Reclaiming hundreds of dollars each year requires tracking down the stealthy surcharges draining your hard-earned paycheck. You can immediately boost your monthly cash flow by exposing and eliminating the hidden fees lurking inside your everyday services. Middle-income households often lose significant portions of their budget to minor charges disguised as administrative costs, convenience fees, or unavoidable taxes. These subtle leaks slowly erode your financial security and delay your long-term goals. By understanding exactly where businesses hide these extra expenses, you gain the power to stop the outflow. Securing your savings demands a sharper eye and a proactive approach to your daily transactions.

The Invisible Drain on Your Paycheck

Modern consumers navigate a minefield of deceptive pricing structures. Companies increasingly advertise an artificially low base price to capture your attention, only to inflate the final bill with mandatory surcharges at checkout. This practice—often referred to as drip pricing—frustrates budget-conscious shoppers and obscures the true cost of living. When you calculate your monthly expenses based on advertised rates rather than final receipts, your budget inevitably falls short. You might blame yourself for overspending, yet the real culprit often lies buried in the fine print of your monthly statements.

Federal regulators estimate that Americans pay tens of billions of dollars annually in unnecessary junk fees. These predatory charges disproportionately affect middle-income families striving to balance rising grocery bills with stagnant wage growth. As inflation pressures household budgets, corporations leverage administrative surcharges to maintain their profit margins without announcing formal price hikes. Recognizing this economic reality empowers you to fight back; you can shield your wealth by treating fee avoidance as a fundamental component of your personal finance strategy.

Ten Hidden Fees Sabotaging Your Budget

The Banking Maintenance and Overdraft Trap

Traditional banks frequently penalize customers for the very act of holding an account. Monthly maintenance fees activate when your balance drops below an arbitrary threshold or your direct deposits fall short of a mandated minimum. Furthermore, overdraft protection programs often function as expensive short-term loans, triggering massive penalties for a transaction that exceeds your balance by just a few cents. You can bypass these expenses by migrating your funds to an online-only institution or a local credit union that guarantees truly free checking.

Resort and Destination Charges in Travel

Hospitality conglomerates routinely strip essential amenities from their nightly rates to appear competitive on travel search engines. Upon arrival, front desk agents inform you of a mandatory daily resort fee covering internet access, pool towels, and fitness center entry—services you likely assumed the base rate included. You must always read the final pricing breakdown before confirming a non-refundable reservation. Calling the property directly allows you to negotiate or request a fee waiver, especially if you possess elite status within their loyalty program.

Delivery App Service and Small Order Surcharges

Ordering a quick meal through a smartphone application introduces a cascade of unexpected costs. Beyond the delivery charge and the driver tip, platforms impose ambiguous service fees that scale dynamically with your order subtotal. Moreover, ordering dinner for one often triggers a small order penalty. Restaurants also inflate their in-app menu prices to offset the heavy commissions charged by the delivery network. Picking up your food directly from the restaurant entirely eliminates this multi-layered pricing scheme.

Telecom and Internet Administrative Costs

Your monthly telecommunications bill likely features a densely packed section labeled taxes and surcharges. While government taxes remain unavoidable, internet service providers deliberately invent administrative cost recovery fees to pass their internal operating expenses onto you. These line items look official, yet they represent purely discretionary price increases. You hold the leverage to call the customer retention department and demand the removal of these specific charges, threatening to switch providers if they refuse your request.

Subscription Auto-Renewal and Processing Fees

Digital subscriptions drain your resources through inertia. Streaming platforms, digital magazines, and software providers rely on auto-renewal clauses buried in their terms of service. When a free trial expires, the company instantly bills your linked credit card—sometimes adding a payment processing fee for the transaction. You must aggressively monitor your recurring subscriptions. Setting immediate calendar alerts the moment you activate a trial ensures you cancel the service before the introductory period evaporates.

Event Ticketing Convenience Surcharges

Securing access to live music or sporting events exposes you to monopolistic pricing tactics. Ticketing platforms dominate the market, allowing them to attach exorbitant convenience fees, order processing charges, and facility facility fees to every transaction. These add-ons frequently inflate the face value of a ticket by thirty percent or more. While bypassing digital platforms entirely proves difficult, purchasing tickets directly from the venue box office often circumvents the heaviest online processing penalties.

