You can reclaim hundreds of dollars a month by optimizing the household services you already pay for, turning financial stress into breathing room. When an unexpected car repair hits the same week your teenager empties a newly restocked refrigerator and the electric bill spikes to an all-time high, panic sets in quickly. Managing a home operates exactly like running a small business, requiring ruthless efficiency and strategic oversight. By treating your recurring monthly bills as negotiable contracts rather than fixed realities, you take immediate control of your cash flow. This guide dismantles nine specific household expenses, offering immediate tactics to trim the fat without sacrificing your family’s comfort, security, or daily quality of life.

Conducting a Comprehensive Spending Audit

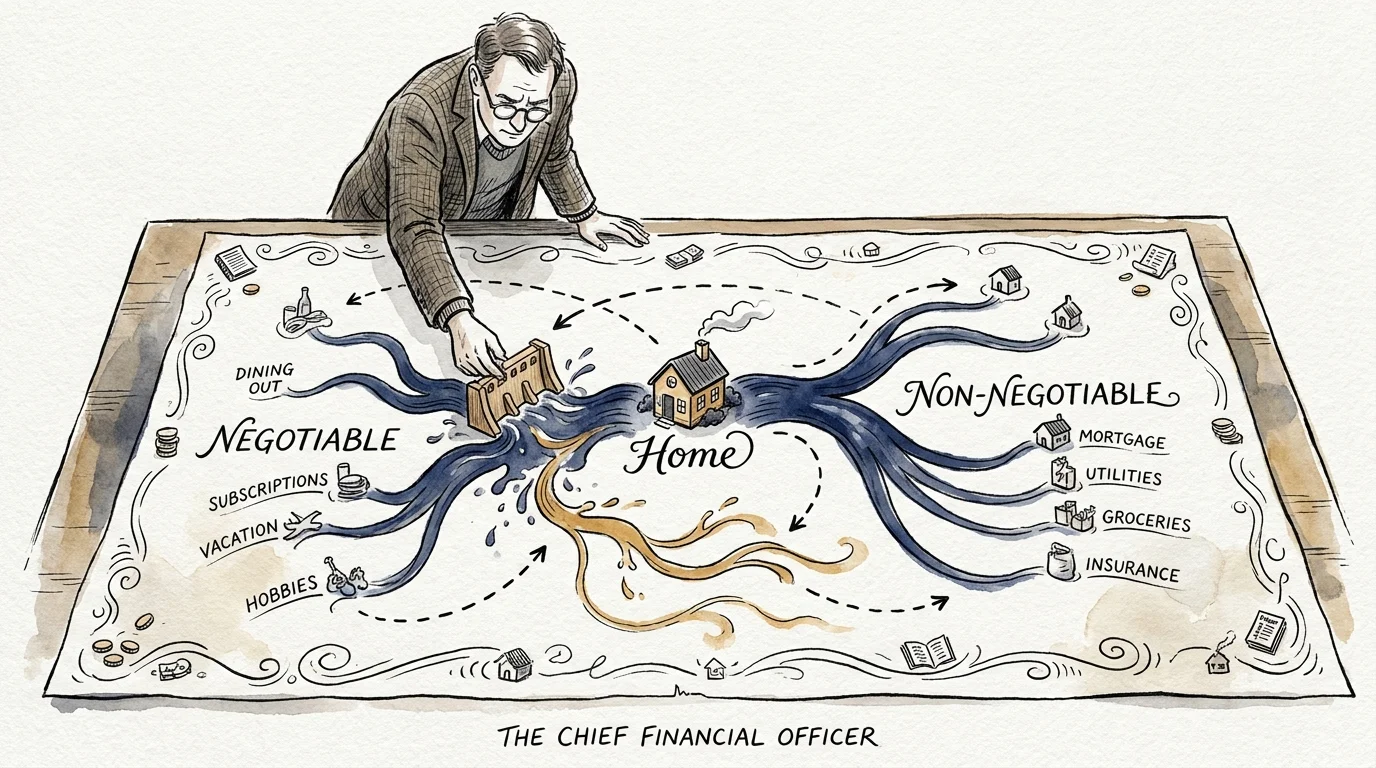

Before you can negotiate lower rates or slash unnecessary services, you must map exactly where your money flows each month. A spending audit removes the guesswork from household management; it forces you to confront the slow drip of subscription creep and the silent drain of inefficient utilities. Start by downloading your past three months of bank and credit card statements, highlighting every recurring charge you spot. Separate these expenses into two distinct categories: negotiable and non-negotiable. Your mortgage or rent represents a relatively fixed, non-negotiable cost, whereas electricity, internet, groceries, and insurance premiums fluctuate based on usage and provider pricing. For a family of four, simply writing out these expenses often reveals hundreds of dollars lost to services nobody uses anymore. Treat this exercise as a corporate financial review—you are the chief financial officer of your home, and your mandate is to maximize operational efficiency while protecting your bottom line.

