You can recover hundreds of dollars this month by identifying the hidden duplicate charges quietly draining your bank account. Middle-income households often lose significant portions of their paychecks to redundant subscriptions, overlapping insurance policies, and forgotten recurring fees that offer zero added value. When you audit your monthly statements, you reclaim control over your hard-earned cash and redirect those funds toward meaningful financial goals. Finding these accidental double payments requires nothing more than a focused afternoon and a clear understanding of where modern billing systems overlap. Stop letting administrative oversights dictate your financial health, and start keeping the money that rightfully belongs in your pocket.

The State of the Wallet: Why Redundancy Happens

Americans face an unprecedented level of subscription fatigue. The shift toward recurring revenue models means you now rent everything from your productivity software to your evening entertainment. This business model thrives on friction; companies make signing up seamless while designing cancellation processes that require multiple clicks, phone calls, and navigation through deliberately confusing menus. Over time, these small monthly charges blend into the background noise of your credit card statement. When you combine dual-income households merging their finances, the rapid adoption of digital services, and the sheer volume of automatic payments, duplication becomes inevitable.

Recent regulatory actions emphasize the severity of this issue. The Consumer Financial Protection Bureau has actively scrutinized subscription traps and junk fees, noting that confusing billing practices cost consumers billions annually. You are not failing at budgeting if you have a few overlapping charges hidden in your monthly ledger. You are simply navigating a financial landscape engineered to make you forget what you are paying for.

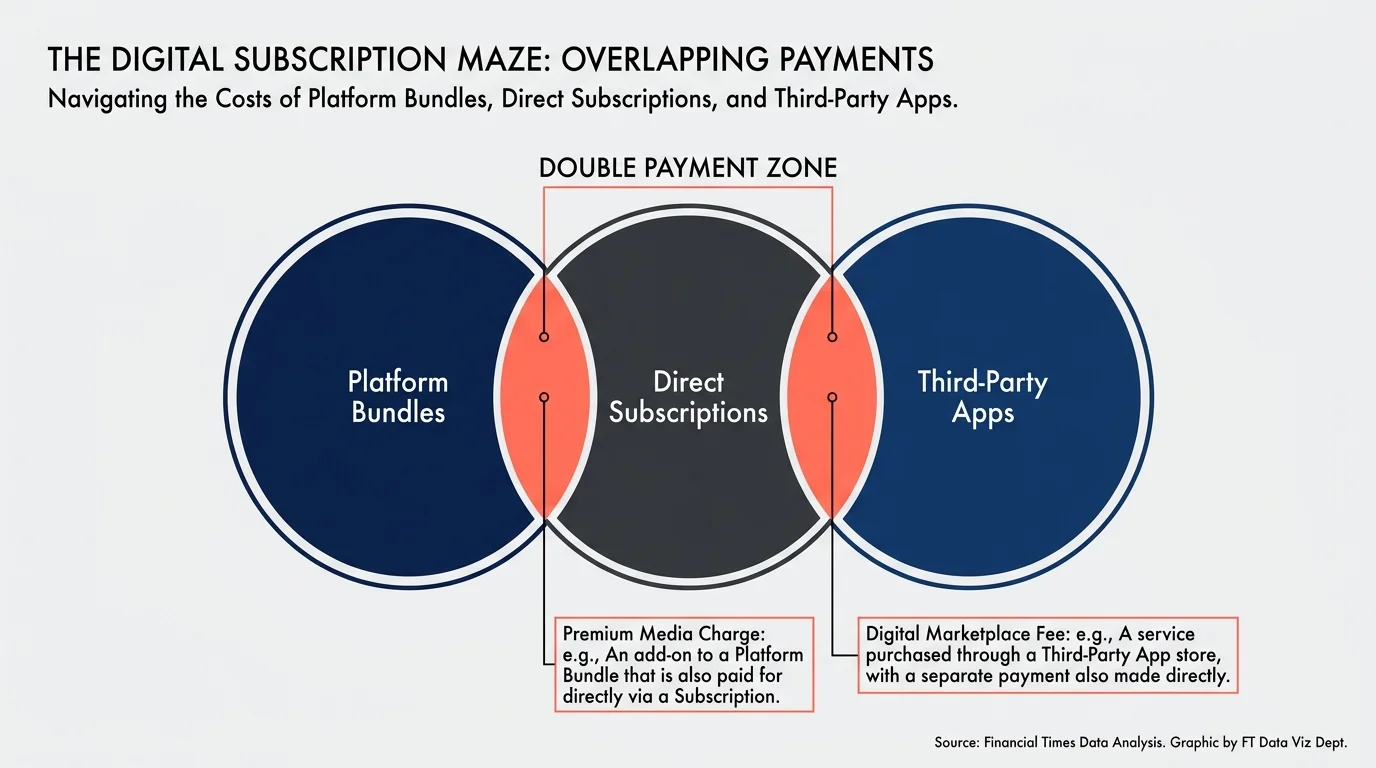

If “third-party” is two:

