Subscription creep drains your bank account silently each month, stealing hundreds of dollars you could channel toward debt payoff or a family vacation. You likely signed up for a free trial or an enticing introductory offer, only to completely forget about the recurring charge hiding deep within your credit card statement. Taking a hard look at your monthly outgo allows you to quickly reclaim that lost income without changing your core lifestyle. When you audit your cash flow and cancel the digital dead weight, you create immediate breathing room in your budget. Let us examine the ten most common recurring expenses draining middle-income households and explore concrete strategies to plug the leaks in your financial ship.

State of the Wallet: The Hidden Cost of Convenience

Middle-income households face mounting pressure from inflation and the rising cost of basic necessities. When you evaluate your monthly spending, you likely focus on the massive line items like your mortgage or grocery bill. However, smaller recurring charges inflict substantial damage because they operate entirely under the radar. Consumer research consistently reveals a massive disconnect between what Americans think they spend on digital services and what actually leaves their checking accounts each month.

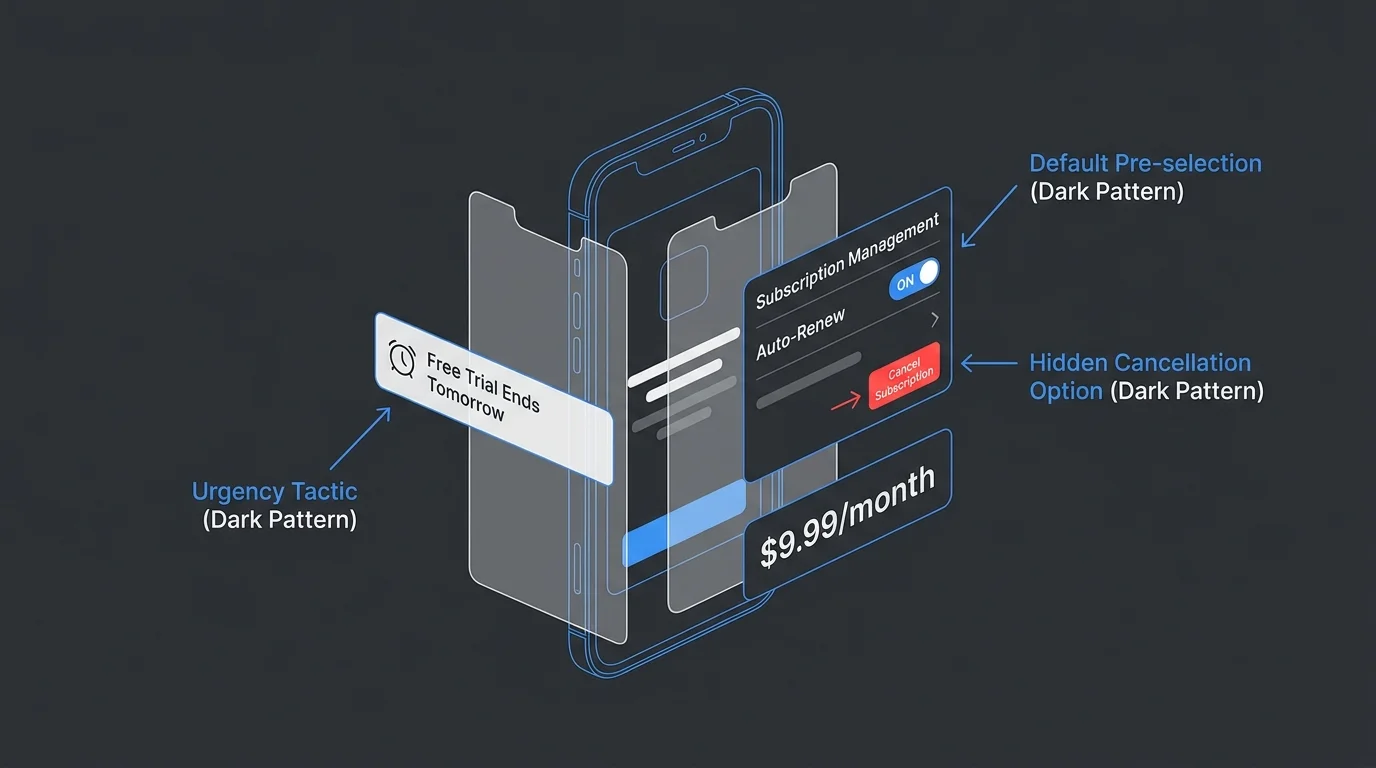

This phenomenon occurs because companies strategically design sign-up processes to be completely frictionless, while simultaneously making the cancellation process an arduous labyrinth. The Consumer Financial Protection Bureau highlights the impact of these dark patterns, noting how businesses intentionally trap consumers in recurring billing cycles. By auditing these hidden expenses, you regain absolute control over your money and redirect those funds toward your most pressing financial priorities.

Strategy Pillar One: The Great Cash-Flow Audit

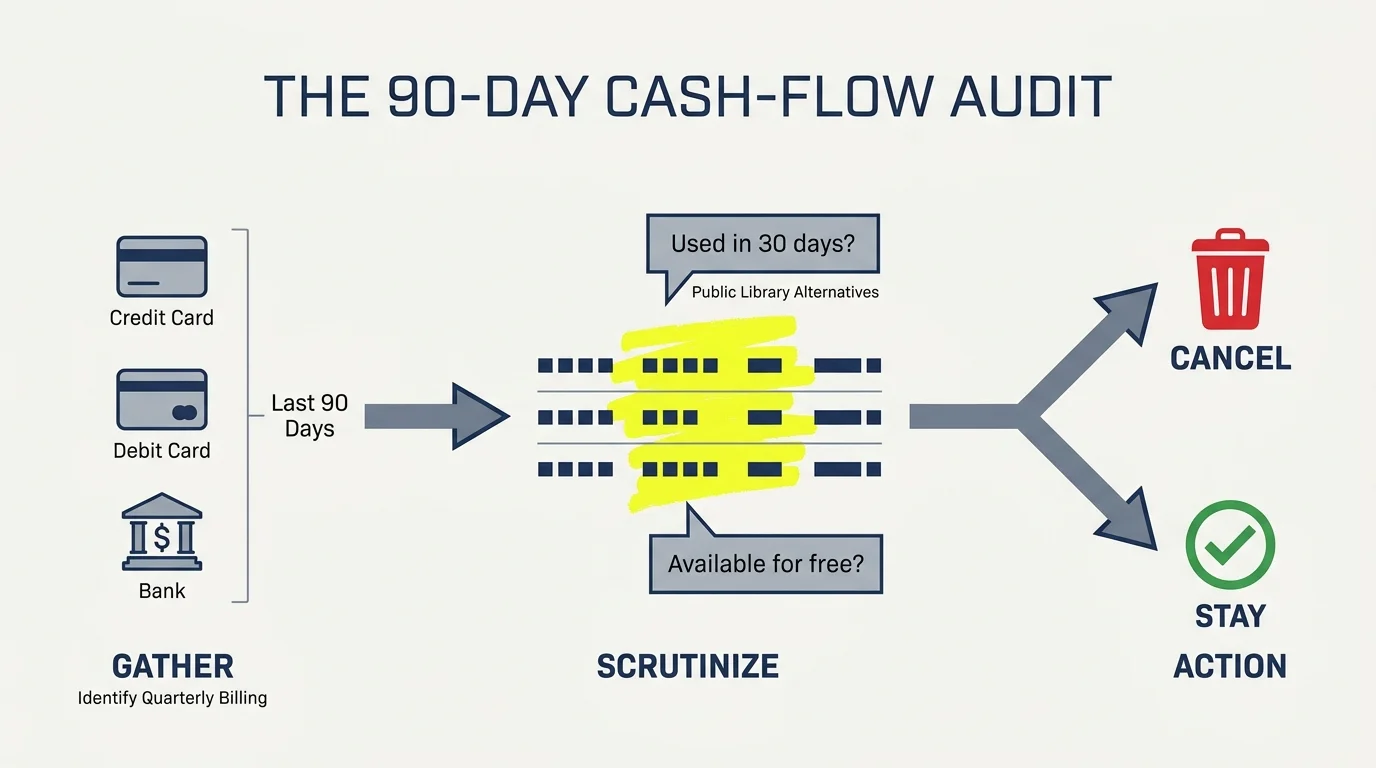

You cannot fix a budget deficit you refuse to acknowledge. Launching a comprehensive cash-flow audit serves as your primary defense against subscription bloat. Gather your credit card statements, debit card transactions, and bank account summaries spanning the previous ninety days. You must look back three full months because many digital software services bill on a quarterly basis, meaning a thirty-day review guarantees you will miss critical data points.

