You review your credit card statement and spot the usual suspects: a legacy cell phone plan, a sprawling streaming bundle, and a hefty auto insurance premium. Look closer, and you realize you are still footing the bill for your 26-year-old’s daily conveniences. Financial independence rarely happens overnight; it resembles a slow transition rather than a sudden leap. While you want to help your adult children navigate rising living costs, endless support often compromises your own retirement timeline. If you feel secretly burdened by these lingering expenses, you are not the only one funding a stealth family payroll. We unpack the most common expenses parents cover today and provide actionable strategies for achieving true financial independence.

State of the Wallet: The Cost of the Extended Nest

The economic landscape for young professionals is harsh, characterized by steep housing costs, persistent inflation, and heavy student loan burdens. Consequently, the bank of mom and dad remains open long past graduation. According to a Bankrate survey on parental financial sacrifices, over sixty percent of parents with adult children sacrifice their own financial security to provide assistance, often draining emergency funds to keep their kids afloat.

Parents currently provide a significant average monthly financial support for adult children that routinely exceeds a thousand dollars per month. A recent Pew Research Center study on young adult financial independence revealed that a majority of parents with children ages 18 to 34 provided them with financial assistance in the past year. While helping your kids get established is honorable, funding their lifestyle indefinitely creates dependency. Identifying where your money leaks is the first crucial step toward reclaiming your future.