Airline Seat Selection and Baggage Drip Pricing

Aviation pricing structures prioritize unbundling. Budget airlines—and increasingly legacy carriers—sell a basic economy fare that guarantees nothing beyond physical transit. Selecting a seat next to your spouse incurs a fee; placing a bag in the overhead bin triggers another charge. You must calculate the fully loaded cost of your journey before purchasing a ticket. Frequently, upgrading to a standard economy fare costs less than purchasing a basic ticket and adding the necessary services piecemeal.

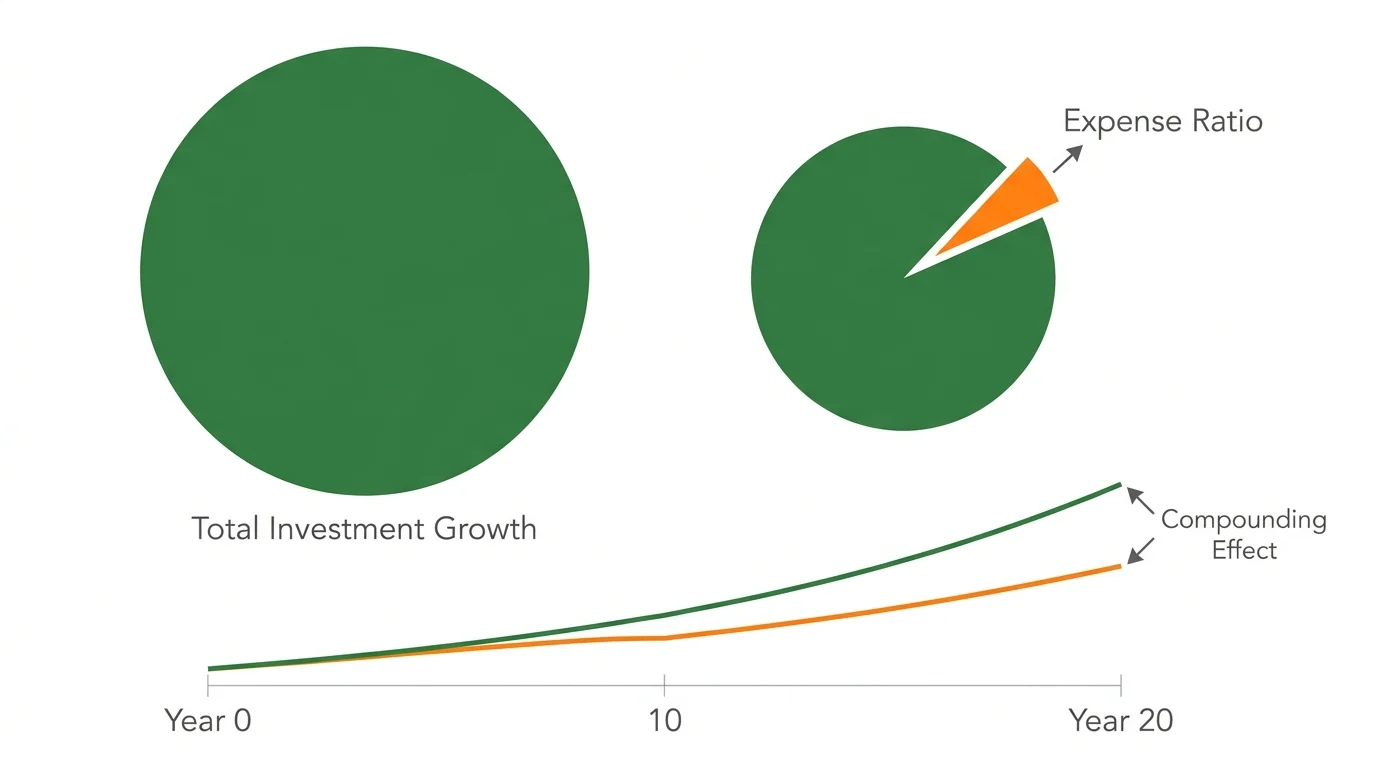

Investment Account Expense Ratios

Wall Street subtly extracts wealth from your retirement portfolio through internal fund fees known as expense ratios. Mutual funds deduct these percentages directly from your investment returns, making the transaction virtually invisible on your monthly statements. A one percent management fee sounds insignificant, yet it compounds over decades, potentially devouring hundreds of thousands of dollars from your final nest egg. Shifting your capital into low-cost index funds minimizes these expenses and accelerates your path to financial independence.