Grab a highlighter and ruthlessly scrutinize every line item. Ask yourself simple questions for each recurring charge. Did you use this service within the last thirty days? Can you access this exact same value for free through a public library or an ad-supported alternative? Identify the leaks immediately so you can staunch the bleeding and move toward a stronger financial foundation.

10 Subscription Bills Draining Your Budget

Every household maintains a unique digital footprint, but specific categories of recurring expenses consistently drain wallets across the country. Review the following ten culprits to see which ones silently extract wealth from your bank account.

1. The Forgotten Gym Membership

You signed up for a fitness club with excellent intentions, but your schedule became chaotic, and you stopped visiting. The facility continues pulling fifty dollars from your account every thirty days. You hesitate to cancel because it feels like abandoning your health goals. Acknowledge this sunk cost, cancel the unused membership today, and opt for free home workouts to stop the financial bleed.

2. Premium App Subscriptions

Smartphone applications actively prompt users to upgrade during moments of immediate need. You download a meditation app to calm your mind, agree to a free trial, and completely forget the commitment once your stress subsides. Dig into the subscription management settings on your mobile device to uncover and terminate the various tools quietly charging your linked credit card.

3. Overlapping Streaming Services

Cord-cutting promised massive savings, but you now pay for a half-dozen independent streaming platforms. You maintain active accounts for multiple services simultaneously, even though you realistically only possess the free time to watch one show. Keep one primary platform active for a month, binge the specific content you desire, cancel the service, and rotate to another provider.

4. Unused Cloud Storage Upgrades

Your smartphone constantly warns you about running out of photo storage, creating a persistent sense of false urgency. You authorize a monthly upgrade fee for additional gigabytes and eventually pay for redundant space across different tech ecosystems. Consolidate your digital files onto a single platform and regularly delete duplicate photos to stay securely within the free storage tiers.

5. Subscription Boxes That Pile Up

Meal kits and beauty samples provide a temporary burst of dopamine upon delivery. The novelty wears off rapidly, leaving you with a stockpile of unused cosmetic samples or ingredients you lack the energy to cook. These physical boxes represent highly expensive recurring charges. Evaluate your inventory of shipped goods. If you own a massive backlog, immediately pause the delivery service.

6. Credit Monitoring Services

When you apply for a mortgage, you frequently enroll in premium credit monitoring services out of sheer anxiety. You do not need to pay a monthly premium to view your financial data. Federal law entitles you to free weekly credit reports from the major bureaus, and many major credit card issuers provide excellent free score tracking directly within their mobile apps.

7. Auto-Renewing Software Licenses

You purchase premium productivity software, and companies quietly enroll you in auto-renewal programs that charge exorbitant rates twelve months later. Oftentimes, these unannounced renewal rates significantly exceed the promotional pricing originally offered to new customers. Always log into your software accounts immediately after a purchase and proactively toggle the auto-renew feature to the off position to protect your wallet.

8. Magazine and Digital News Paywalls

You hit a restrictive paywall while researching a topic, pay a promotional rate for temporary access, and completely ignore the fine print. You suddenly face a thirty-dollar monthly charge for a publication you never actually read. Check your local library, which routinely provides registered patrons with completely free digital access to major national newspapers and premium magazines.

9. Extended Warranties and Protection Plans

Retailers heavily push monthly protection plans on everything from smartphones to kitchen appliances. Manufacturer warranties and the automatic protections provided by major credit cards render most of these insurance plans completely redundant. Cancel these third-party subscriptions and funnel that exact same monthly amount into a dedicated emergency fund to confidently self-insure against unexpected hardware failures.

