadsheets offer a perfect middle ground. Spreadsheets force you to manually review and categorize your spending, keeping you highly engaged and deeply accountable to your cash flow. You can easily customize the rows and columns to perfectly match your unique household needs, tracking specific senior benefits alongside your primary income streams. The Consumer Financial Protection Bureau encourages consumers to regularly review their financial data and maintain active oversight of their accounts, a habit that manual tracking naturally reinforces. The drawback involves the necessary time commitment, as you must fiercely protect time each week to update the numbers. Whichever tool you ultimately choose, ensure it facilitates clear, transparent communication between you and anyone else involved in managing the household finances.

Building Accountability Habits That Stick

A beautifully crafted budget holds absolutely no value if you completely abandon it by the second week of the month. Establishing strong accountability habits transforms your budget from a theoretical spreadsheet into a highly practical lifestyle tool. Implement a mandatory weekly financial check-in lasting no more than fifteen minutes. Pick a consistent day, such as Sunday afternoon, to review your category balances and prepare for the week ahead. This brief administrative meeting allows you to pivot and adjust your meal plan if the grocery budget looks uncomfortably thin, or cancel an upcoming recreational outing if your entertainment funds are already depleted.

In addition to weekly reviews, schedule a comprehensive monthly financial summit. During this longer session, objectively evaluate what worked perfectly and what went completely off the rails. Did an unexpected pharmacy run blow up your medical category? This represents the perfect time to remind your aging relatives to utilize the extra help prescription program you previously signed them up for. To protect your ongoing progress, establish firm guardrails for your most common derailers. Unsubscribe from aggressive retail marketing emails that routinely trigger impulse purchases, and actively delete saved credit card information from your favorite online stores to introduce deliberate friction into the checkout process. Consistent, daily engagement builds the undeniable financial discipline required to maintain long-term stability.

Frequently Asked Questions About Family Budgeting

How do I budget with an irregular income?

Managing variable income requires a strict baseline approach. You must calculate your absolute bare-bones living expenses—the bare minimum amount required to keep a roof over your head, food on the table, and the lights turned on. Use your lowest-earning month from the past calendar year as your projected monthly income. When you earn more than that conservative baseline, immediately funnel the surplus directly into your emergency fund or apply it aggressively toward outstanding debts. Financial experts at the National Foundation for Credit Counseling highly recommend that variable-income earners build a significantly larger cash buffer than traditional households to smooth out the inevitable valleys in their monthly earnings cycle.

What is the best way to handle existing debt within a new budget?

Debt repayment must become an absolutely non-negotiable line item in your monthly blueprint. You can choose between the debt snowball method, which targets the smallest balances first to build rapid psychological momentum, or the debt avalanche method, which tackles the highest interest rates first to save the most money mathematically. Regardless of the specific strategy you select, consistently pay the minimums on all accounts and throw every extra available dollar at your primary target debt. Incorporating the senior benefit savings you recently unlocked provides an excellent, steady source of extra cash to dramatically accelerate this payoff process.

How can I protect my budget from unexpected expenses?

Unexpected expenses represent an absolute certainty in life, rather than a rare anomaly. You protect your monthly cash flow by aggressively building a robust emergency fund. Start with a manageable beginner goal of saving exactly one month of essential living expenses. Treat your monthly emergency fund contribution as a fixed, mandatory bill that you pay directly to yourself every single payday. Additionally, leaning heavily on sinking funds for predictable but irregular costs—like routine car maintenance and minor home repairs—effectively prevents those routine items from masquerading as catastrophic emergencies and derailing your hard work.

How do I get my partner on board with strict budgeting?

Financial friction inside a marriage frequently stems from a fundamental lack of shared goals. Instead of leading the conversation with harsh restrictions and immediate spending cuts, start the dialogue by discussing your shared, long-term dreams. Whether you desperately want to escape the crushing stress of living paycheck to paycheck, afford an annual family vacation, or comfortably support your aging parents without resentment, defining the clear why makes the difficult how much easier to swallow. Schedule regular, entirely judgment-free money meetings where both partners hold an equal voice in allocating funds and adjusting the budget to fit your shared household priorities.

Your Next Step Toward Financial Clarity

Regaining total control of your family cash flow requires decisive, immediate action rather than endless planning. You now possess the exact knowledge required to map your historical expenses, implement a proven financial system, and leverage powerful modern tools to keep your daily spending on track. More importantly, you deeply understand how to tap into crucial financial assistance programs that dramatically ease the heavy burden of multigenerational caregiving. Do not let this motivational momentum fade away. Your immediate assignment is to log into your primary bank account right now, download your most recent monthly statement, and rigorously highlight every single recurring subscription. Cancel just one digital service you no longer actively use, and immediately redirect that newly freed money toward your newly established emergency fund. This single, achievable victory sets the solid foundation for lasting financial peace.