Recalibrating your spending habits puts real money back into your pocket tonight, allowing you to breathe easier when payday feels too far away. Surging living costs have quietly transformed manageable monthly bills into sources of deep financial stress for middle-income households across the country. You do not need to sacrifice your entire quality of life to build a reliable safety net. By intentionally targeting nine specific monthly expenses that millions of Americans are slashing right now, you regain immediate control over your household budget. Small, strategic cuts compound quickly into significant inflation savings, giving you the financial margin required to pay down debt, boost your emergency fund, and sleep better at night.

The State of the Household Wallet

Inflation might dominate the evening news cycle, but its true impact reveals itself exclusively inside your checking account. When the price of basic necessities climbs, the discretionary income you previously enjoyed shrinks rapidly, forcing difficult conversations around the kitchen table. According to a recent Federal Reserve survey on household economics, a significant portion of consumers cite rising prices as their primary financial challenge, prompting a widespread reevaluation of recurring outflows. You are currently navigating an economic environment where every dollar matters significantly more than it did three years ago.

Maintaining the exact same spending habits while prices surge inevitably leads to credit card reliance and depleted savings accounts. Acknowledging this stark reality represents your first necessary step toward long-term financial resilience. You must approach your household budget not as a restrictive, punishing cage, but as a dynamic tool specifically designed to protect your hard-earned wealth. By auditing exactly where your money flows automatically each month, you empower yourself to intercept that cash and redirect those funds toward goals that genuinely improve your stability.