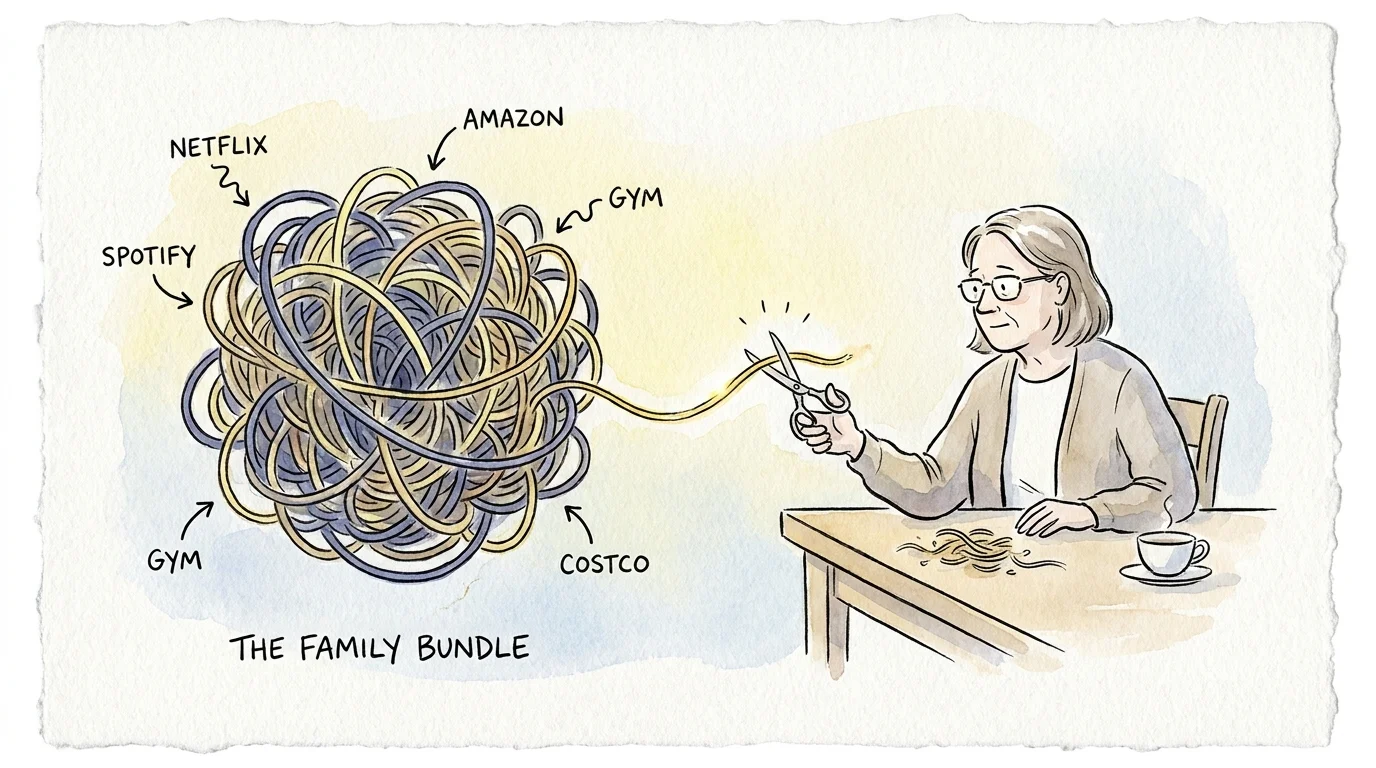

Strategy Pillar 1: Unbundling the Everyday Subscriptions

Small, recurring charges often hide in plain sight. Because these expenses hit your credit card on auto-pay, you rarely notice them adding up. Unbundling these subscriptions begins the financial offboarding process.

* 1. Fingers 2. point 3. to 4. device 5. payment 6. and 7. insurance 8. charges 9. on 10. a 11.

1. Cell Phone Plans

Family phone plans offer undeniable discounts, making it highly tempting to keep your working adult child on your account. However, that extra line costs money, frequently including equipment installment plans for their smartphone upgrade. Calculate their exact portion of the bill—including taxes and device fees—and set up an automatic monthly transfer from their bank account to yours. Once they realize the true cost of connectivity, they might opt for a cheaper prepaid carrier entirely.