10. Identity Theft Protection Add-Ons

Fear-based marketing convinces many consumers to purchase expensive identity theft protection plans. You pay twenty dollars a month believing it creates a magical shield around your data. You can achieve far superior protection for absolute zero dollars by initiating a proactive security freeze on your credit files, making it incredibly difficult for identity thieves to open fraudulent accounts.

Strategy Pillar Two: Smarter Saving Automations

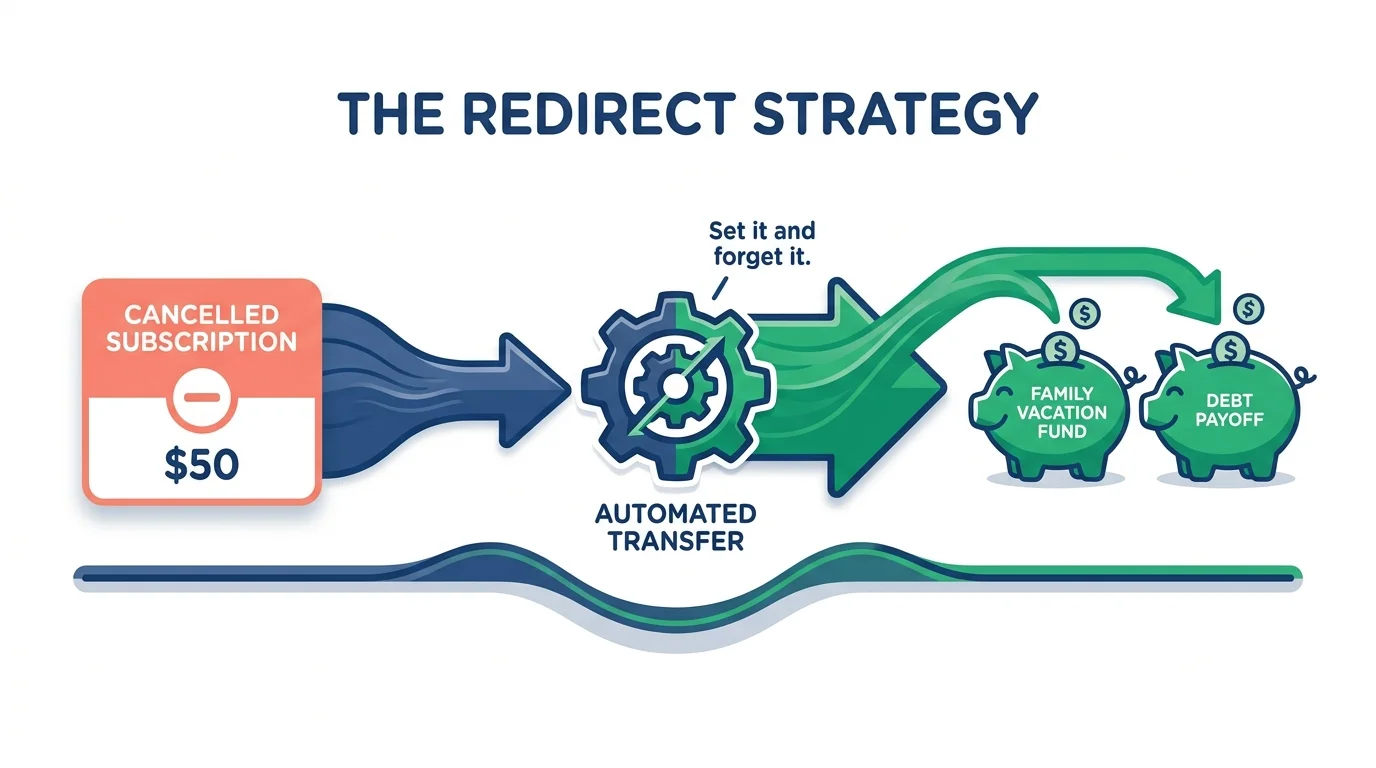

Canceling an unused service represents only the first phase of wealth building. If you merely eliminate a fifteen-dollar charge and leave the money sitting in your checking account, you will inevitably spend those funds on a random impulse purchase. You must actively capture the savings and give those reclaimed dollars a specific, highly productive job in your budget.