Strategy Pillar One: Conducting a Cash-Flow Audit on Discretionary Subscriptions

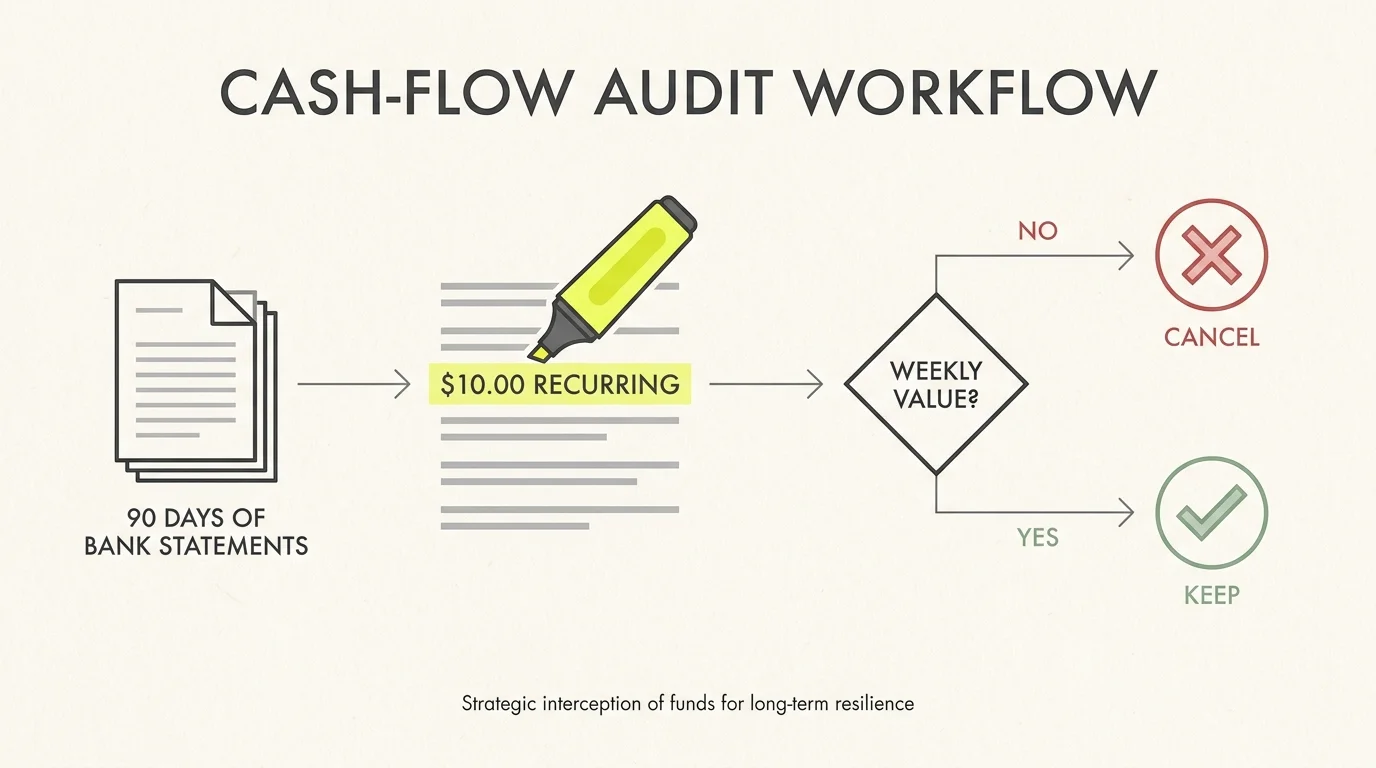

Your first line of defense against rapid lifestyle creep involves an aggressive cash-flow audit targeting discretionary subscriptions. Digital services and continuous memberships rely entirely on consumer inertia—the psychological tendency to ignore small recurring charges because canceling them feels like an overwhelming hassle. Giant corporations literally bank on you forgetting about that ten-dollar monthly fee. However; ten dollars extracted across five different services equals six hundred dollars removed from your pocket annually.

You must sit down with your last ninety days of bank statements and highlight every single recurring charge in bright ink. If a service does not bring you immediate, measurable value on a weekly basis, you must ruthlessly eliminate it. The Federal Trade Commission guidelines on auto-renewals emphasize your legal right to easily cancel unwanted services, so take full advantage of digital cancellation portals today.

1. Underused Streaming Services

Americans currently suffer from profound streaming fatigue. During the height of the pandemic, accumulating multiple entertainment platforms felt completely justified, yet today, most households consistently watch only one or two primary networks. You are likely paying for premium, ad-free tiers on platforms you have not actively opened in weeks. Savvy consumers now practice subscription churning—they subscribe to a single service to watch a specific highly anticipated show, finish the entire season, and immediately cancel the membership before the next billing cycle triggers. Adopting this rotational strategy instantly reduces your monthly bills without permanently depriving you of the premium entertainment you genuinely want to consume.

2. Ghost Gym Memberships

Corporate fitness centers engineer their entire business models around ghost members—well-intentioned people who pay monthly dues but never actually swipe their entry tags at the front desk. If you consistently find yourself driving past your gym rather than pulling into the parking lot, you are simply funding someone else’s daily workout. You can easily replace a costly boutique fitness membership with free community running clubs, inexpensive local recreation centers, or high-quality home workout routines readily available at no cost online. Cancel the guilt-inducing gym membership today; you maintain the freedom to rejoin later if your daily schedule and athletic motivation finally align.

3. Subscription Boxes and Curated Deliveries

Curated monthly boxes featuring gourmet snacks, premium pet toys, or specialized cosmetics offer a brief, powerful moment of dopamine upon delivery. Unfortunately, the novelty wears off rapidly—often after just three or four shipments—while the automatic billing continues indefinitely behind the scenes. You frequently end up hoarding unused boutique products that clutter your living space and drain your household budget simultaneously. Cutting these purely aesthetic subscriptions instantly frees up thirty to fifty dollars a month. If you truly desire a specific item featured in a promotional box, you can simply purchase it individually for a fraction of the burdensome annual subscription cost.

Strategy Pillar Two: Automating Savings by Negotiating Essential Bills

While you cannot entirely eliminate essential living expenses like shelter and communication, you absolutely possess the power to negotiate their monthly financial impact. Major service providers actively penalize their most loyal customers by slowly creeping up rates year after year, hoping you will blindly pay the inflated invoice rather than endure a tedious customer service phone call. You must immediately shed the costly misconception that utility and service rates remain permanently fixed.

By dedicating just one uninterrupted afternoon every six months to shopping around and threatening to leave for a direct competitor, you force these massive companies to offer you their lucrative, unadvertised retention rates. The ultimate goal here involves keeping the exact same high-quality service while drastically lowering your contractual financial obligation.

4. Premium Cell Phone Plans

Legacy telecommunications companies charge exorbitant, unnecessary premiums for unlimited data plans packed with obscure perks you likely never utilize. Millions of frugal consumers are currently slashing this exact expense by migrating their mobile service to Mobile Virtual Network Operators. These alternative, prepaid providers lease the exact same high-speed cellular towers as the major carriers but offer network access at roughly half the retail cost. Transitioning your entire family from a massive legacy carrier plan to a streamlined prepaid alternative frequently saves upward of one hundred dollars a month, delivering massive inflation savings without ever dropping a single phone call.