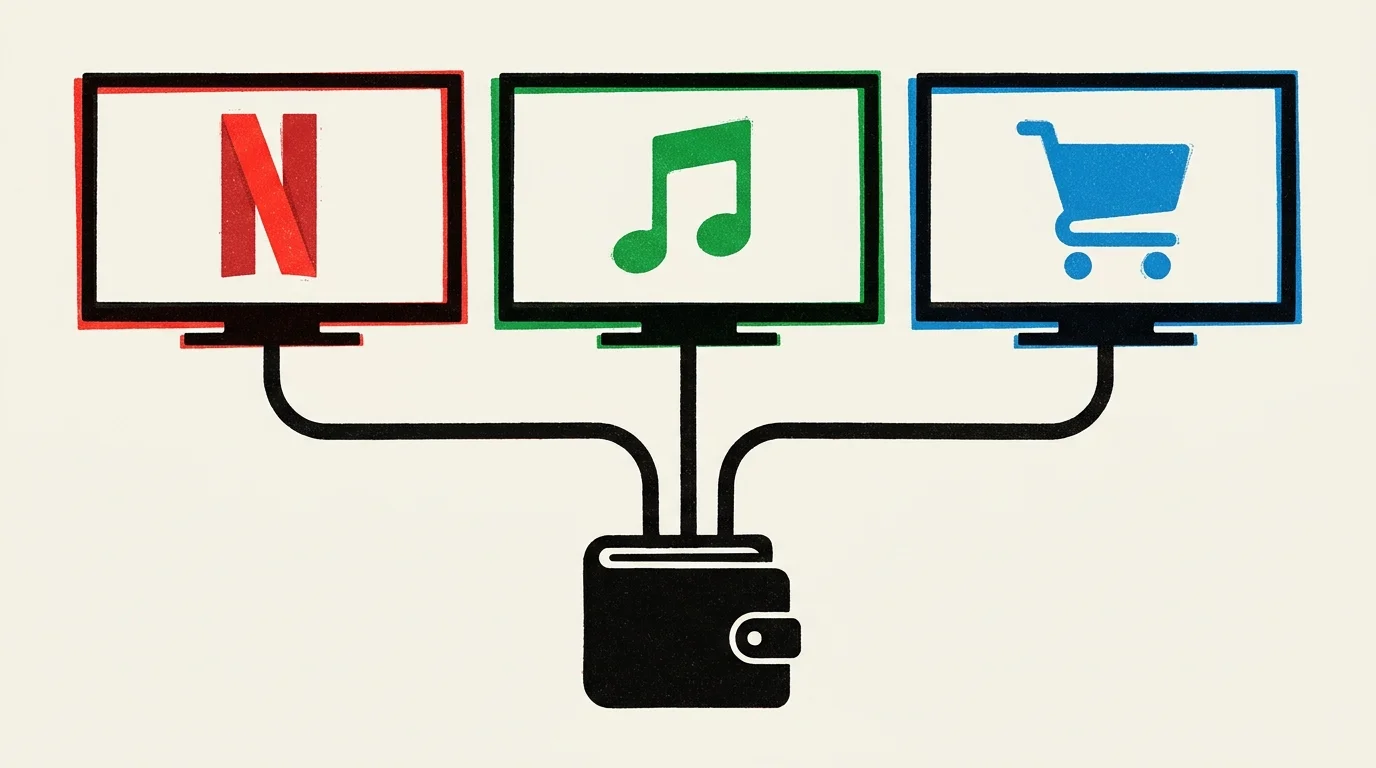

2. Streaming Services and Digital Subscriptions

You likely share passwords for Netflix, Spotify, and Amazon Prime. While platforms are cracking down on household sharing, parents routinely maintain primary accounts while adult kids consume content for free. These micro-transactions silently drain hundreds of dollars from your budget without you noticing. Address this by assigning specific services to your child. If they want premium channels or ad-free music, they can easily take over the billing for that platform.

3. Gym Memberships and Club Dues

Parents often sign teenagers up for local gym memberships, only to completely forget the recurring charge when the child moves away. It is shockingly common for parents to pay fitness dues for a facility their child has not visited in years. Audit your bank statements specifically for wellness charges. Cancel any memberships your child no longer uses, and transfer billing details for active memberships directly to their personal credit card.

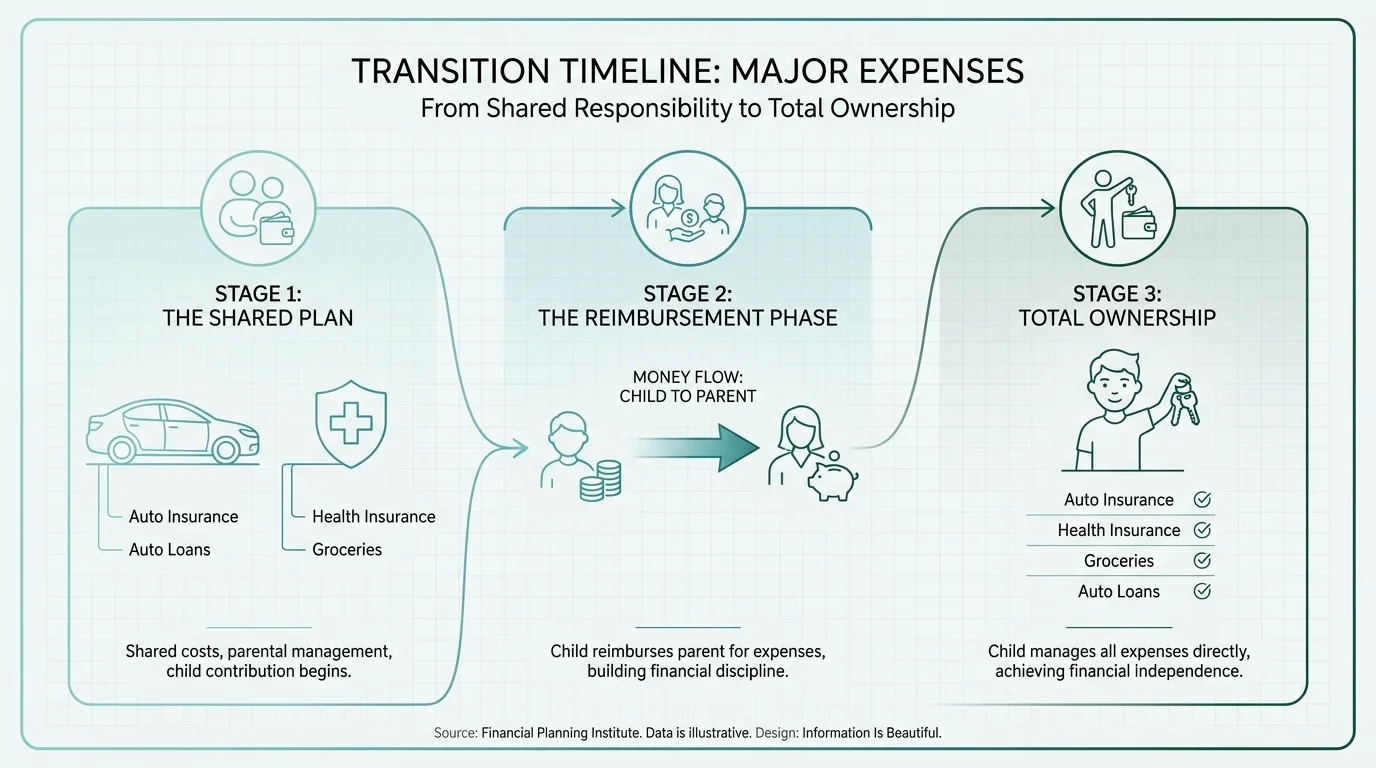

Strategy Pillar 2: Transitioning the Big-Ticket Basics

Once you tackle the digital subscriptions, it is time to address the structural expenses that form the foundation of an adult budget. These categories require delicate conversations, as they directly impact your child’s daily stability.