Establish an automated transfer from your primary checking account to a high-yield savings account. If you cancel sixty dollars worth of subscriptions, set up an automatic recurring transfer for sixty dollars on your designated payday. The Federal Reserve emphasizes the critical importance of emergency savings for overall household resilience, while institutions like Chase Bank recommend automating your savings to effectively remove the temptation of discretionary spending. Automating this process ensures your newly freed cash flow instantly strengthens your financial safety net.

Strategy Pillar Three: Mindful Spending and Managing Trials

You will inevitably want to test new digital services in the future, requiring a robust defensive strategy to prevent a financial relapse. Adopting mindful spending habits ensures you forever dictate the terms of your digital engagements. Whenever a company requires a credit card to activate a free trial, leverage virtual card numbers offered by major credit card issuers.

You can set specific expiration dates on these virtual cards. When the deceptive trial period ends and the merchant attempts to process a massive fee, the charge simply declines. Furthermore, establish a strict personal rule regarding calendar usage. The exact moment you sign up for any promotional offer, open your digital calendar and set an aggressive alert for two days before the renewal date.

Real-World Voices: What Behavioral Economists Say

Behavioral economists note that human beings suffer from strong status quo bias; we strongly prefer things to remain exactly as they are because making a change requires immediate cognitive effort. Subscription companies intentionally weaponize this natural human tendency to ensure continued revenue streams.

You continue paying for unused services because the perceived mental exhaustion of finding the cancellation portal heavily outweighs the immediate pain of the monthly charge. The Federal Trade Commission aggressively combats this exact issue through regulations requiring companies to make canceling a service just as easy as signing up. Push through the artificial friction and reclaim your agency over your finances.