5. Escalating Auto Insurance Premiums

Auto insurance rates have skyrocketed across the nation recently, punishing perfectly safe drivers with unbelievably steep premium hikes. If you simply allow your existing policy to auto-renew every six months without questioning the rate, you are almost certainly leaving hundreds of dollars on the table. You should proactively request fresh quotes from multiple independent brokers annually to ensure you receive the absolute most competitive rate available in your zip code. Additionally, strongly consider utilizing National Association of Insurance Commissioners resources to understand how increasing your physical damage deductible from five hundred dollars to one thousand dollars drastically lowers your ongoing monthly premium, provided you keep an adequate emergency fund securely in place.

6. Expensive Meal Kit Services

Pre-portioned meal kits genuinely revolutionized weeknight cooking for busy professionals by eliminating tedious grocery store trips and meticulous meal planning. However, the extreme convenience premium baked into these delivery services completely destroys standard grocery budgets. When you calculate the exact cost per serving, you realize you frequently pay premium restaurant prices for raw food you still have to chop, cook, and clean up yourself. Everyday Americans are rapidly canceling these services en masse and returning to traditional grocery shopping. By utilizing free recipe applications and dedicating just one focused hour on Sunday afternoon to meal prep, you successfully replicate the convenience of a meal kit while cutting the associated food expense by more than half.