4. Auto Insurance Premiums

Car insurance is expensive for drivers under twenty-five, prompting parents to keep young adult children on the family policy. While staying on a joint policy secures a better rate, you should not be paying the premium yourself. Request a detailed breakdown from your agent showing exactly how much your child’s vehicle adds to the total cost. Hand this figure to your child and establish a firm due date for reimbursement.

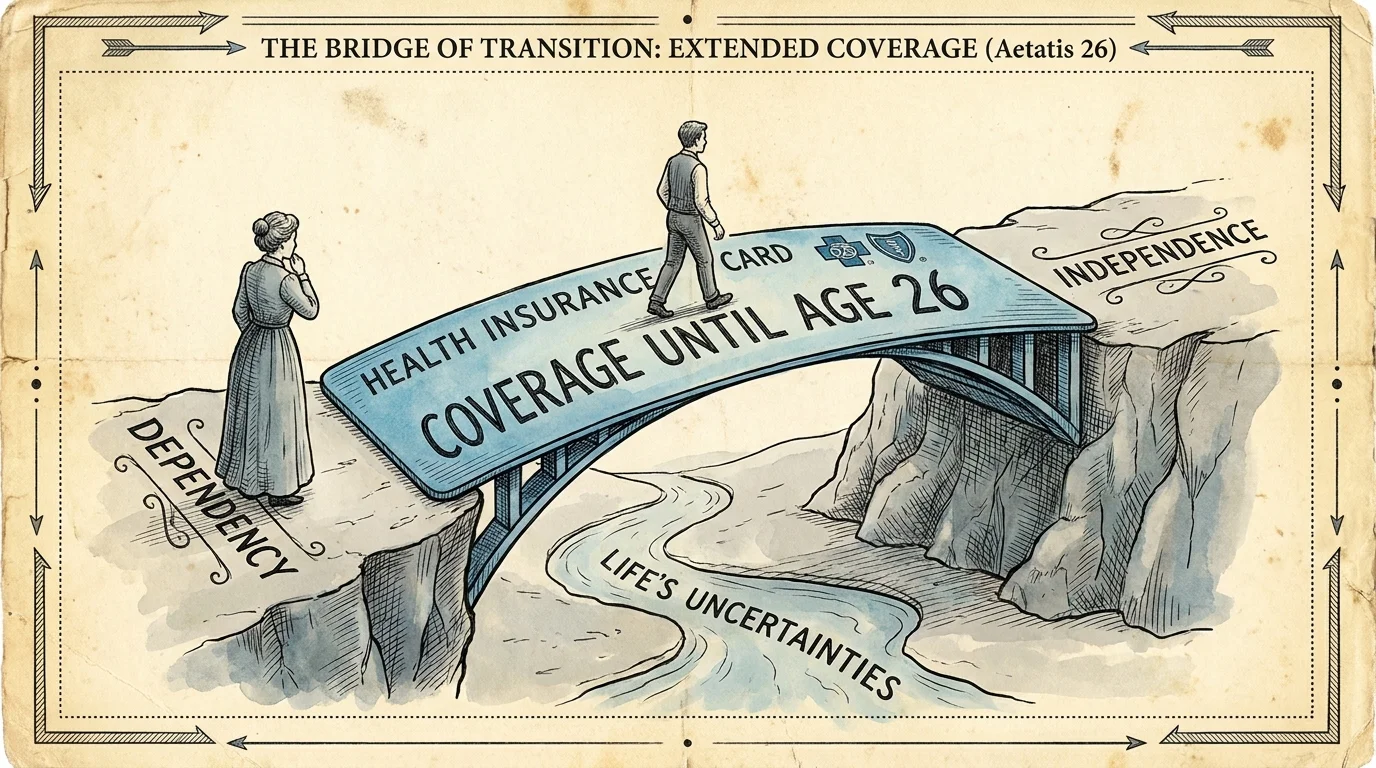

5. Health Insurance Plans

The Affordable Care Act allows young adults to remain on parents’ health insurance until twenty-six, providing an excellent safety net. However, covering their premiums and copays is a separate issue. If your employer charges extra to keep dependents on your plan, ask your working child to subsidize that premium difference. Require them to pay their own medical bills to build healthcare literacy before they age out of your coverage.

