Securing reliable passive income transforms your retirement years from a period of financial anxiety into an era of genuine financial freedom. You worked decades to build a nest egg; now you need strategies that generate extra money without requiring you to clock into a daily job. Creating streams of retirement income ensures your middle-income household can cover rising healthcare costs, inflation, and everyday living expenses while still affording travel or hobbies. A pragmatic approach to senior finances requires looking beyond traditional pension plans to leverage modern, low-maintenance income vehicles. By taking immediate action to restructure your assets, you will build a resilient financial foundation that pays you consistently, stretching your monthly paycheck and preserving your quality of life.

The State of Your Retirement Wallet

Middle-income households face unprecedented pressure to fund longer lifespans with limited traditional pension options. According to the Federal Reserve Board, many adults approaching retirement feel vastly underprepared for the realities of relying solely on fixed incomes and Social Security benefits. Inflation relentlessly eats away at your purchasing power, making extra money crucial to maintain the lifestyle you enjoyed while working. Generating passive income represents a mandatory layer of defense for senior finances. You must rethink your existing assets and cash reserves to create reliable yields. Financial independence during these golden years requires proactive steps today, allowing your money to work quietly in the background. The days of simply parking cash in a standard savings account have passed; today, prosperity depends on optimizing every single dollar.

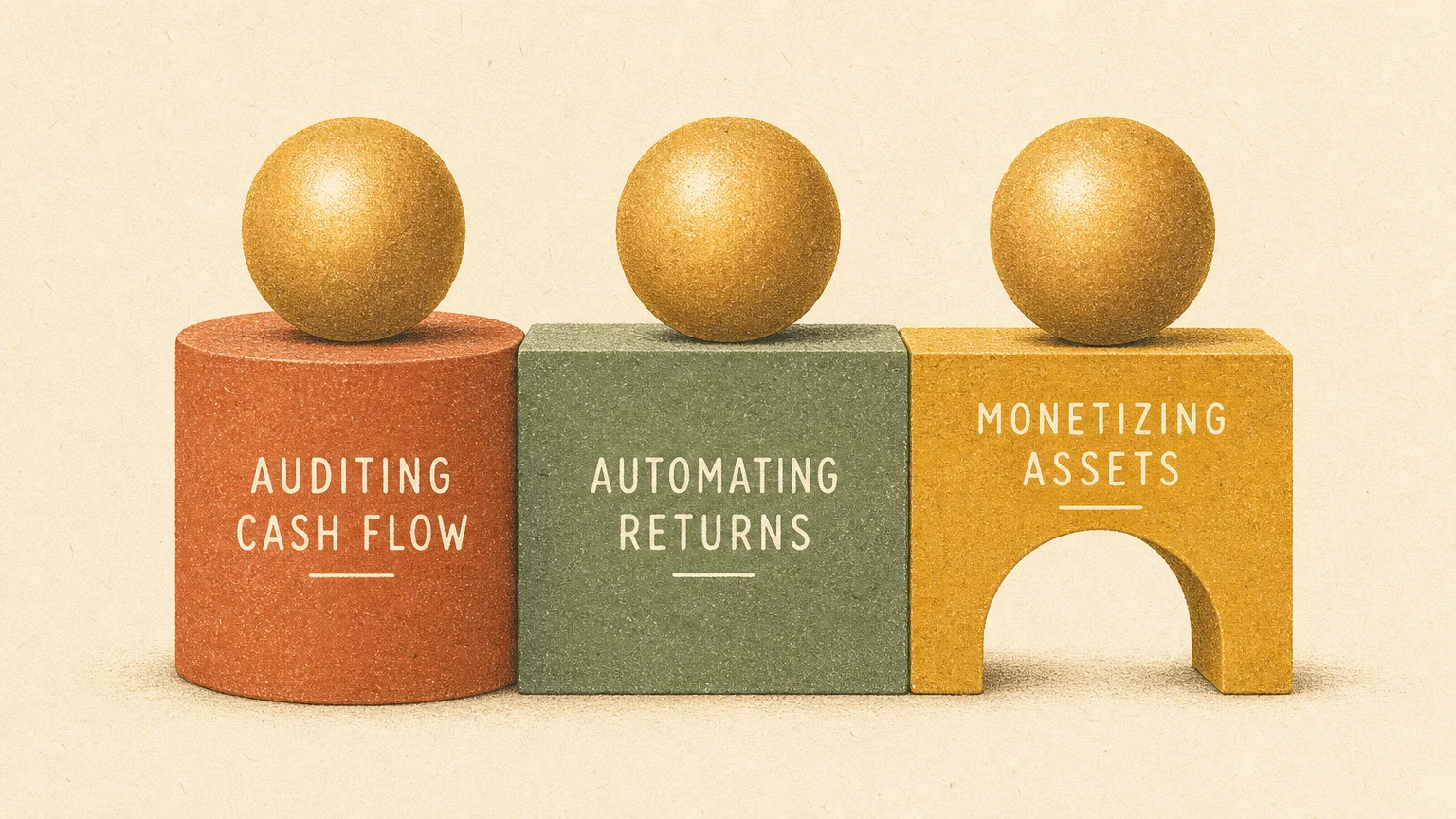

Three Pillars of Financial Freedom in Retirement

Before diving into specific income vehicles, you need a solid framework to govern your choices. Approaching retirement income strategically ensures you do not take unnecessary risks with your principal balances. These foundational pillars will guide you toward sustainable returns.