Strategy Pillar Three: Embracing Mindful Spending in Daily Habits

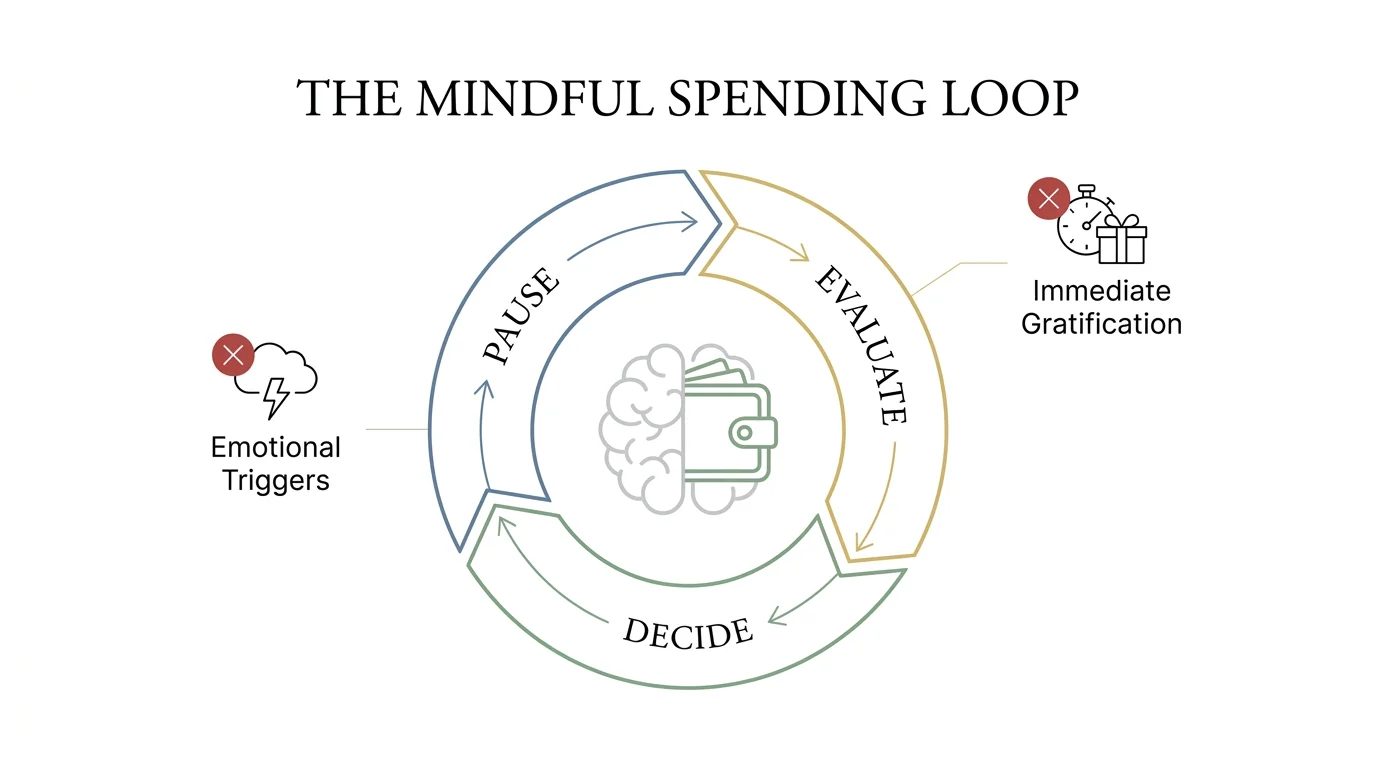

The final, most critical frontier in stretching your middle-income paycheck requires directly addressing your daily habitual spending. Small, repetitive, seemingly harmless transactions frequently fly completely under the radar of a traditional monthly budget spreadsheet, yet they represent the largest systemic leak in your financial foundation. Mindful spending does not mean you must permanently eliminate all joy and spontaneity from your daily routine; rather, it demands that you deliberately introduce intentional friction into your digital purchasing decisions.

When you force yourself to physically pause and evaluate the long-term financial cost of a fleeting convenience, you naturally redirect your capital toward meaningful activities that provide lasting satisfaction.

7. Frequent App-Based Food Delivery

Ordering a quick, hot dinner through a mobile delivery application feels like a harmless, highly deserved indulgence after an exhausting workday. Yet, when you heavily scrutinize the final digital receipt, you quickly discover that platform service fees, elevated hidden menu prices, and expected driver tips nearly double the actual retail cost of the meal. A fifteen-dollar local sandwich frequently transforms into a thirty-dollar major expense by the time it finally reaches your front porch. Deleting these frictionless delivery applications entirely from your smartphone removes the daily temptation instantly. If you truly want takeout food, force yourself to drive to the restaurant and pick it up; the added physical effort alone drastically reduces exactly how often you rely on commercial kitchens.

8. Name-Brand Grocery Purchases

Modern supermarket aisles are meticulously engineered by corporate psychologists to steer you directly toward heavily marketed, brightly colored name-brand products. Savvy shoppers are currently fighting back against grocery inflation by exclusively purchasing store-brand or generic alternatives for their heavily used pantry staples. The vast majority of private-label items—ranging from canned black beans to over-the-counter pain medication—are manufactured in the exact same industrial facilities as their expensive name-brand counterparts. Swapping your lifelong allegiance over to generic brands routinely shaves fifteen to twenty percent off your total grocery bill, offering you immediate and effortless cash savings right at the checkout register.