6. Groceries and Meal Delivery

It is natural to buy your kids groceries when they visit, but it is entirely different when they routinely use your credit card for weekly grocery runs or meal deliveries. Millions of parents subsidize their grown children’s supermarket bills to combat food inflation. To help them eat well without handing over a blank check, replace open-ended credit card access with a fixed-amount grocery gift card to force budgeting.

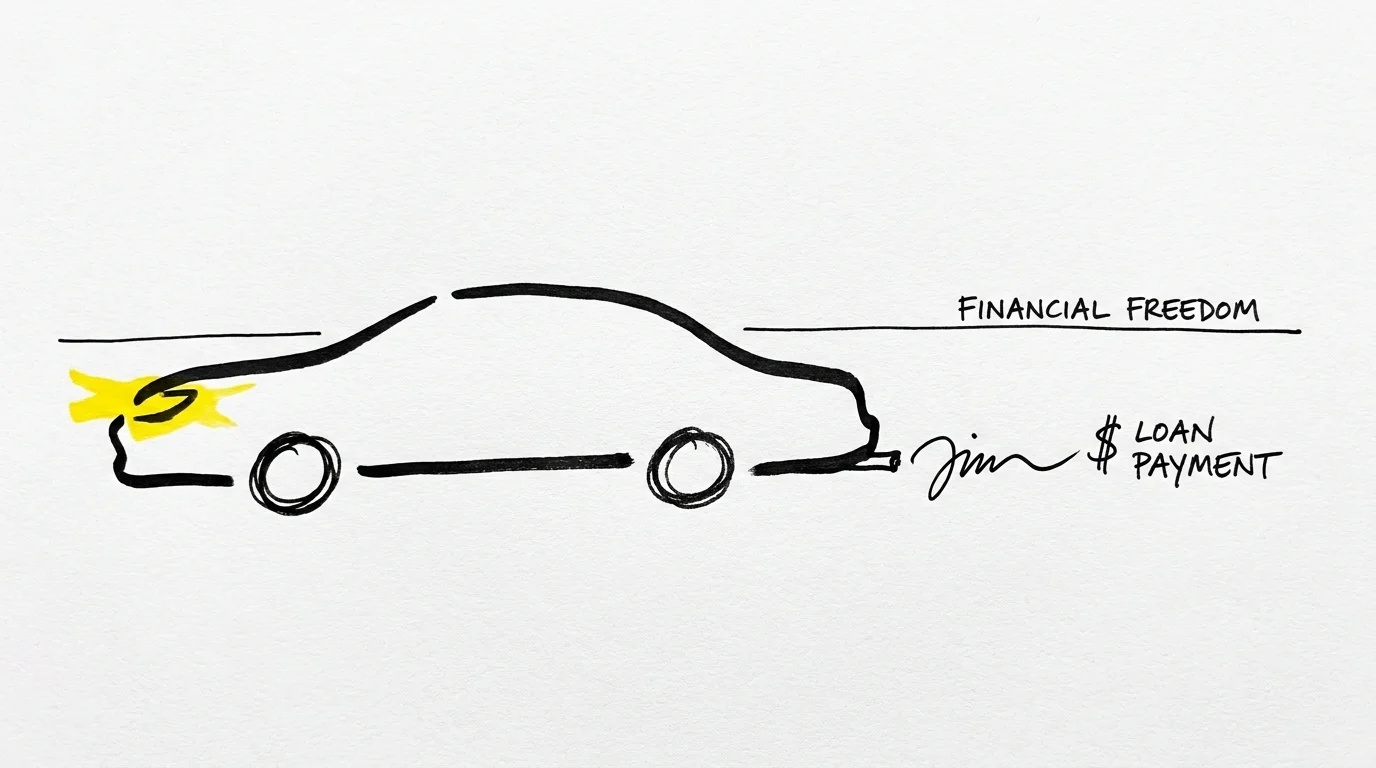

7. Auto Loans and Transportation

Co-signing an auto loan helps your child secure a reliable vehicle, but parents often end up making the monthly payments when the child’s budget gets tight. Covering a car payment severely restricts your personal cash flow. If you currently pay their auto loan, mandate a structured transition period. Inform them that within six months, they will be fully responsible for the note. If the vehicle is too expensive, advise selling it.