Efficiency Upgrades: 9 Bills You Can Cut Right Now

1. Electricity and Power

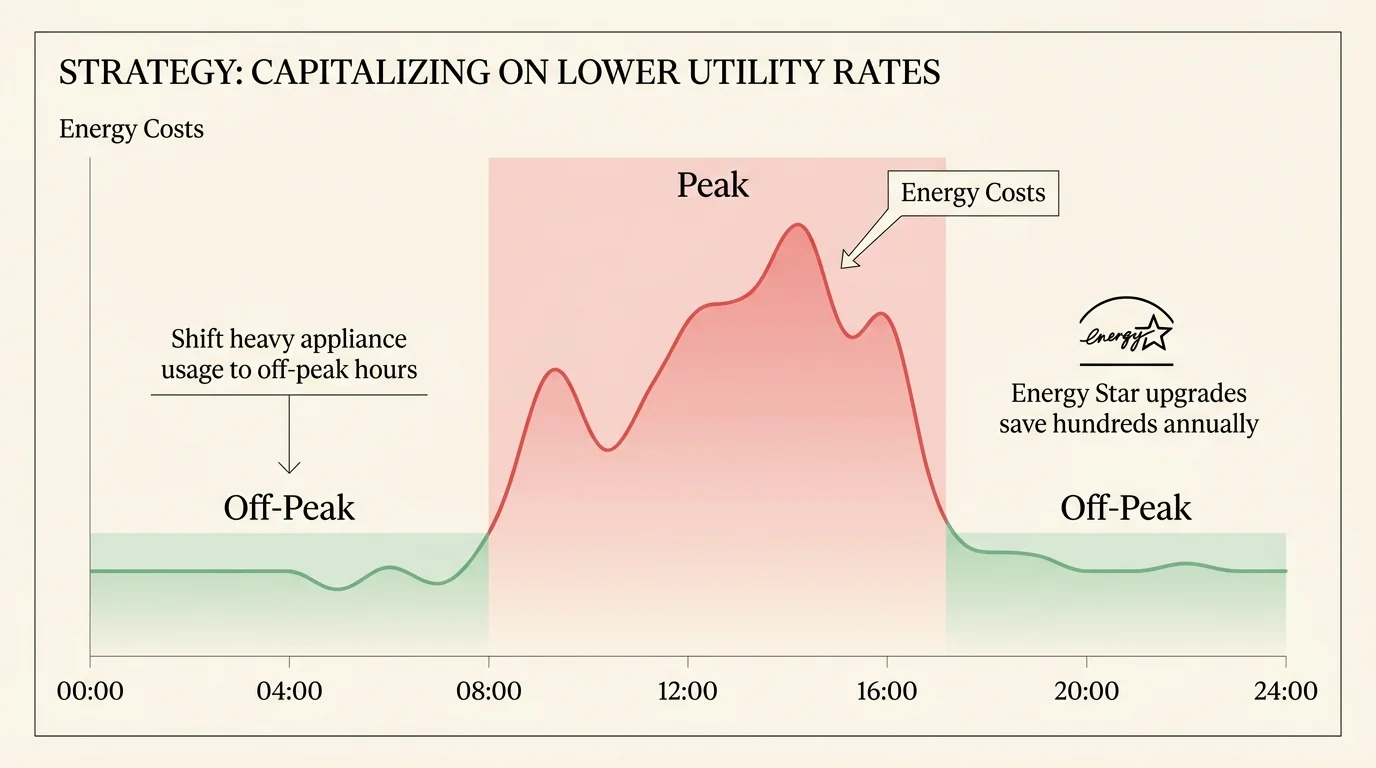

Your power bill rarely reflects a fixed rate, meaning behavioral changes and minor physical upgrades yield immediate dividends. Swapping out aging incandescent bulbs and sealing drafty windows drastically reduces your heating and cooling load. According to Energy Star guidelines for home upgrades, families save hundreds annually by programming thermostats efficiently and utilizing smart power strips. If you live in a multigenerational household where someone is always home, shift heavy appliance usage to off-peak hours to capitalize on lower utility rates provided by many regional energy companies.

2. Municipal Water and Sewer

Water conservation goes far beyond taking shorter showers, especially when factoring in the massive consumption tied to landscaping and outdated plumbing fixtures. Installing aerators on your kitchen and bathroom sinks—a project costing less than twenty dollars—saves thousands of gallons a year. The EPA WaterSense program notes that fixing a single running toilet saves a family up to eight hundred dollars annually in water and sewer costs. Renters should aggressively report leaks to landlords, as the compounding cost of dripping faucets directly impacts monthly utility obligations.

3. Grocery and Household Consumables

Feeding a household routinely stands out as the most volatile line item in any budget, but it also offers the highest degree of flexibility. Relying on the USDA monthly food plans to benchmark your spending helps identify whether you are paying a massive premium for convenience foods and disjointed shopping habits. Implementing a strict inventory system—checking your pantry before ever setting foot in a store—prevents the classic scenario of buying duplicate spices and perishable produce. Purchasing staple goods in bulk and adhering to a rigid grocery list routinely shaves twenty percent off the average family food budget.

4. Broadband Internet

Internet service providers rely on customer apathy to gradually increase rates once promotional periods expire. You should call your provider annually to negotiate your rate; politely inform their retention department that you are reviewing competitor offers and actively considering a switch to a local fiber-optic network. Downgrading your speed represents another viable tactic—most homes paying for expensive gigabit internet speeds only require a fraction of that bandwidth for standard streaming, online gaming, and remote work. You can also eliminate arbitrary equipment rental fees by purchasing your own reliable modem and router, a straightforward technological move that typically pays for itself within six short months.