Pillar One: Auditing Your Cash Flow

You cannot build new income streams if you constantly hemorrhage cash through unnecessary expenses or high-interest debt. Conduct a rigorous audit of your monthly spending habits. Categorize your outbound money into fixed necessities, discretionary lifestyle costs, and debt obligations. Identifying areas where you can trim waste frees up capital to invest in income-producing assets. Think of every dollar saved as a potential employee sent into the market to earn a continuous wage. Lowering your basic overhead automatically decreases the amount of extra money you need to generate.

Pillar Two: Automating Smart Returns

Passive income relies heavily on automation. You want systems that deposit money into your checking account while you sleep, travel, or spend time with family. Set up automatic transfers from your brokerage accounts or high-yield savings directly to your primary spending accounts. This methodology reduces the temptation to touch the principal and protects your long-term financial freedom. The less manual intervention required, the more truly passive your retirement income becomes. Automation strips the emotion out of financial management, ensuring your bills get paid without ongoing stress.

Pillar Three: Monetizing Assets Mindfully

Your home, your savings, and your lifetime of acquired knowledge represent untapped reservoirs of extra money. Middle-income households often overlook the assets they already control. Monetizing these assets requires a shift in perspective; you must view your dormant cash or specialized skills as inventory ready for deployment. Carefully weigh the maintenance costs and effort required for each monetization strategy to ensure the net gain genuinely improves your retirement income without creating a stressful second career.