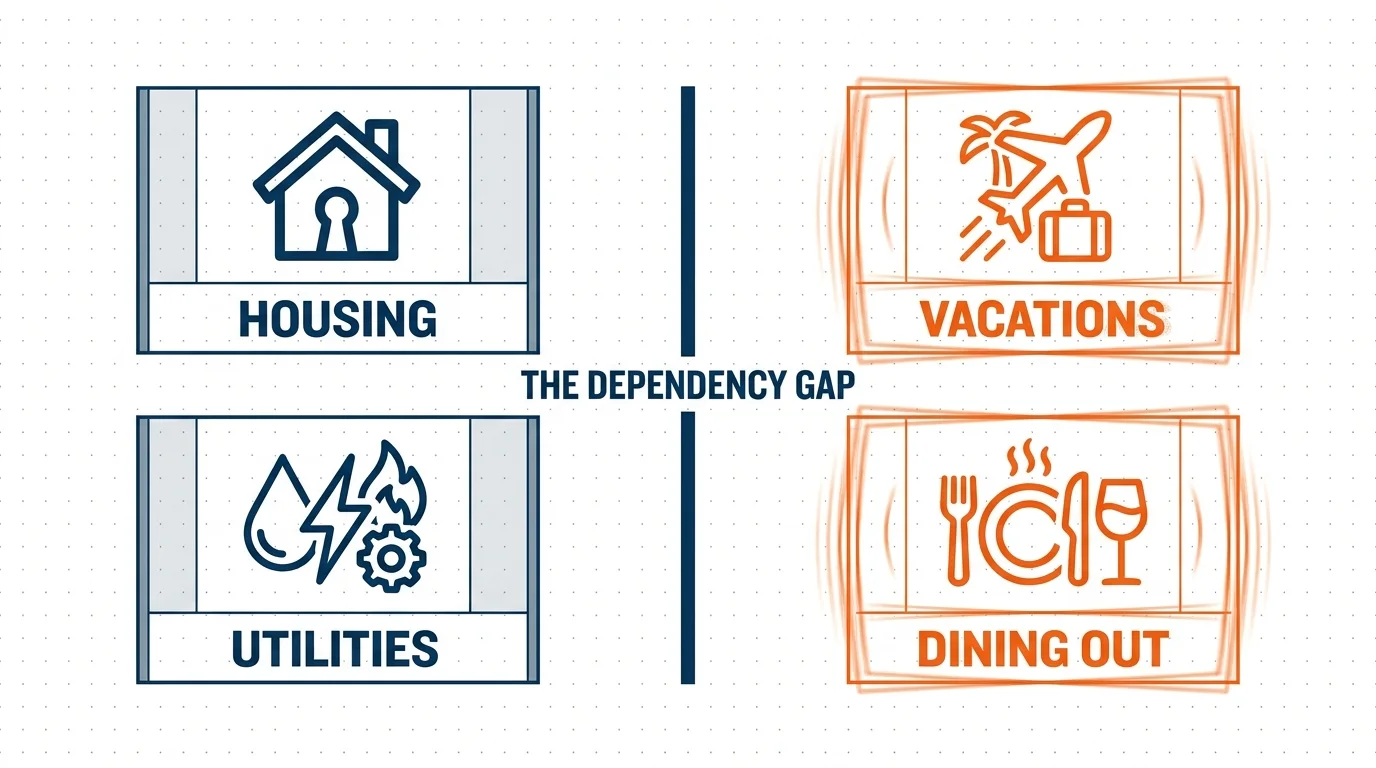

Strategy Pillar 3: Addressing Lifestyle and Living Costs

The final pillar involves the heaviest financial burdens. Funding an adult child’s lifestyle choices or housing needs places the greatest strain on your retirement timeline.