5. Cellular Phone Plans

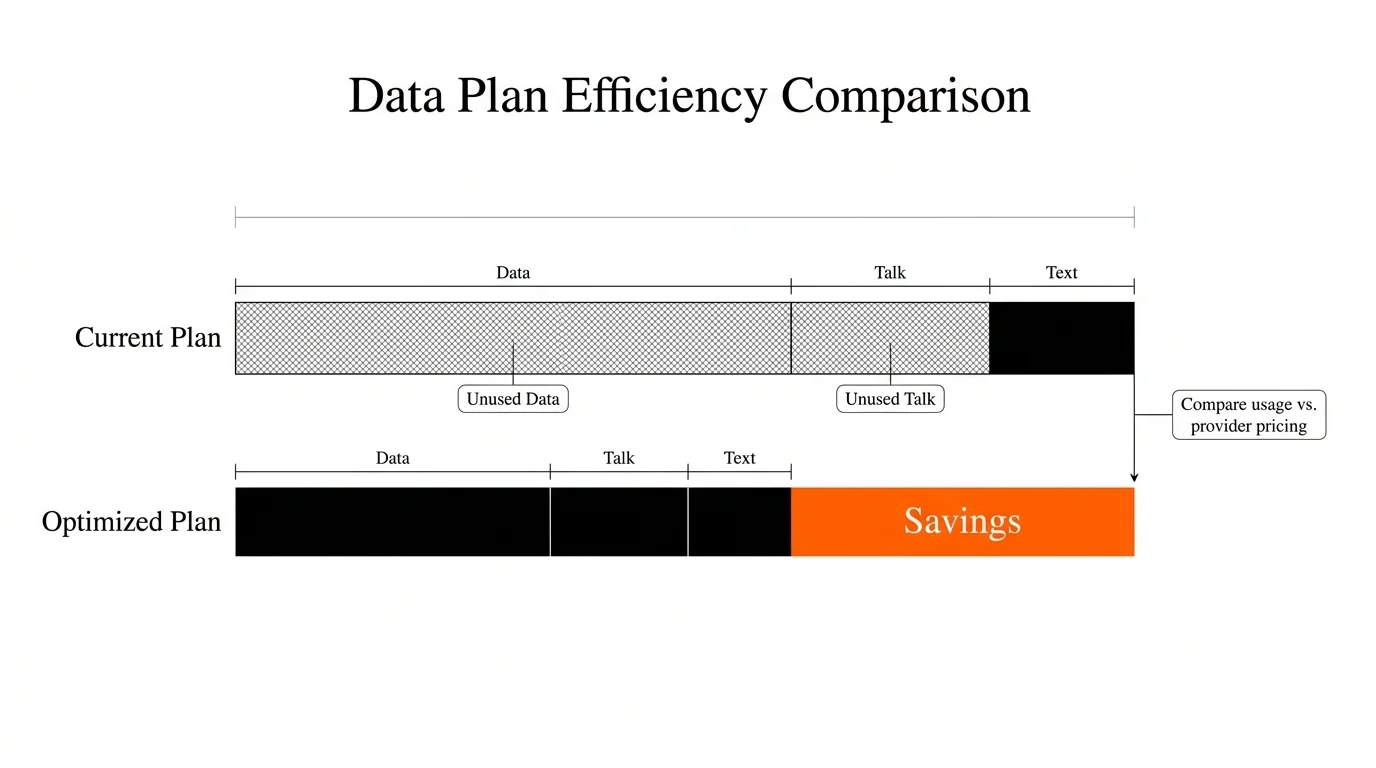

The era of being locked into exorbitant, multi-year contracts with major cellular carriers has thankfully ended, paving the way for affordable mobile virtual network operators. These budget-friendly carriers lease tower space directly from the primary networks, offering identical geographical coverage and call quality at a mere fraction of the traditional cost. A family currently paying two hundred dollars a month can often seamlessly switch to a prepaid family plan offering unlimited data for under eighty dollars. Review your actual monthly data consumption; if you constantly connect to Wi-Fi at home, at the local coffee shop, and in the office, you are actively paying for premium unlimited data tiers you simply do not use.

6. Streaming and Digital Subscriptions

Subscription fatigue drains household accounts quietly, often masked by low individual price points that collectively amount to a massive annual expense. Conduct a ruthless purge of your streaming services, keeping only the one or two platforms your family actually watches daily. You can cycle through services rather than maintaining them simultaneously—subscribe to a platform for a month to binge a specific show, then cancel it and rotate to another. Consolidating family plans for music and utilizing digital resources from your local library further eliminates redundant entertainment costs.

7. Homeowners or Renters Insurance