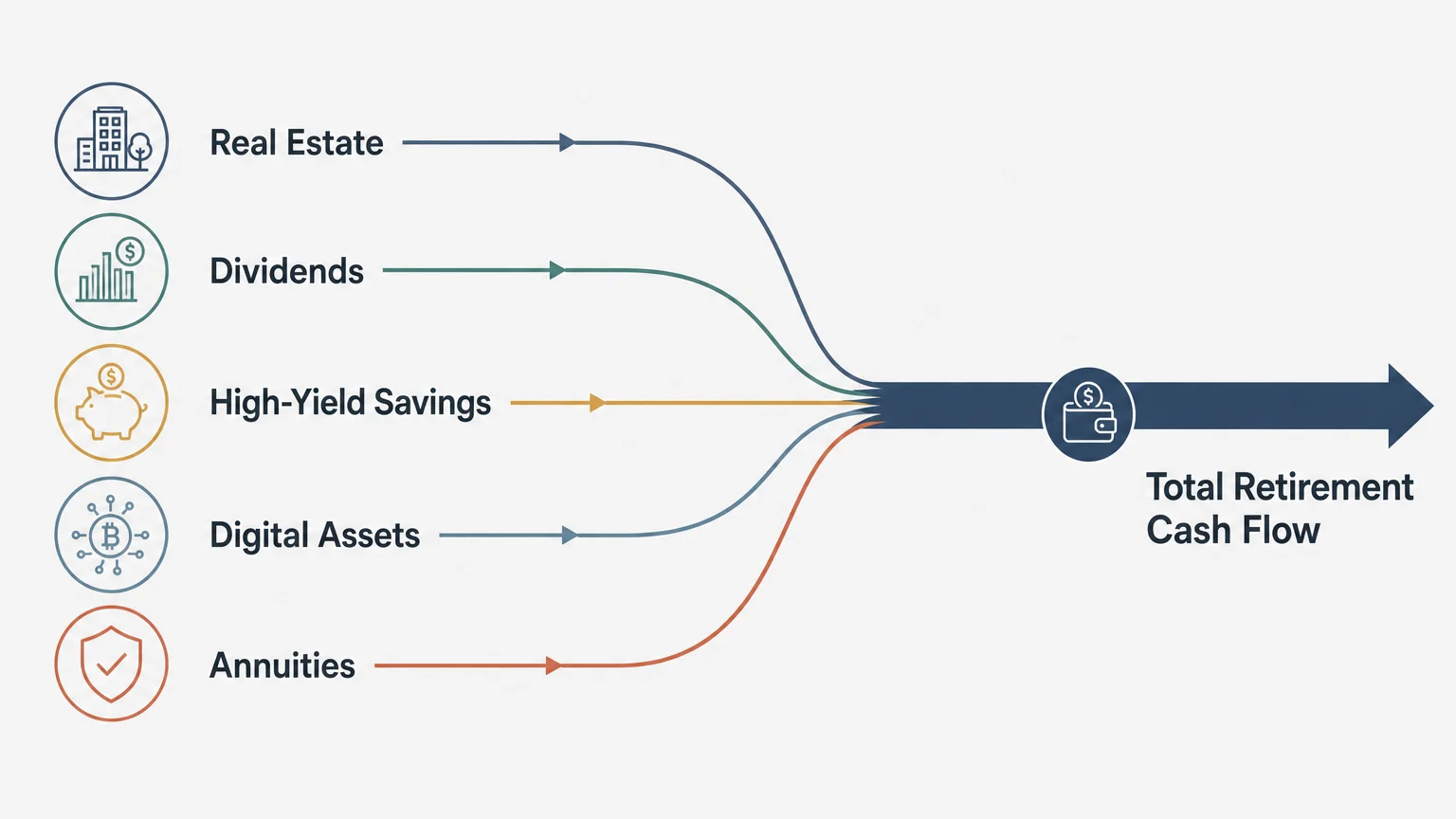

10 Passive Income Ideas for Retirement

Let us explore ten proven avenues to generate passive income. Each option balances risk, effort, and reward differently, allowing you to build a diversified portfolio that robustly supports your senior finances.

Idea One: High-Yield Savings Accounts and Certificates of Deposit

The simplest way to earn extra money begins with moving your idle cash reserves out of traditional bank accounts. High-yield savings accounts and certificates of deposit offer substantially higher interest rates with virtually zero risk. Because these accounts are heavily regulated and typically backed by the Federal Deposit Insurance Corporation, your principal remains secure. By locking a portion of your funds into a CD ladder—buying multiple CDs that mature at staggered intervals—you can access your cash regularly while capturing peak interest rates. This foundational strategy guarantees a predictable stream of retirement income.

Idea Two: Dividend-Paying Stocks

Investing in established corporations that distribute a portion of their quarterly earnings back to shareholders provides a classic route to financial freedom. Dividend-paying stocks, particularly those celebrated for their decades-long history of consistent payouts, offer both immediate cash flow and the potential for long-term capital appreciation. You can choose to reinvest these dividends to accelerate your portfolio growth or have them deposited directly into your bank account. Researching resilient market sectors like utilities or healthcare will help you identify reliable dividend contributors that continue paying out during economic downturns.

Idea Three: Real Estate Investment Trusts

If you desire the steady cash flow of commercial real estate without the crippling headaches of property management, Real Estate Investment Trusts offer an excellent compromise. These specialized companies own and operate income-producing commercial real estate. By federal law, they must distribute at least ninety percent of their taxable income to shareholders as dividends. The Securities and Exchange Commission notes that publicly traded REITs provide robust retirement income and crucial portfolio diversification away from traditional equities.