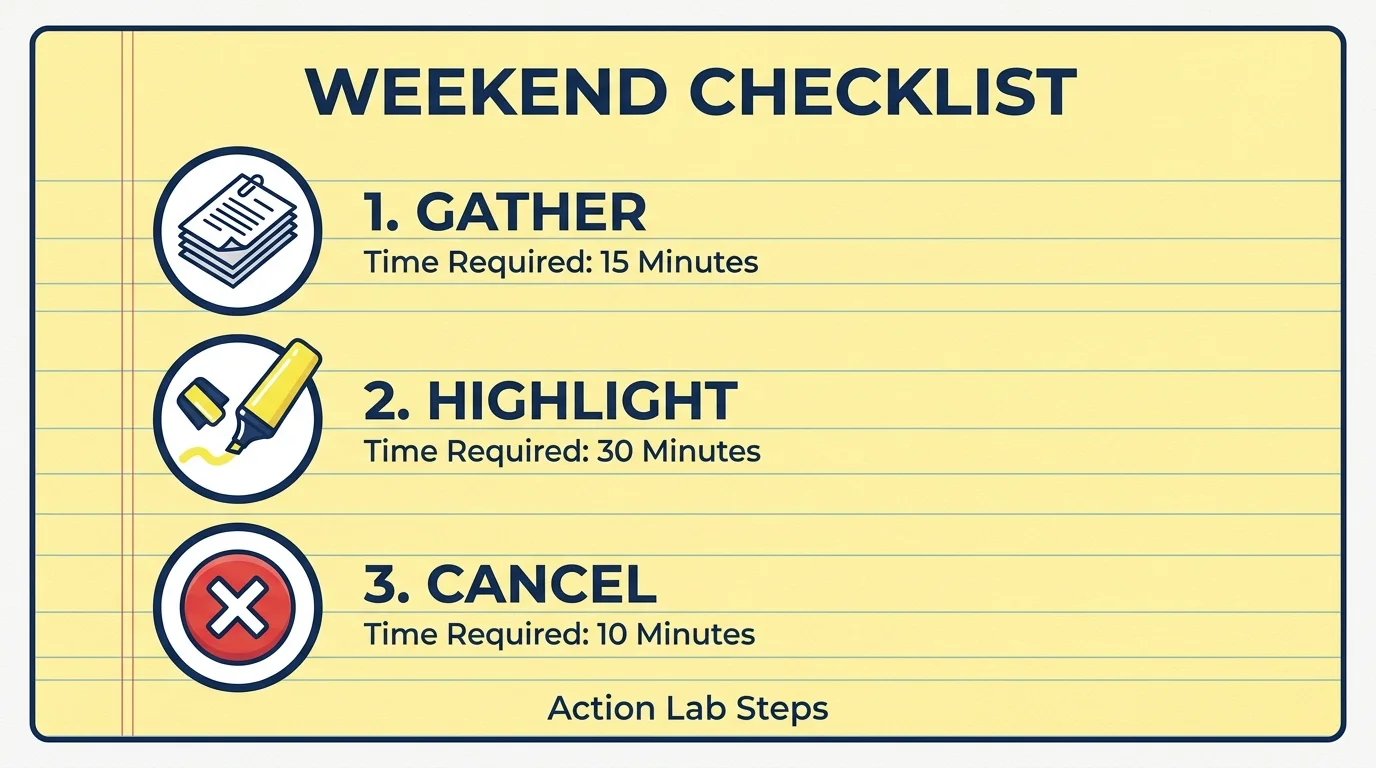

Action Lab: Your Weekend Budget Tweak

Theoretical knowledge holds absolutely no value unless you apply it immediately to your actual circumstances. Dedicate exactly thirty minutes this Saturday morning to execute a highly targeted budget tweak. Open your smartphone and navigate directly to your active subscriptions list within the primary settings menu.

Identify three services you have not actively utilized in the past fourteen days and cancel them without hesitation. Assume you cancel a premium weather app for five dollars, a secondary streaming platform for fifteen dollars, and an unused audio book credit system for fifteen dollars. You just reclaimed thirty-five dollars a month. Redirected into a basic investment account yielding a modest seven percent return, that seemingly insignificant cash flow compounds to over six thousand dollars in ten years.

Guardrails and Pitfalls: Avoiding the Relapse

As you actively prune your monthly expenses, watch out for hidden traps that can quickly derail your progress. The most significant mistake consumers make involves using a debit card for digital sign-ups. When you provide a debit card, a predatory subscription service can directly drain cash from your checking account, potentially triggering cascade overdraft fees and failed mortgage payments. Always use a standard credit card for recurring digital transactions to maintain a strong layer of fraud protection.

Additionally, do not ignore the massive savings potential hidden within family plans. If your household members pay individually for a premium music service, you bleed cash unnecessarily. Consolidate individual accounts into a single family plan to slash the per-person cost dramatically. Finally, beware of the pause button trap. Companies frequently encourage you to simply pause your subscription rather than executing a hard cancellation, which merely delays the inevitable expense.

Frequently Asked Questions About Subscription Management

Can a company legally refuse to let me cancel a subscription?

Companies cannot legally hold you hostage, but they frequently use obfuscation tactics to make the process incredibly frustrating. Federal law mandates that terms and conditions must be clear and conspicuous. If a company deliberately hides the cancellation mechanism or refuses to process a legitimate request, you possess the absolute right to contact your credit card issuer, declare the ongoing charges unauthorized, and initiate a formal billing dispute.

Will canceling a subscription improve my credit score?

Standard subscription services like streaming platforms, gym memberships, and digital magazines do not report your on-time payments to the major credit bureaus. Therefore, paying these bills provides zero direct benefit to your credit profile, and canceling them will not harm your score. However, redirecting the money saved from canceled subscriptions to pay down high-interest credit card debt will rapidly improve your credit utilization ratio, thereby boosting your score organically.

Should I use a third-party app to cancel my subscriptions?

Numerous financial technology applications offer to identify and cancel unwanted subscriptions on your behalf. While these tools offer undeniable convenience, they require you to surrender your highly sensitive banking credentials and extensive transaction history. Furthermore, some of these automated services charge a percentage of the money they successfully save you. You can achieve the exact same results manually for free by investing twenty minutes of focused effort.