1. A

2. Venn

3. diagram

4. illustrates

5. how

6. overlapping

7. digital

8. subscriptions,

9. platform

10. bundles,

Strategy Pillar One: Eliminating Entertainment and Digital Overlaps

Your digital life offers the most fertile ground for double payments. The fragmentation of media, app ecosystems, and data storage means you likely subscribe to multiple services that perform the exact same function without realizing it.

1. The Streaming Channel Trap

You often pay for a standalone streaming service while simultaneously paying for that exact same channel as an add-on through another provider. For example, you might subscribe to a premium network directly through their respective website, but later sign up for a free trial through your Amazon Prime Video or Apple TV interface and forget to cancel it. Because the billing names appear differently on your credit card statement—one reading as a direct media charge and the other bundled into a broader digital marketplace fee—the redundancy easily escapes your notice. You must thoroughly review your third-party billing platforms to ensure you are not double-paying for the identical premium content.

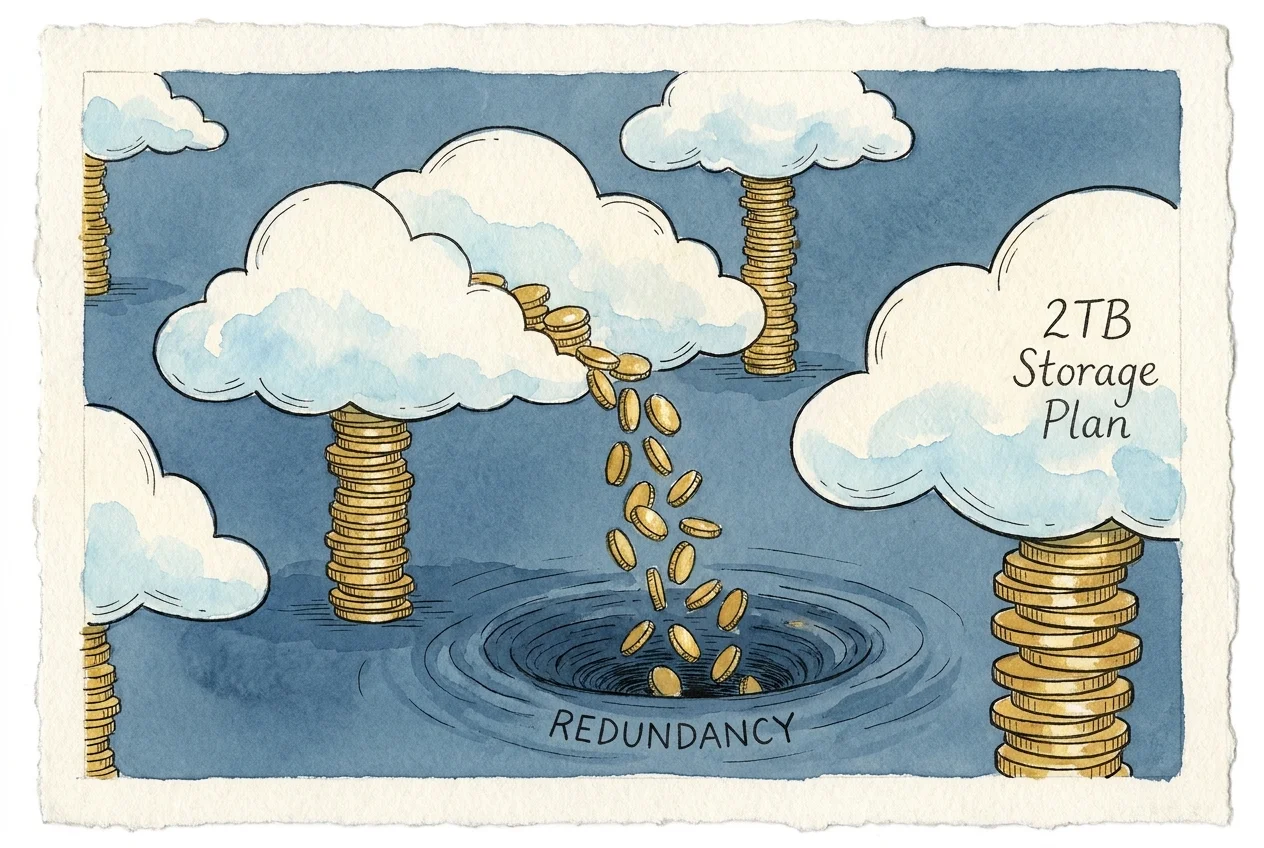

2. Cloud Storage Duplication

Digital hoarding leads directly to financial waste. You probably pay Apple for iCloud storage to back up your smartphone, Google for Drive space to manage your massive email archives, and perhaps Dropbox for document management. These services overlap completely in their core utility. By consolidating your digital files into a single ecosystem, you eliminate the need for multiple premium tiers. Choose the platform that best integrates with your daily workflow and migrate your files accordingly. Canceling the redundant two-terabyte storage plans saves you significant money over the course of a year without sacrificing file security.

3. Premium Delivery Redundancy

The convenience economy tricks you into paying for free delivery multiple times over. You might pay for a standalone restaurant delivery subscription while holding a premium travel or dining credit card that offers those exact memberships as a complimentary, built-in perk. Furthermore, your standard retail memberships often include overlapping grocery and restaurant delivery benefits. If you pay a monthly fee for food delivery but carry a premium rewards card in your wallet, you are throwing money away. Audit your wallet benefits to unlock the overlapping perks you already possess and cancel the standalone subscriptions immediately.

Strategy Pillar Two: Pruning Protection and Financial Services

Fear drives many redundant purchases. Companies upsell protection plans and monitoring services by playing on your anxieties, causing you to buy expensive coverage you already own through existing policies.