Idea Four: Renting Out Unused Property Space

Many middle-income retirees find themselves living in homes significantly larger than they currently need. Renting out a spare bedroom, a finished basement, or a highly sought-after parking space can yield significant extra money each month. Modern digital platforms streamline the vetting, booking, and payment processes. While this strategy requires occasional communication and minor ongoing upkeep, the steady influx of substantial cash drastically improves your senior finances. This approach transforms a dormant liability into a performing asset, effectively offsetting the heavy ongoing costs of property ownership.

Idea Five: Fixed Annuities

For those who prioritize absolute certainty in their retirement income, fixed annuities act as a personalized pension plan. You provide a lump sum to a highly rated insurance company, and they contractually guarantee you a set payout for a specific period or for the rest of your life. This vehicle entirely eliminates the anxiety of outliving your money. While annuities often carry internal fees and strict surrender charges for early withdrawal, the sheer peace of mind and predictable monthly checks make them deeply valuable for households seeking sleep-at-night financial freedom.

Idea Six: Creating a Bond Ladder

Bonds represent a loan you make to a major corporation or government entity, which then pays you regular interest until the bond reaches maturity. Constructing a bond ladder involves purchasing multiple bonds with carefully staggered maturity dates. As each bond matures, you receive your principal back to spend on living expenses or reinvest at current market interest rates. This continuous rolling approach delivers highly consistent passive income while protecting you from getting locked into exceptionally low rates during aggressive inflationary periods. It remains a historical cornerstone of conservative senior finances.

Idea Seven: Peer-to-Peer Lending

The digital age allows you to bypass massive traditional banks entirely and lend your capital directly to individuals or small businesses via peer-to-peer lending platforms. By intentionally funding only a tiny fraction of hundreds of different individual loans, you heavily mitigate the catastrophic risk of a single borrower default while earning interest rates that consistently outpace standard savings accounts. This alternative asset class requires careful platform selection and an understanding of consumer credit risks, but it provides an attractive yield for those willing to dedicate a small portion of their portfolio to generate extra money.

Idea Eight: Royalties from Intellectual Property

If you spent your long career creating written content, recording music, drafting designs, or patenting inventions, your past labor can continue to fund your retirement today. Licensing your intellectual property generates reliable royalties every single time someone uses or purchases your original work. Even if you do not consider yourself a traditional artist, self-publishing a specialized how-to guide or creating downloadable digital templates based on your specific professional expertise creates a perpetual stream of passive income. The upfront effort pays off for years, requiring minimal ongoing maintenance.

Idea Nine: Affiliate Marketing on an Existing Digital Platform

If you maintain a popular community blog, a widely read newsletter, or a robust social media presence heavily related to a passionate hobby, you can smoothly monetize that audience through affiliate marketing. By genuinely recommending useful products or services you personally use, you earn a handsome commission on every single sale generated through your unique tracking links. This specific strategy requires a preexisting audience, but once those specialized links go live, they quietly generate extra money around the clock, perfectly aligning with the overarching goals of passive retirement income.

Idea Ten: Silent Partnerships in Small Businesses

Investing essential capital into a thriving local, proven business without taking any active role in the demanding daily operations allows you to securely share in the profits as a silent partner. Many successful small business owners desperately look for private capital to swiftly fund new expansions or purchase heavily needed equipment. Structuring a crystal-clear, legally binding agreement that explicitly outlines your generous profit share and heavily limits your personal liability taps directly into the robust entrepreneurial economy. This advanced strategy requires diligent vetting and sharp legal counsel.

Real-World Voices on Senior Finances

Understanding the mechanics of passive income solves only half the equation; applying them successfully requires a definitive shift in mindset. Financial planners frequently observe that retirees struggle with the psychological transition from saving money to actively spending it. Behavioral economists note that the comfort of earning a regular paycheck makes drawing down principal terrifying for many middle-income households. Generating your own recurring paycheck through diversified streams bridges this psychological gap.