Insurance premiums tend to creep upward every year, yet many homeowners and renters blindly auto-renew their policies without shopping the market. Consulting with an independent insurance broker reveals steep discounts for bundling your home and auto policies, installing security systems, or upgrading your roof. Increasing your deductible from five hundred to one thousand dollars significantly lowers your monthly premium, freeing up cash that you can route directly into a dedicated emergency fund.

8. Lawn Care and Property Maintenance

Outsourcing your landscaping, gutter cleaning, and seasonal pool maintenance buys you precious time, but it exacts a heavy toll on your monthly cash flow. Reclaiming just one of these minor physical tasks—such as mowing your own lawn on Saturday mornings or handling basic seasonal fertilization—keeps hundreds of dollars securely in your pocket each season. If tackling the entire yard proves physically impossible due to your schedule, negotiate with your current provider to strategically reduce the frequency of their visits, shifting from weekly to bi-weekly service during the slower, cooler growing months.

9. Pest Control Services

While severe infestations require professional intervention, routine quarterly preventative sprays are tasks you can easily manage yourself using commercial-grade concentrates. Purchasing a basic pump sprayer and a highly-rated perimeter treatment costs less than fifty dollars, providing enough product to protect your home for over a year. By handling this specific maintenance routine internally, a typical homeowner eliminates a recurring forty-dollar monthly expense while achieving the exact same defensive results.