8. Rent and Mortgage Assistance

Housing affordability is a genuine crisis, leading young adults to rely heavily on parents for rent contributions. Bank of America notes ongoing trends in empty nest financial support, highlighting that a substantial portion of Generation Z does not pay for their own housing. Treat subsidized rent as a temporary launchpad. Draft a clear written agreement detailing when your financial contribution will decrease. If they live at home rent-free, implement a modest monthly housing fee.

9. Vacations and Travel

Family vacations are wonderful bonding experiences, but paying for your adult child’s flights, hotels, and dining is a luxury you must carefully evaluate. Funding independent trips with friends crosses the line into pure indulgence. Never finance an adult child’s leisure travel while neglecting your retirement savings. Communicate your boundaries clearly before planning the next family trip. Tell them they will need to cover their own airfare and daily spending money.

10. Student Loan Payments and Tuition

Watching your child struggle with student debt is painful, prompting many parents to make monthly payments on their behalf. While minimizing interest accrual is a noble goal, you cannot prioritize their educational debt over your wealth accumulation. If you currently pay their student loans, ask them to apply for an income-driven repayment plan. These federal programs cap monthly payments based on discretionary income, making the debt highly manageable without continuous intervention.

Real-World Voices: Insights From Financial Experts

Financial planners consistently warn against the dangers of over-supporting adult children. The fundamental rule of family wealth management states that you must secure your own oxygen mask before assisting others. Your retirement accounts cannot borrow money to fund your later years, whereas your child has decades of earning potential ahead to finance their lifestyle and pay down their debts.

Behavioral economists point out that shielding young adults from financial friction stunts their developmental growth. When parents automatically cover shortfalls, young professionals never learn lifestyle sizing—the ability to align their spending with their actual income. Setting clear boundaries is an act of long-term care. Consulting the Consumer Financial Protection Bureau provides excellent guidelines on managing family debt and obligations that can help structure these difficult conversations.