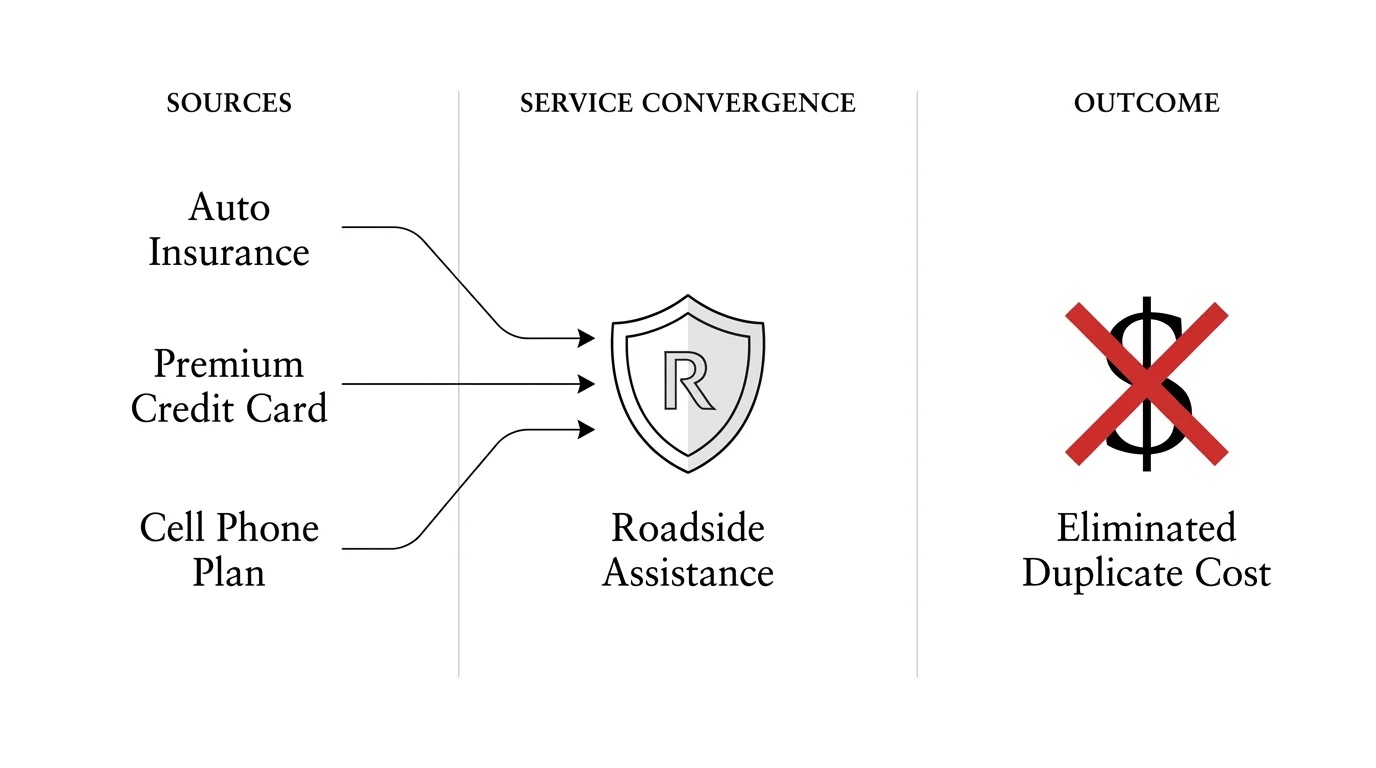

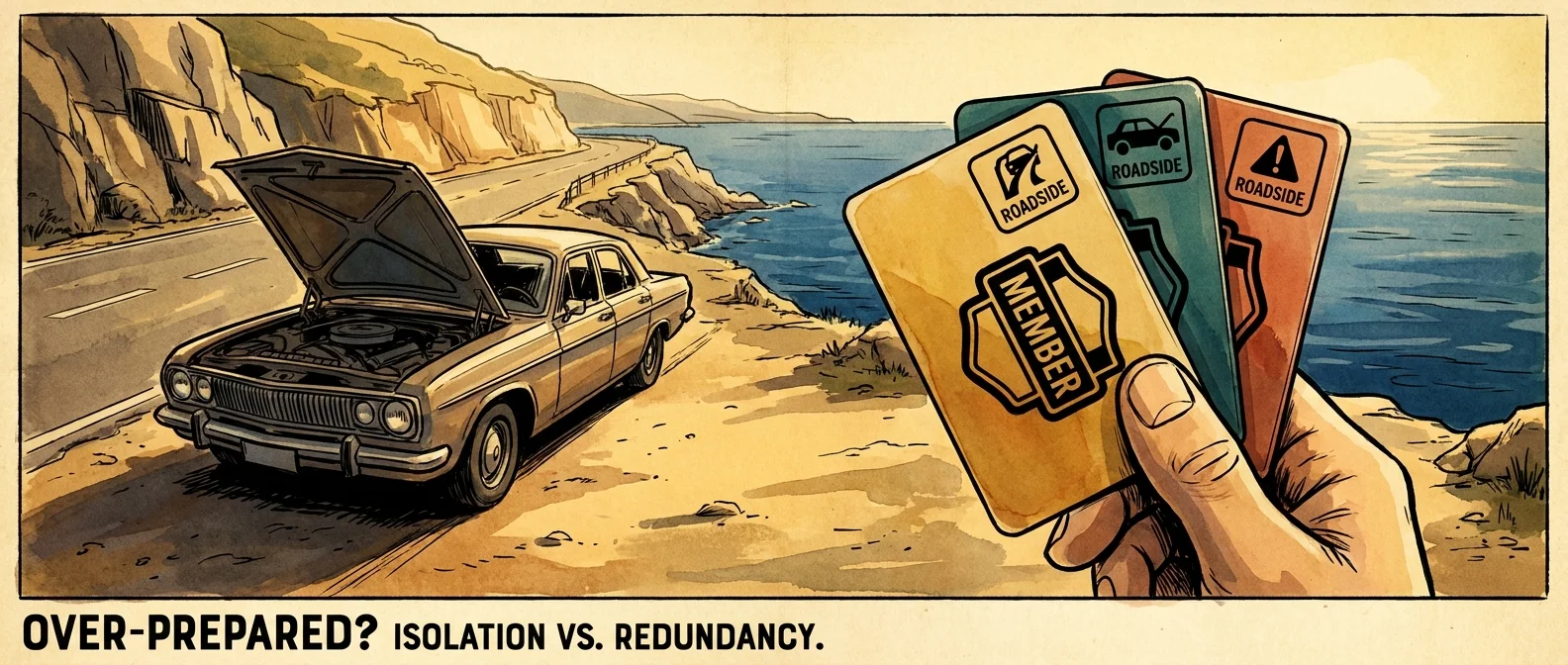

4. Roadside Assistance Triangulation

You likely pay for towing and tire-change services three times over. Many drivers faithfully pay an annual fee to a dedicated motor club out of habit. However, your comprehensive auto insurance policy probably includes roadside assistance for a fraction of that cost. Additionally, many premium credit cards and even new vehicle warranties offer complimentary dispatch services for stranded motorists. Review your auto insurance declarations page and your credit card benefits guide to determine if your standalone motor club membership serves any actual purpose beyond taking up space in your glovebox.

5. Unnecessary Credit Monitoring

Paying a monthly fee for basic credit monitoring represents one of the most common financial redundancies. Third-party companies charge a premium to alert you to changes in your credit file. Yet, almost every major bank and credit card issuer now provides free access to your credit score and sends real-time smartphone alerts for suspicious activity. Furthermore, federal law guarantees your right to review your credit files directly. Following the Federal Trade Commission guidelines on credit reporting allows you to monitor your financial health comprehensively without subscribing to an expensive, redundant third-party service.

6. Overlapping Identity Theft Protection

Similar to credit monitoring, identity theft protection often overlaps with benefits you already receive for free. Many large employers offer comprehensive identity restoration services as part of their standard employee benefits packages. Your homeowners or renters insurance policy might also include a generous rider for identity theft recovery at no additional charge. Before paying a standalone company to monitor the dark web for your email address, consult your human resources department and your property insurance agent to see if you already hold robust, active coverage.