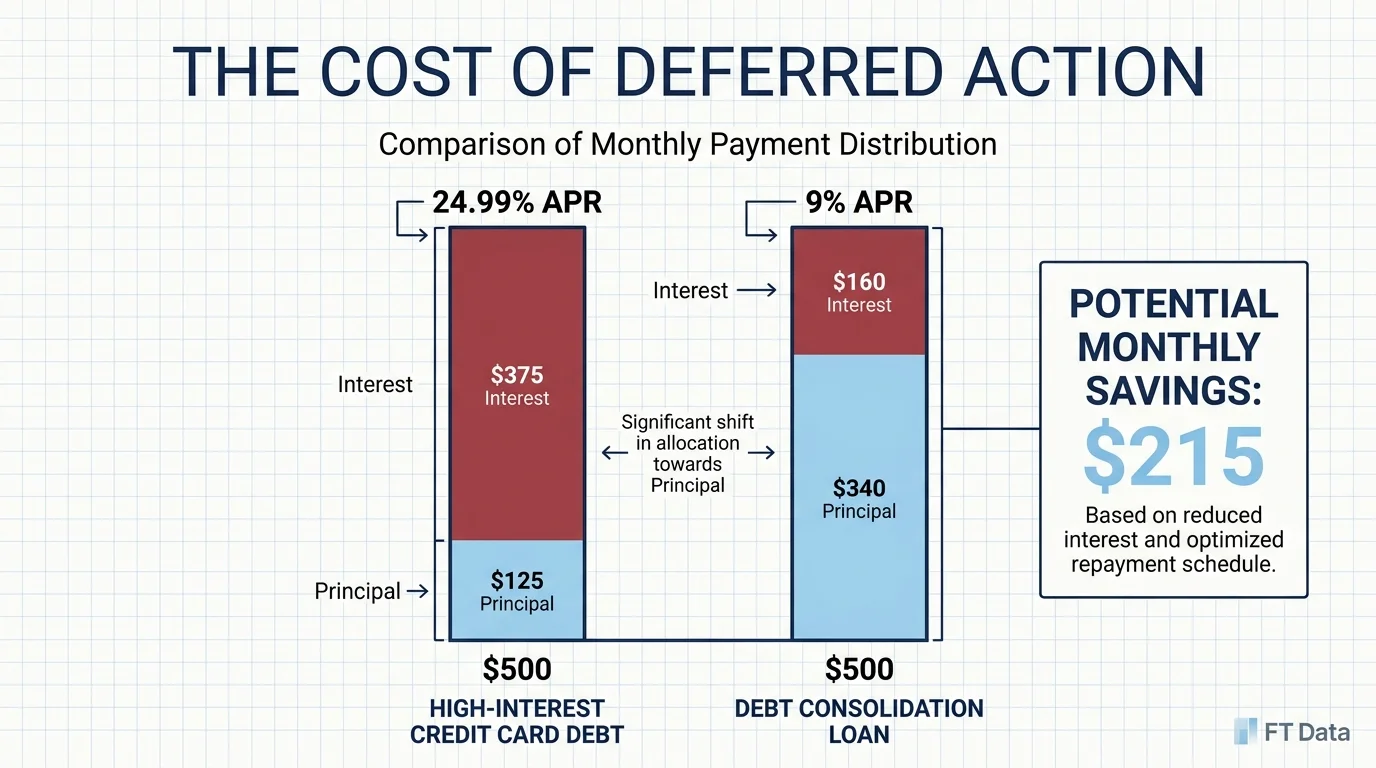

9. High-Interest Debt Payments

Carrying a revolving balance on a high-interest credit card guarantees that a significant portion of your monthly income vanishes straight toward predatory interest charges before you even begin paying down the actual principal. Viewing debt servicing as a permanent, non-negotiable monthly expense keeps you trapped endlessly in a vicious cycle of financial stress. You must actively work to aggressively reduce the carrying cost of this burden. According to Consumer Financial Protection Bureau reports on credit card balances, consolidating high-interest balances into a single, lower-interest personal loan or actively utilizing a zero-percent balance transfer promotion drastically reduces your monthly interest obligation. Lowering this underlying rate immediately frees up heavy cash flow that you can quickly redirect toward aggressively eliminating the debt altogether.

Real-World Voices: What Behavioral Economists Say About Cutting Expenses

Leading financial planners and prominent behavioral economists frequently study the invisible psychological barriers that completely prevent middle-income households from saving money. They constantly highlight a powerful academic concept known as the pain of paying. When you hand over physical paper cash for a standard purchase, your brain successfully registers a tangible, painful loss, naturally regulating your innate desire to spend. Modern digital commerce deliberately removes this necessary psychological pain by allowing you to purchase goods instantly with a single invisible click or a rapid biometric facial scan.

To permanently regain control over your bleeding household budget, financial experts strongly recommend actively reintroducing logistical friction into your daily financial life. You should immediately disconnect your primary credit cards from all mobile digital wallets and force yourself to manually type in your physical sixteen-digit card number for absolutely every online purchase. This tiny logistical hurdle gives your logical brain just enough time to successfully override your impulsive, emotional desires, ultimately preventing hundreds of dollars in entirely unnecessary purchases each and every month.

Action Lab: Execute Your Own Cash-Flow Tweak Tonight

Reading extensively about financial strategy means absolutely nothing if you do not pair that knowledge with immediate, decisive action. Tonight, you can execute a remarkably simple budget tweak that instantly improves your monthly margins. First, open your laptop and load your primary checking account dashboard. Set the calendar date range to clearly display your cleared transactions from the past thirty days. Next, grab a physical paper notepad and write down the exact corporate name and exact dollar amount of every single recurring subscription or utility payment you spot.

Once you build this comprehensive master list, highlight the single largest discretionary bill—perhaps a bloated premium cable package or an underutilized boutique gym membership. Pick up your smartphone immediately and call the customer retention department directly for that specific company. Clearly inform the representative that you are strictly auditing your household budget and unfortunately need to cancel your service entirely due to escalating costs. In the vast majority of cases, the representative will instantly offer you a heavily discounted retention rate simply to keep your business active. If they offer a lower price, cheerfully accept it and enjoy the effortless savings; if they process the cancellation instead, you successfully removed a heavy financial burden from your monthly obligations.