The Consumer Financial Protection Bureau highlights that seniors who proactively maintain multiple streams of income report significantly lower financial stress levels regarding inflation and unexpected healthcare costs. Top advisors strongly advocate for the bucket strategy, where you confidently allocate immediate cash needs to highly liquid savings while keeping long-term funds in diversified market investments. Structuring your assets to pay you directly transforms an unpredictable future into a manageable, well-funded present. Genuine financial freedom comes directly from knowing exactly where your next dollar originates.

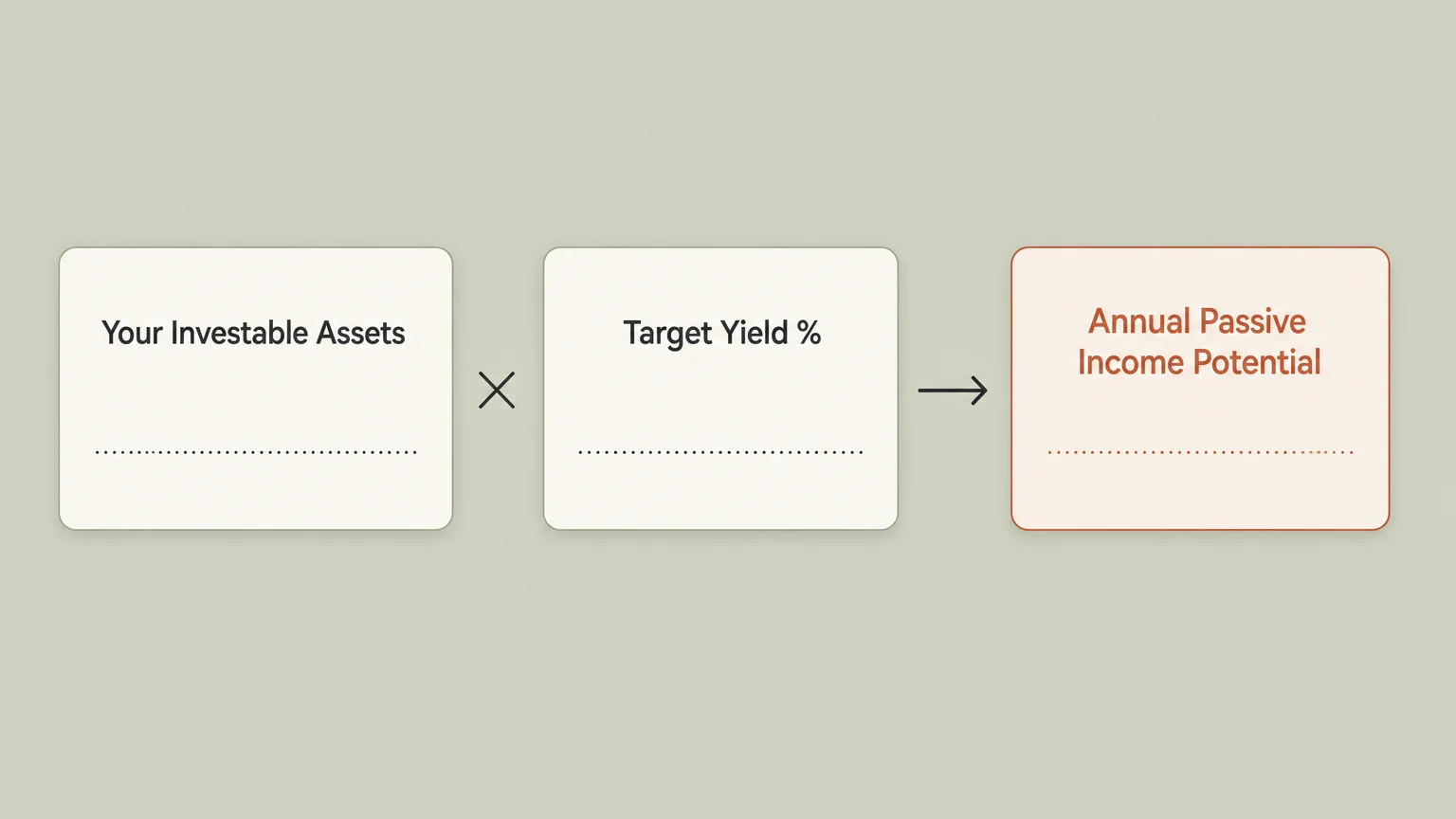

Action Lab: Calculating Your Extra Money Potential

Moving from abstract theory to tangible practice requires running your own concrete numbers. Let us walk through a practical cash-flow exercise you can complete tonight to accurately assess your current retirement income potential.