* “Paperclips chain a torn membership card to a contract, highlighting the sting of early termination penalties.”

* 1: Paperclips

*

Early Termination Penalties

Gymnasiums, cell phone carriers, and alarm system providers trap consumers in multi-year agreements backed by harsh cancellation policies. If you need to relocate or simply desire a better service, invoking your right to cancel activates an early termination fee that can exceed the cost of remaining in the contract. You must scrutinize the cancellation terms before signing any long-term agreement. Opting for month-to-month contracts protects your financial flexibility, even if the monthly rate appears slightly higher.

Inactivity Fees on Financial Products

Forgotten assets still cost you money. Prepaid debit cards, flexible spending accounts, and legacy brokerage platforms occasionally deploy inactivity fees. If you leave an account dormant for twelve consecutive months, the institution begins siphoning a monthly maintenance charge until the balance reaches zero. You must consolidate your financial accounts and close obsolete debit cards to protect your remaining capital from these quiet deductions.

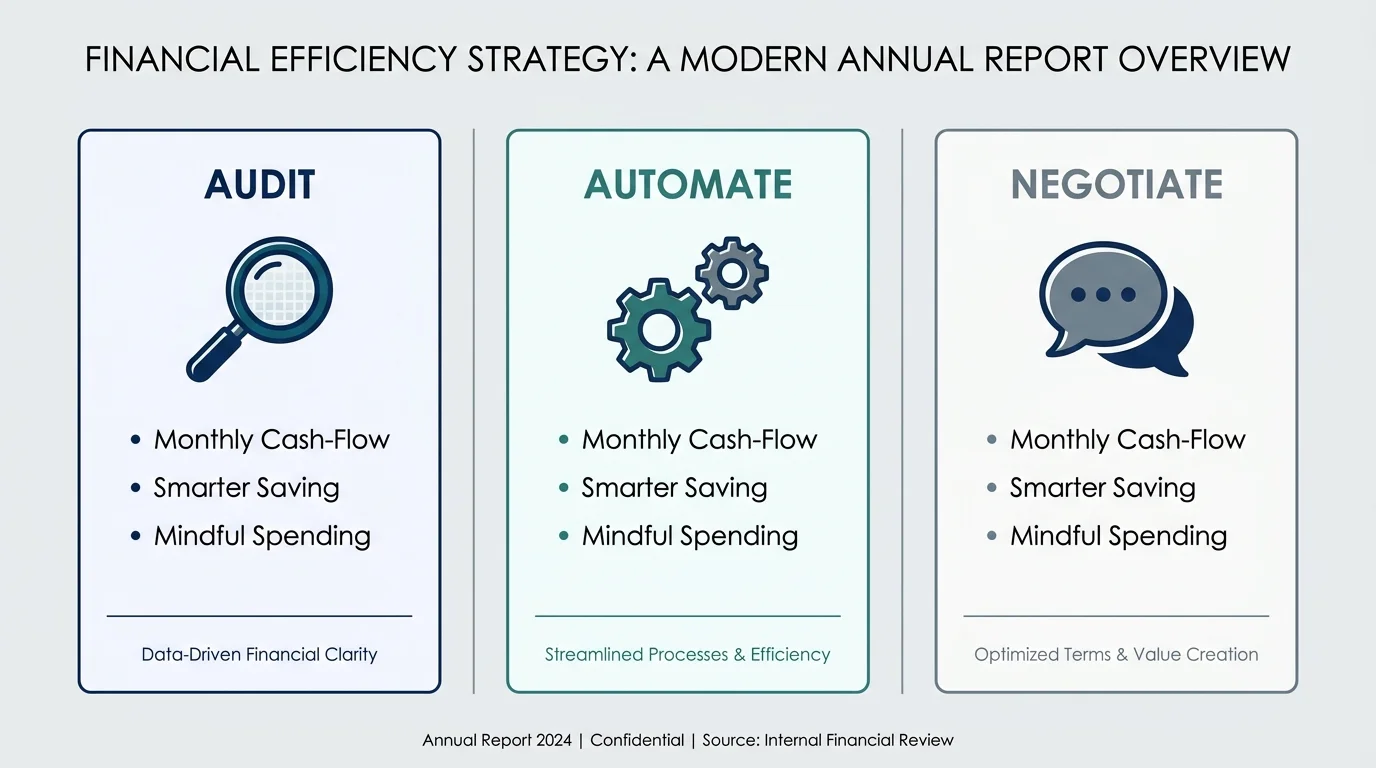

Strategy Pillars to Plug the Leaks

Conduct a Monthly Cash-Flow Audit

Ignorance serves as the lifeblood of the hidden fee economy. You must perform a rigorous cash-flow audit on the first weekend of every month. Print out your credit card and checking account statements—physical paper forces a deeper level of cognitive engagement—and highlight every charge under ten dollars. These micro-transactions usually house the administrative surcharges and forgotten subscriptions draining your resources. Tracking these expenses illuminates patterns you otherwise overlook during your busy workweek.