7. Redundant Device Insurance

When you purchase a new smartphone, the retail salesperson heavily pressures you into buying a monthly protection plan. You might politely agree, completely forgetting that you already pay your cellular carrier for a comprehensive family protection plan that covers all devices on the account. More importantly, paying your monthly cell phone bill with a premium credit card often provides complimentary cellular telephone protection against damage and theft. By understanding the built-in benefits of your primary payment methods, you can confidently decline the expensive warranties pushed at the register.

Strategy Pillar Three: Stopping the Convenience and Lifestyle Tax

Lifestyle subscriptions accumulate as your habits change, but the automated billing continues long after you abandon the underlying activity.

8. The Forgotten Digital Fitness App

The booming digital fitness industry frequently double-bills enthusiastic consumers. You might maintain an expensive physical gym membership while also paying for a premium digital workout app or a specialized yoga platform. Often, your physical gym includes a comprehensive digital class library in your base membership, rendering the standalone app completely unnecessary. Evaluate your actual workout habits. If you visit the physical gym three times a week, cancel the digital app. If you prefer working out in your living room, drop the expensive brick-and-mortar membership to stop paying twice for your health routine.

9. Point-of-Sale Travel Insurance

Airlines and online travel agencies aggressively push trip cancellation insurance during the final checkout screen. Panicked travelers often click accept, adding a hefty percentage fee to their total ticket cost. However, if you book that flight using a dedicated travel rewards credit card, you almost certainly already hold robust trip cancellation, delay, and lost luggage insurance. Paying for the airline’s point-of-sale policy creates a complete duplication of benefits. Trust your existing credit card coverages and bypass the point-of-sale fear tactics designed to pad corporate profit margins.

10. Software License Sprawl

Families frequently overpay for essential productivity software by carrying multiple individual licenses. You might pay for a personal word processing subscription while your spouse pays for another, and your college student pays for a third. Upgrading to a family plan dramatically reduces the per-person cost and simplifies your billing. Additionally, many employers and universities provide complimentary home-use licenses for enterprise software suites. Before renewing your annual subscription, verify whether your institutional affiliations provide the exact same software suite entirely for free.

Voices from the Field: How Experts Handle Cash-Flow Audits

Financial planners and behavioral economists view subscription duplication as a classic behavioral trap. The human brain struggles to aggregate small, recurring expenses. A ten-dollar charge feels insignificant in the moment, but multiple ten-dollar charges spread across different billing cycles create a massive drag on your household cash flow over a calendar year. Certified financial planners often mandate a forensic review of the past ninety days of bank statements for new clients. They find that high-earning, middle-income families are actually the most susceptible to this phenomenon because they have enough buffer in their checking accounts to ignore small monthly leakages.