First, calculate your total annual living expenses. Assume you realistically need sixty thousand dollars a year to live comfortably and travel occasionally. Next, subtract your guaranteed income sources. If Social Security reliably provides thirty-five thousand dollars annually, you currently face a twenty-five-thousand-dollar gap.

Now, closely examine your investable assets. If you hold five hundred thousand dollars in various savings and investment accounts, you need to generate a five percent overall yield to close that specific gap without ever touching your core principal. You might conservatively allocate one hundred thousand dollars to high-yield CDs earning five percent, two hundred thousand dollars to solid dividend-paying stocks yielding four percent, and two hundred thousand dollars to diverse REITs generating six percent. This blended, strategic approach mathematically satisfies your entire twenty-five-thousand-dollar requirement. Run your exact numbers using this straightforward framework to instantly demystify your personal path to financial freedom.

Guardrails and Pitfalls to Avoid

The determined pursuit of passive income contains hidden traps that can swiftly derail your senior finances if you do not proceed with caution. Yield chasing stands out as the single most common and destructive mistake retirees make. When you stretch your portfolio for abnormally high interest rates or massive dividend yields, you almost always take on hidden, disproportionate risk. If an investment suddenly offers double the standard market average, it often signals underlying financial instability within that specific company.

Furthermore, blatantly ignoring the strict tax implications of your extra money can severely impact your actual net returns. Interest generated from savings accounts and peer-to-peer lending is typically taxed as ordinary income by the Internal Revenue Service, whereas qualified corporate dividends might benefit from substantially lower tax rates. Always evaluate an income stream based solely on its after-tax yield. Finally, neglecting the silent threat of inflation will steadily erode your purchasing power. A fixed annuity might sound appealing today, but a flat monthly payment will buy significantly fewer groceries a decade from now. Ensure a core portion of your passive income strategy includes dynamic assets that historically grow alongside climbing inflation.

Frequently Asked Questions

How much money do I need to start generating passive income?

You can begin building streams with surprisingly small amounts of capital. High-yield savings accounts and fractional shares of premium dividend stocks allow you to start earning extra money with as little as one hundred dollars. The ultimate key lies in the consistent, incremental restructuring of your assets rather than fruitlessly waiting until you have accumulated a massive lump sum.

Will passive income negatively affect my Social Security benefits?

Generally, pure investment income like standard dividends, interest, and capital gains do not count toward the specific earned-income limit that temporarily reduces Social Security benefits for those who claim early. However, these lucrative income streams do strongly factor into your combined provisional income, which ultimately determines whether your actual Social Security benefits become subject to federal taxation.

Is renting out my property considered truly passive?

No traditional property rental operates as entirely passive. It squarely falls into the demanding category of semi-passive income. You still must diligently deal with late-night tenant communications, occasional emergency maintenance, and stressful vacancy periods. Utilizing a professional property management company makes the endeavor significantly more passive, though their standard monthly fees will noticeably reduce your overall profit margin.

How often should I review my passive income portfolio?

You should conduct a comprehensive review of your senior finances at least twice a year. Federal interest rates rapidly fluctuate, corporate dividend policies dramatically change, and your deeply personal cash flow needs inevitably evolve over time. Semiannual check-ins perfectly allow you to rebalance your entire portfolio and ensure your varied income vehicles still align with your long-term goals for financial freedom.

Your Next Step Toward Financial Freedom

Transforming your retirement years into a vibrant period of abundance requires deliberate, focused action starting today. You absolutely possess the necessary knowledge and the accessible tools to strategically optimize your current assets and generate reliable extra money. Start small by ruthlessly auditing your current cash flow and swiftly moving idle cash into high-yield accounts to secure immediate wins. Then, gradually explore the power of dividends, commercial real estate, and digital assets to build a remarkably robust, diversified safety net. Every single step you take fortifies your senior finances against raging inflation and unexpected expenses. You worked hard for your money; now it is unequivocally time to make your money work tirelessly for you.