Deploy Smarter Saving Automations

Technology provides an exceptional defense against behavioral pricing traps. You should configure robust alert systems within your mobile banking application. Set your account to text you whenever your balance drops below two hundred dollars; this single action virtually eliminates accidental overdraft fees. Additionally, utilize virtual credit cards with strict spending limits when signing up for digital free trials. If the merchant attempts to process an unexpected renewal fee, the virtual card declines the transaction and protects your core bank account.

Practice Mindful Spending and Negotiation

Silence guarantees you pay the maximum possible price. You possess immense power as a consumer, provided you muster the courage to ask for a better deal. When you spot an unfamiliar line item on a medical bill or a utility invoice, call the billing department immediately. Representatives possess broad discretionary authority to waive late fees and remove administrative surcharges for polite, persistent customers. Combining this proactive negotiation tactic with a mandatory twenty-four-hour waiting period before utilizing premium convenience services sharply reduces your reliance on fee-laden platforms.

Real-World Voices: What the Experts Say

Behavioral economists emphasize that corporate pricing models exploit human psychology. Consumers experience decision fatigue during complex transactions; by the time an airline presents the final baggage fee, the buyer feels too committed to abandon the purchase. Financial planners combat this by advocating for zero-based budgeting, a system where every dollar receives a specific assignment before the month begins. Experts universally agree that simplifying your financial ecosystem—consolidating bank accounts, canceling redundant streaming services, and utilizing emergency savings research to plan for the unexpected—drastically reduces the surface area where companies can attach surprise charges.