Behavioral economists point to the status quo bias as the primary culprit. Once you set up an automatic payment, canceling it requires active effort, password recovery, and navigating aggressive retention offers. Your brain prefers the path of least resistance, which usually means leaving the subscription active. By reframing the cancellation process as an hourly wage—realizing that spending twenty minutes on the phone to cancel a hundred-dollar annual charge equates to an effective tax-free rate of three hundred dollars per hour—you can easily overcome the psychological hurdle of administrative maintenance.

Action Lab: Your Step-by-Step Budget Tweak

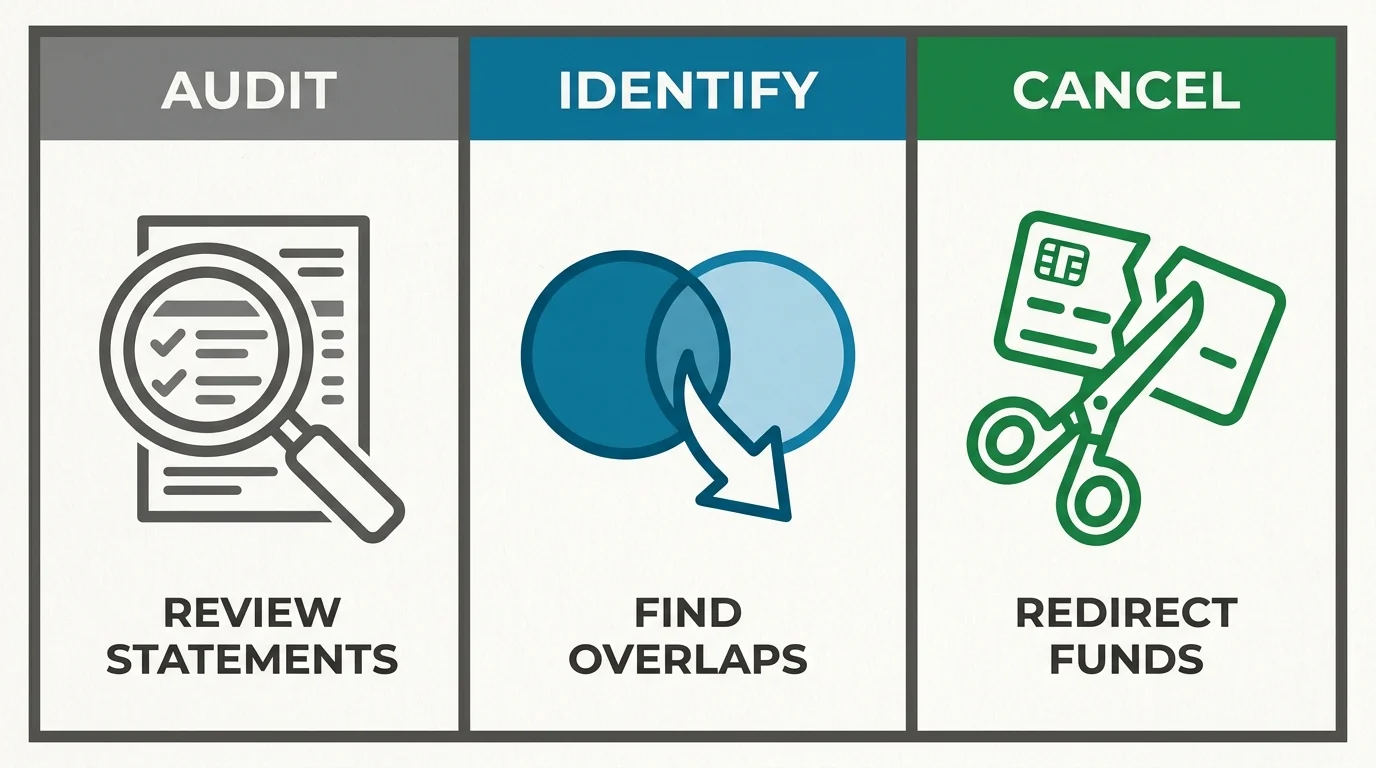

You can eliminate these redundancies this weekend by executing a systematic cash-flow audit. Start by gathering your primary checking account statement and all credit card statements from the previous month. You will need three different colored highlighters or a blank digital spreadsheet. Dedicate the first color to essential utilities and housing. Use the second color for variable necessities like groceries and transportation. Apply the third color strictly to recurring subscriptions, memberships, and automated fees.