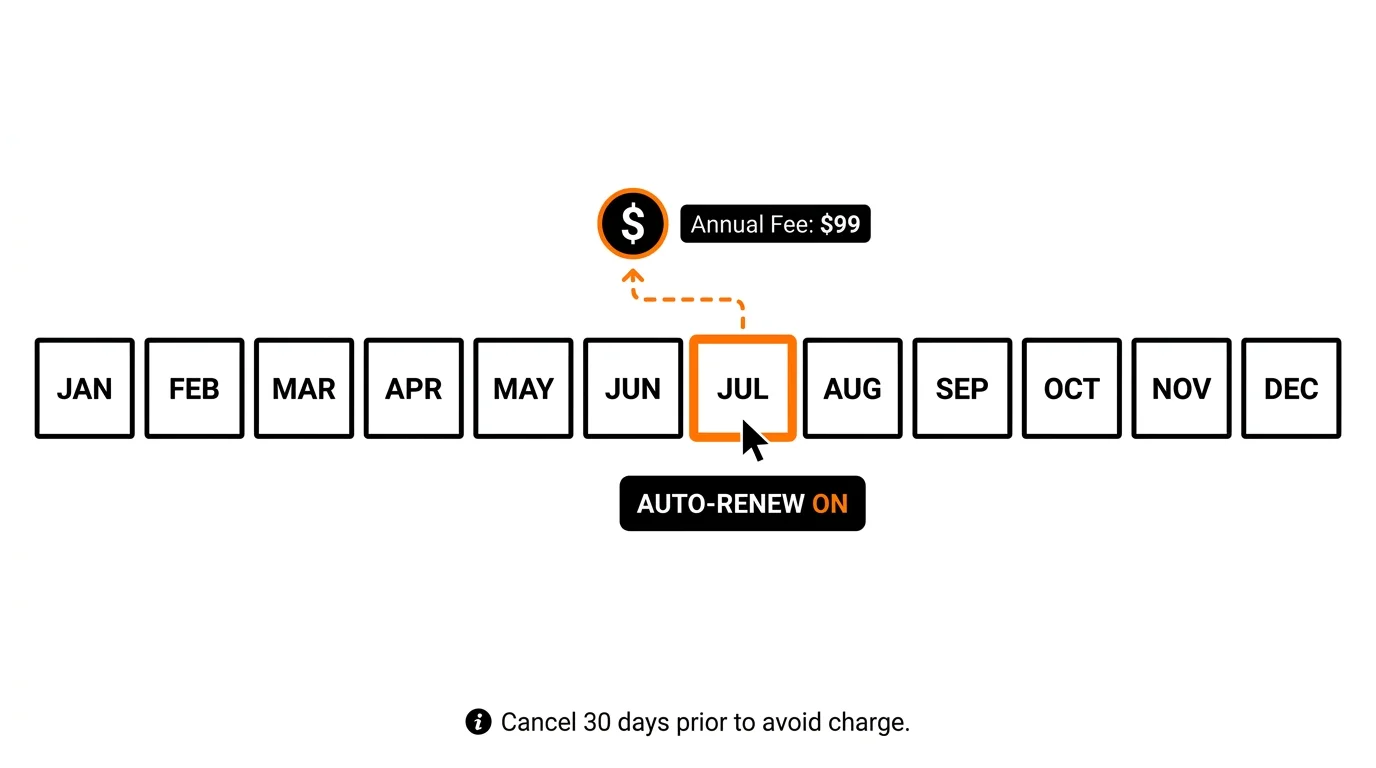

How do I handle annual subscriptions that just renewed?

If you miss a cancellation window and a massive annual charge hits your credit card statement, immediately contact customer service. Do not assume the money is permanently lost. If you reach out within twenty-four to forty-eight hours of the renewal date and firmly explain that you originally intended to cancel the account, many reputable companies will reverse the charge and issue a full refund to maintain goodwill.

Reclaim Your Financial Power

Managing your personal finances simply requires consistent attention to detail and a willingness to confront your actual spending behavior. Subscription bills rely entirely on your apathy to survive and multiply. By executing a thorough cash-flow audit and aggressively eliminating the digital dead weight, you instantly generate the extra capital needed to fund your true priorities. Take back your hard-earned money today. Dedicate half an hour this week to reviewing your credit card statements, cancel the services providing zero value to your life, and automate the newly found savings into an account that actively builds your future prosperity.