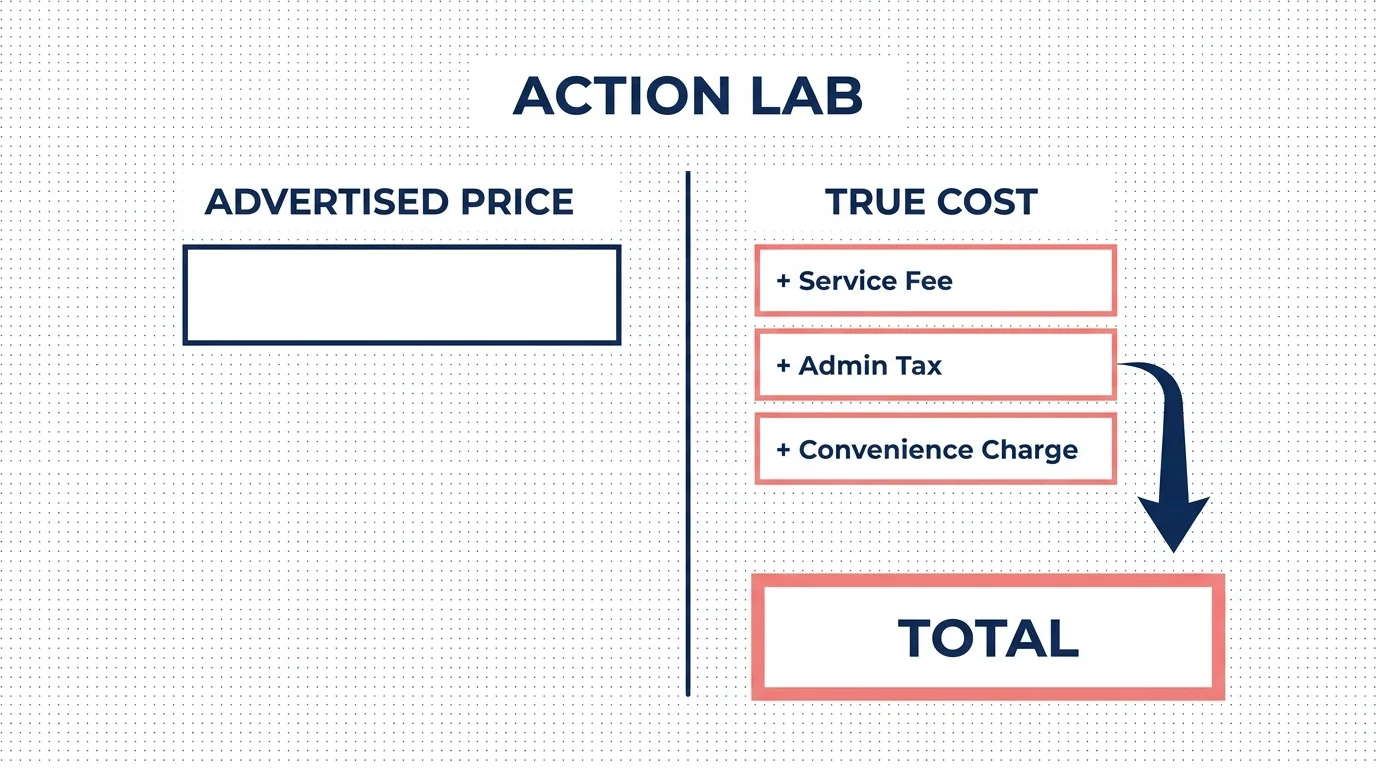

Action Lab: Calculating Your True Costs

Let us examine a routine Friday evening takeout order to reveal the compounding nature of convenience fees. You browse a delivery application and select a twenty-dollar artisan pizza. When you proceed to checkout, the platform adds a four-dollar delivery fee, a three-dollar service charge, and a two-dollar small order penalty. After applying a customary five-dollar driver tip, your twenty-dollar meal suddenly demands thirty-four dollars from your checking account. By driving ten minutes to retrieve the pizza yourself, you save fourteen dollars. If you redirect that weekly fourteen-dollar savings into an investment account earning a modest seven percent return, you accumulate over ten thousand dollars in a decade. Translating immediate convenience into long-term wealth powerfully reframes your daily spending decisions.

Guardrails and Pitfalls to Avoid

While eliminating unnecessary expenses accelerates your financial goals, you must avoid the frugality trap. Do not spend three hours battling a customer service representative over a one-dollar discrepancy; your time holds immense value, and misallocating it generates unnecessary stress. Furthermore, exercise extreme caution when migrating to financial platforms that advertise zero fees. Corporations must generate revenue; if an application offers completely free services, they likely package and sell your transaction data to third-party marketers. Always investigate regulatory guidance regarding how alternative financial technology companies monetize their user base before transferring your primary direct deposits.

Frequently Asked Questions

Can I negotiate everyday utility and telecom fees?

Yes; you hold more leverage than you realize. Customer retention departments possess discretionary power to waive setup fees, activation charges, and administrative costs. You achieve the best results by researching competitor rates and politely threatening to cancel your service if your current provider refuses to match the lower pricing structure.

Are hotel resort fees legally binding if I do not use the amenities?

Generally, courts consider these fees legally binding provided the property disclosed them during the booking process. However, hotels frequently waive these charges for guests who ask directly at the front desk, especially if a specific amenity—such as the fitness center or the pool—remains closed for maintenance during your stay.

Do fee-tracking smartphone applications actually work?

These applications provide excellent visibility into your subscription habits, but they require significant trade-offs. You must link your sensitive banking credentials to their platform, and many of these services take a percentage of the refunds they negotiate on your behalf. Manual auditing with a spreadsheet remains the most secure and cost-effective tracking method.

How do I find the true expense ratio of my mutual funds?

You must proactively search for the specific ticker symbol of your mutual fund on your brokerage platform. Navigate to the fund profile and locate the prospectus document; the expense ratio will be listed under the fees and expenses section. Replacing high-cost actively managed funds with broad market index funds instantly reduces this hidden tax on your wealth.

Reclaim Your Spending Power

Your financial trajectory changes the moment you stop accepting arbitrary charges as the standard cost of modern life. Auditing your transactions and confronting businesses about deceptive pricing demands effort, but the immediate return on your investment justifies the discomfort. You hold the authority to direct your income toward your family, your passions, and your retirement rather than padding corporate profit margins. Challenge yourself to locate and eliminate just one recurring fee this weekend. That single victory builds the momentum you need to completely overhaul your budget and secure the financial peace of mind you deserve.