Once you successfully isolate the recurring fees, group them by category rather than by date. Place all entertainment subscriptions in one column, all insurance and protection plans in another, and all software or apps in a third. This categorical grouping immediately exposes the hidden overlaps. When you see multiple music and video services stacked together on the same page, the redundancy becomes undeniable.

Next, identify the subscriptions you have not actively utilized in the past thirty days. The Federal Reserve report on the economic well-being of households frequently highlights how optimized cash flow directly impacts financial resilience against unexpected shocks. Take those unutilized or overlapping services and initiate the cancellation process immediately. Do not tell yourself you will do it later. Open a new browser tab, log into the specific service, and terminate the billing agreement. If you calculate the annual cost of the eliminated redundancies, you will likely discover enough recovered capital to fund a minor emergency account or accelerate a lingering debt payoff.

Guardrails and Pitfalls: What to Avoid

While aggressively cutting redundant bills provides a fantastic financial boost, you must proceed with caution to avoid unintended consequences. The most common pitfall involves canceling vital insurance coverage before thoroughly verifying the replacement policy limits. Never cancel your primary auto insurance roadside assistance until you physically verify that your credit card benefit covers the exact mileage and towing requirements for your daily commute. Credit card protections often carry strict limitations and secondary coverage clauses that differ drastically from dedicated insurance policies.

Another frequent mistake involves deleting digital storage without backing up your data. If you decide to cancel your redundant cloud storage provider, you must migrate your photos, documents, and contacts to your primary platform before hitting the cancellation button. Companies routinely purge data immediately upon account termination. Take the necessary time to download your archives locally to a physical hard drive to ensure you do not permanently lose precious family memories in your quest to save a few dollars a month.

Finally, beware of the subscription pause trap. Many digital services offer the option to pause your membership for a few months rather than canceling outright. They rely heavily on the fact that you will forget about the pause, allowing the billing to resume automatically without your direct authorization. Unless you have a concrete, calendar-driven plan to resume using the service, always choose the hard cancellation. You can always sign up again later if you genuinely miss the service.

Frequently Asked Questions

How far back should I review my bank statements to catch annual subscriptions?

You must review a full twelve months of statements to capture every redundant bill. Many software licenses, premium travel credit card fees, and motor club memberships bill on an annual cycle. A ninety-day review will catch your overlapping streaming services and delivery apps, but it will completely miss the large yearly renewals that often represent the most significant duplicate payments draining your resources.

Can I use automated subscription cancellation apps to do this for me?

While third-party financial technology apps offer convenience by scanning your accounts for subscriptions, they often charge a percentage of the money they save you or require a monthly fee themselves. Ironically, paying an app to manage your subscriptions introduces yet another recurring bill to your ledger. You achieve better results and maintain stronger data privacy by conducting a manual review of your own statements.

Will canceling multiple credit cards to avoid overlapping annual fees hurt my credit score?

Closing credit cards can negatively impact your credit score by reducing your total available credit and altering the average age of your accounts. The Federal Deposit Insurance Corporation consumer guidance suggests managing credit carefully to maintain a healthy utilization ratio. Instead of immediately closing a card with an overlapping fee, call the issuer and ask to downgrade the account to a no-annual-fee version. This strategy preserves your credit history while successfully eliminating the redundant yearly charge.

What happens if I accidentally cancel a service I still need?

Canceling a modern digital service is completely reversible and carries almost zero risk. In the rare event you terminate a subscription you actually need, you can simply log back into the platform and resubscribe in minutes. Often, companies will even offer you a highly discounted win-back rate when you return to their platform. Treat cancellation as a stress test for your digital life; if you do not miss the service, you never needed it.

The Path Forward

Mastering your monthly cash flow does not require extreme frugality or endless sacrifice. True financial efficiency comes from aligning your spending with your actual usage and stripping away the administrative bloat that quietly drains your resources. Every duplicate subscription you eliminate functions as an immediate, tax-free raise. Take one hour this weekend to comb through your statements and challenge every automated charge. Reclaiming that lost capital empowers you to build stronger emergency reserves, utilize Securities and Exchange Commission resources on saving and investing more effectively, and finally gain the upper hand over the modern subscription economy.