Guardrails and Pitfalls to Avoid While Trimming Expenses

Intense enthusiasm for cutting expenses frequently leads well-intentioned individuals to slash their budgets way too aggressively, creating a highly unsustainable lifestyle that practically guarantees long-term failure. Financial starvation predictably triggers massive budget burnout. If you completely strip away every single non-essential pleasure—abruptly canceling your streaming services, eliminating all restaurant visits, and denying yourself basic weekend hobbies—you will inevitably snap and binge-spend out of sheer psychological frustration. You must deliberately build a small, guilt-free entertainment allowance into your new lean budget to keep yourself sane.

Furthermore, you must absolutely never cut expenses related to necessary, preventative maintenance. Skipping your routine bi-annual dental cleanings or intentionally delaying an essential oil change for your primary vehicle might briefly save you a hundred dollars today, but it virtually guarantees a catastrophic, multi-thousand-dollar emergency expense next year. Smart frugality explicitly involves efficiently cutting the fat from your budget without ever compromising the vital structural integrity of your health, your home, or your daily transportation.

Frequently Asked Questions About Inflation Savings

How do I identify phantom subscriptions on my credit card statement?

Phantom subscriptions frequently hide behind highly confusing, abbreviated merchant names or process quietly through third-party digital payment platforms, making them incredibly difficult to spot during a quick, casual glance. To successfully uncover these hidden financial drains, you should physically print out your monthly statement and carefully cross-reference every unknown charge using a standard internet search engine. Additionally, several highly reputable budgeting applications securely scan your historical transaction data to flag recurring billing patterns, giving you a clear, centralized dashboard of your active, forgotten subscriptions.

Will canceling my credit cards to save money hurt my credit score?

Closing an active, long-standing credit card account absolutely possesses the potential to lower your formal credit score by immediately reducing your total available credit limit and effectively shortening your average account age history. If you desperately want to stop spending on a specific card without damaging your hard-earned credit profile, you should simply cut the physical plastic card into tiny pieces and permanently delete the saved card details from your various digital devices. This highly effective strategy successfully removes your immediate ability to spend impulsively while keeping the valuable credit line officially open and active on your formal credit report.

What is the fastest way to lower a recurring utility bill?

The absolute quickest method for significantly reducing a massive utility bill involves conducting a thorough, self-guided home energy audit to address immediate physical inefficiencies. Lowering your basement water heater temperature by just ten degrees, sealing your drafty living room windows with highly inexpensive weather stripping, and swapping out legacy incandescent light bulbs for modern energy-efficient LED alternatives immediately decreases your baseline monthly power consumption. You should also proactively contact your local utility provider to inquire directly about budget billing programs, which strategically average out your annual usage to completely prevent massive, unexpected billing spikes during extreme winter or summer weather months.

How much of my income should ideally go toward fixed monthly expenses?

Dedicated financial professionals widely endorse the fifty-thirty-twenty budgeting framework as a highly effective, reliable baseline for standard middle-income households. Under this specific model, you should actively aim to allocate absolutely no more than fifty percent of your net take-home pay toward fixed, essential expenses, strictly including your housing, core utilities, basic groceries, and required insurance. If your required monthly bills currently consume sixty or seventy percent of your take-home pay, you remain incredibly vulnerable to sudden economic shocks, meaning you must aggressively pursue the negotiation and elimination strategies outlined above to quickly restore structural balance to your life.

Keep Moving Forward

Transforming your daily financial reality inherently requires deep patience, fierce discipline, and a brave willingness to confront your daily spending habits with total, unwavering honesty. The intense macroeconomic pressures currently squeezing your weekly paycheck are undeniably real, but you always retain the ultimate authority over exactly how your hard-earned dollars are successfully deployed. Every single unused subscription you courageously cancel, every escalating utility rate you successfully negotiate down, and every highly mindful purchase you make actively serves as a powerful declaration of your ongoing financial independence. Do not attempt to flawlessly overhaul your entire life in a single exhausting weekend; instead, consciously target just one or two specific expenses from this comprehensive guide tonight. As you clearly witness the extra cash safely accumulating in your checking account month after month, your initial economic anxiety will seamlessly transform into profound, unshakeable financial confidence. You already possess the precise tools required to rigorously protect your household; now, you must take the decisive first step.