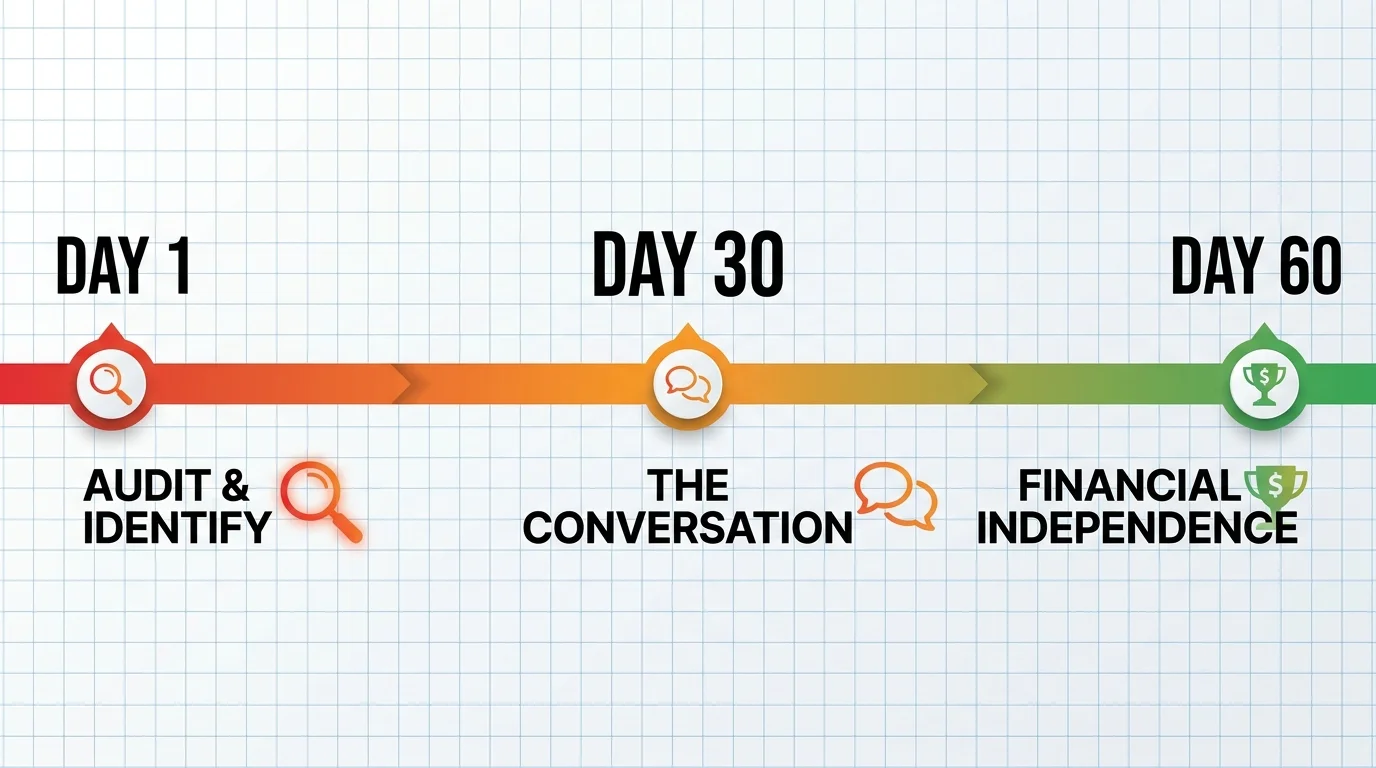

Action Lab: Your 60-Day Financial Offboarding Plan

Moving your adult child off your payroll requires a structured, predictable approach rather than an abrupt cutoff. You can implement a gentle but firm sixty-day offboarding plan. Start your first phase by auditing your expenses. Print out your last three months of bank and credit card statements. Highlight every transaction that benefits your adult child, from auto insurance premiums down to minor streaming services. Add these up to discover your true monthly outlay; the final number will likely surprise you.

Move into the second phase by scheduling a formal financial meeting with your child. Approach the conversation as a partnership rather than a punishment. Show them the numbers and explain that you need to redirect these funds toward your retirement. In the final phase, execute a staggered handover. For example, if you currently pay their two-hundred-dollar car insurance bill, have them pay fifty dollars next month, one hundred dollars the following month, and the full balance by the third month.

Guardrails & Pitfalls: Avoiding the Guilt Trap

As you implement these changes, you will inevitably face emotional resistance. The most common pitfall parents encounter is succumbing to guilt. Your child might complain that they cannot afford to go out with friends or that their budget is too tight. You must resist the urge to step back in and rescue them from minor inconveniences. Experiencing a tight budget is a normal, healthy part of being a young adult.

Another frequent mistake is maintaining vague agreements. Telling your child they need to start paying for their own things soon rarely yields results. You must attach concrete dates and specific dollar amounts to your expectations. Do not let emotional blackmail deter you from your goal. If your child argues that your refusal to pay for their vacation means you do not care, gently remind them that your love is not tied to your wallet.

Frequently Asked Questions

How do I stop paying my adult child’s bills without causing a family rift?

Transparency and ample notice are your best tools. Do not cut off their phone unannounced out of frustration. Schedule a dedicated conversation and outline a realistic timeline for them to assume their expenses. Explain your own financial goals, such as preparing for retirement. When you position the change as a necessary step for your financial health rather than a penalty for their behavior, they are much more likely to cooperate.

Should I charge my adult child rent if they move back home?

Yes, charging rent is generally a wise strategy. The amount does not need to reflect market rates; even a few hundred dollars a month establishes a sense of responsibility and prevents them from growing too comfortable. It forces them to budget their income just as they would if they lived independently. If you do not actually need their rent money, secretly save their payments and gift it back to them later.

Can I legally kick my adult child off my health insurance before they turn 26?

You are under no legal obligation to keep your adult child on your employer-sponsored health insurance plan until they turn twenty-six. The law simply requires insurers to allow you to keep them on the policy if you choose. You can remove them during your company’s annual open enrollment period or a qualifying life event. Always communicate this plan well in advance so they have adequate time to secure alternative coverage.

How do I calculate if I can actually afford to help my adult kids?

You can only afford to help your children financially if you actively meet your own financial targets. This means you have zero high-interest debt, a fully funded emergency savings account, and consistently max out your retirement contributions. If you fall short in any of these areas, you cannot afford to subsidize your adult child. Every dollar you divert to them is a dollar stolen from your future security.

The Path Forward: Securing Your Future and Theirs

Untangling your finances from your adult child’s daily life takes courage, patience, and a willingness to endure uncomfortable conversations. True financial parenting means teaching them how to fish, not delivering a catered dinner to their apartment every night. By methodically handing over the responsibility for cell phones, insurance policies, and streaming services, you give them the gift of competence. Reclaim your budget this week. Start with one subscription, set a firm date for the transition, and watch your young adult take their rightful step toward genuine independence.