Establishing Systems and Maintenance Schedules

Lowering your bills requires temporary effort, but keeping them low demands robust household systems and predictable maintenance schedules. When you establish a standardized meal planning cadence—mapping out dinners every Sunday morning and prepping ingredients in bulk—you inherently reduce the friction that leads to expensive takeout orders. This operational mindset applies directly to your physical property. Creating a seasonal maintenance checklist ensures you regularly replace HVAC filters and clean refrigerator coils. A dirty furnace filter forces your system to work harder, accelerating wear and tear while quietly inflating your energy bill. Calendar reminders serve as the ultimate defense against negligence; schedule specific days to check for plumbing leaks and review your telecom bills. Treating your home like a commercial facility with preventative maintenance protocols stabilizes your spending.

Securing Family Buy-In and Cooperation

Financial optimization fails miserably if you are the only person in the household actively participating in the effort. Securing buy-in from your partner and children transforms budgeting from a punitive restriction into a collaborative, goal-oriented challenge. Sit down with your family and explicitly tie the cost-saving measures to a tangible, shared reward. You might explain that by cutting the grocery bill and eliminating three streaming services, the family will fund a summer road trip. Use specific, constructive communication scripts; instead of demanding people turn off the lights, say that managing the electricity usage directly pays for their weekend entertainment. Creating mini-challenges fosters teamwork and makes financial mindfulness engaging rather than oppressive.

Building Your Household Safety Net

Every dollar you successfully trim from your recurring bills should immediately deploy into a dedicated contingency fund, fortifying your household against inevitable financial shocks. A true safety net transforms a catastrophic appliance failure or an unexpected medical bill into a mere administrative inconvenience. Start by automatically routing your newly generated savings into a high-yield savings account. If you negotiate your internet bill down by forty dollars, set up an automatic transfer for that exact amount on the first of every month. The Consumer Financial Protection Bureau emphasizes that building even a modest emergency fund dramatically reduces the likelihood of relying on high-interest credit cards. Over time, this operational surplus compounds, granting you total peace of mind.

Frequently Asked Questions

How do rent versus own decisions impact my ability to lower monthly expenses?

Renters typically have fewer structural expenses to worry about—landlords cover property taxes, major repairs, and often utilities like water or trash. However, renters remain subject to annual lease increases and have limited ability to make major energy-efficient upgrades. Homeowners bear the absolute burden of all maintenance and volatile property taxes, but they can aggressively lower costs by upgrading insulation, installing solar panels, or refinancing their mortgage. Both demographics must focus heavily on the behavioral consumption of utilities and food to maintain low bills.

What immediate steps should I take when inflation spikes my household expenses?

When inflation drives up the cost of living, you must immediately halt all discretionary spending and audit your consumable goods. Switch from name-brand groceries to store brands, strictly enforce a zero-food-waste policy, and temporarily pause any subscription services. You should also call your insurance and telecom providers to ask for hardship reductions or loyalty discounts, as companies often grant temporary rate relief to retain customers during economic downturns.

Are home warranty plans worth the monthly premium for cost-conscious families?

Home warranties frequently function as a double-edged sword for tight budgets. While they promise to cover system failures, they require a monthly premium alongside mandatory service call fees. For highly disciplined savers, it often proves more economical to cancel the warranty, route that premium directly into a personal home repair fund, and hire trusted local professionals when items break.

How can a renter successfully negotiate utility or maintenance costs with a landlord?

Renters hold more leverage than they realize, particularly if they are reliable and keep the property in excellent condition. You can approach your landlord and offer to take over basic property maintenance—such as mowing the lawn or handling minor interior repairs—in exchange for a reduction in monthly rent. Additionally, if the property features ancient, energy-draining appliances, you can present data showing how a minor landlord investment in efficient replacements lowers your utility burden.

Transforming Your Household Cash Flow

Achieving financial stability within your home does not require winning the lottery or securing a massive promotion at work; it requires a systematic, deliberate approach to the money already flowing through your bank account. Small operational tweaks—like calling your internet provider, insulating your windows, and rethinking your grocery strategy—compound massively over time. By aggressively managing these nine monthly bills, you transition from a passive consumer to an empowered household manager. Take action on just one or two of these categories this week, and watch as those minor adjustments secure lasting financial breathing room for your family.