Securing a comfortable post-career life requires finding flexible jobs for retirees that generate steady cash without consuming your hard-earned freedom. You need strategies that balance your need for extra money with your desire to travel, relax, and spend time with family. Middle-income households often face shrinking purchasing power as inflation chips away at fixed pensions and savings drawdowns. Earning a retirement side income relieves this daily financial pressure and provides a powerful mental boost. By leveraging the skills you spent decades building, you can transform free hours into meaningful economic security. Exploring these targeted senior money making ideas allows you to bridge the gap between your essential living expenses and your ultimate lifestyle goals.

The State of the Wallet: Why Retirees Are Returning to Work

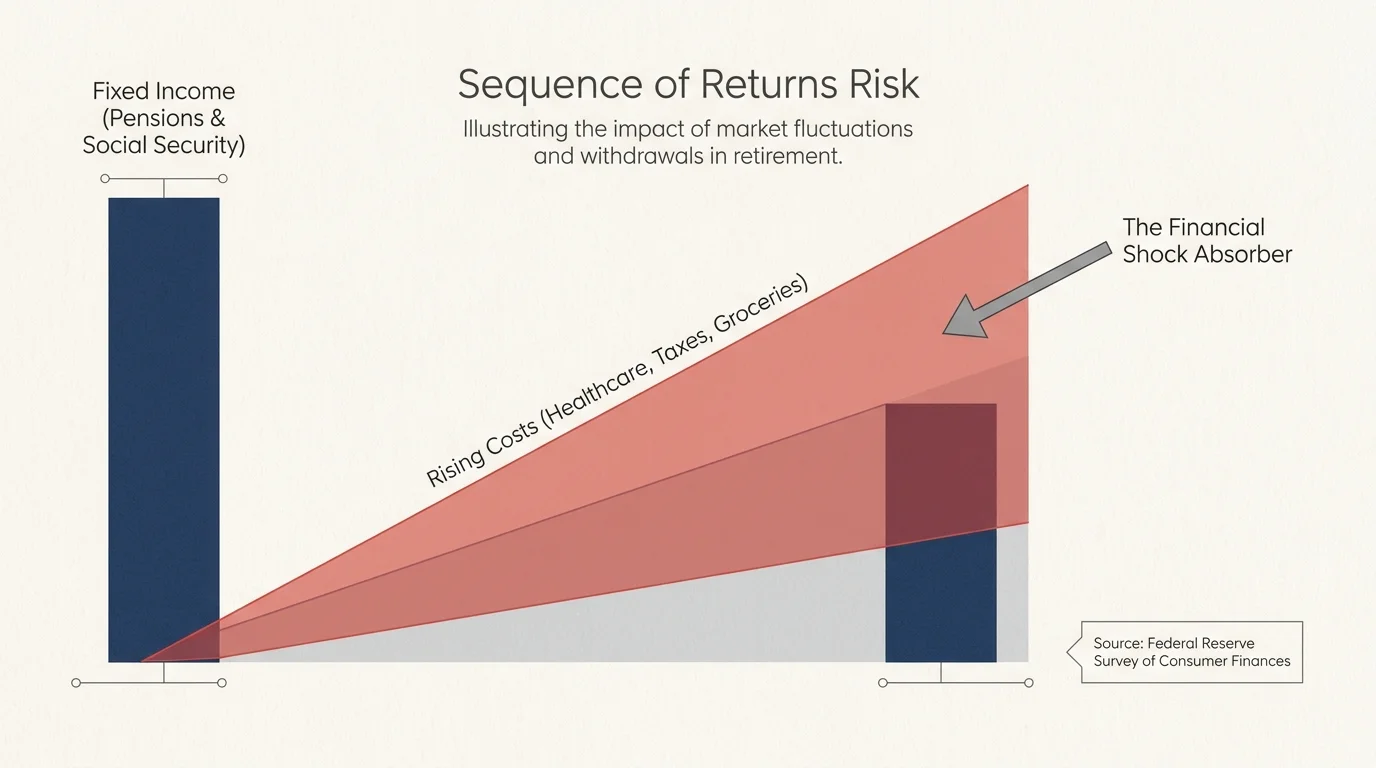

Many households reach their sixties only to realize their carefully constructed nest egg feels inadequate against the rising costs of healthcare, property taxes, and daily living. You carefully monitor your distributions and track every receipt, yet the math feels increasingly tight. Data from the Federal Reserve Survey of Consumer Finances routinely highlights the vulnerability of middle-income retirees, noting that average account balances often fall short of funding a thirty-year retirement without supplementary cash flow. You feel this reality every time you visit the grocery store or open a utility bill, realizing that your fixed income does not stretch as far as it did just a few years ago.

Consequently, the landscape of retirement is shifting dramatically. Older Americans remain in the labor force at unprecedented rates, not necessarily out of desperation, but out of a pragmatic desire to regain control over their household budgets. Projections from the Bureau of Labor Statistics indicate that workers aged sixty-five and older represent the fastest-growing segment of the modern labor force. Extra income after retirement acts as a crucial shock absorber against sudden economic shifts. When you earn even a modest amount through side gigs for seniors, you actively reduce your sequence of returns risk—the severe danger of drawing down your investment portfolio during a stock market downturn.

Generating active cash flow means you can leave your principal invested longer, allowing it to recover and compound over time. This structural shift in how we view our golden years transforms the traditional hard stop of retirement into a gentle, customizable glide path. Instead of abruptly leaving the workforce, you can blend well-deserved leisure with purposeful, profitable activity, ensuring your financial foundation remains robust well into your later years.

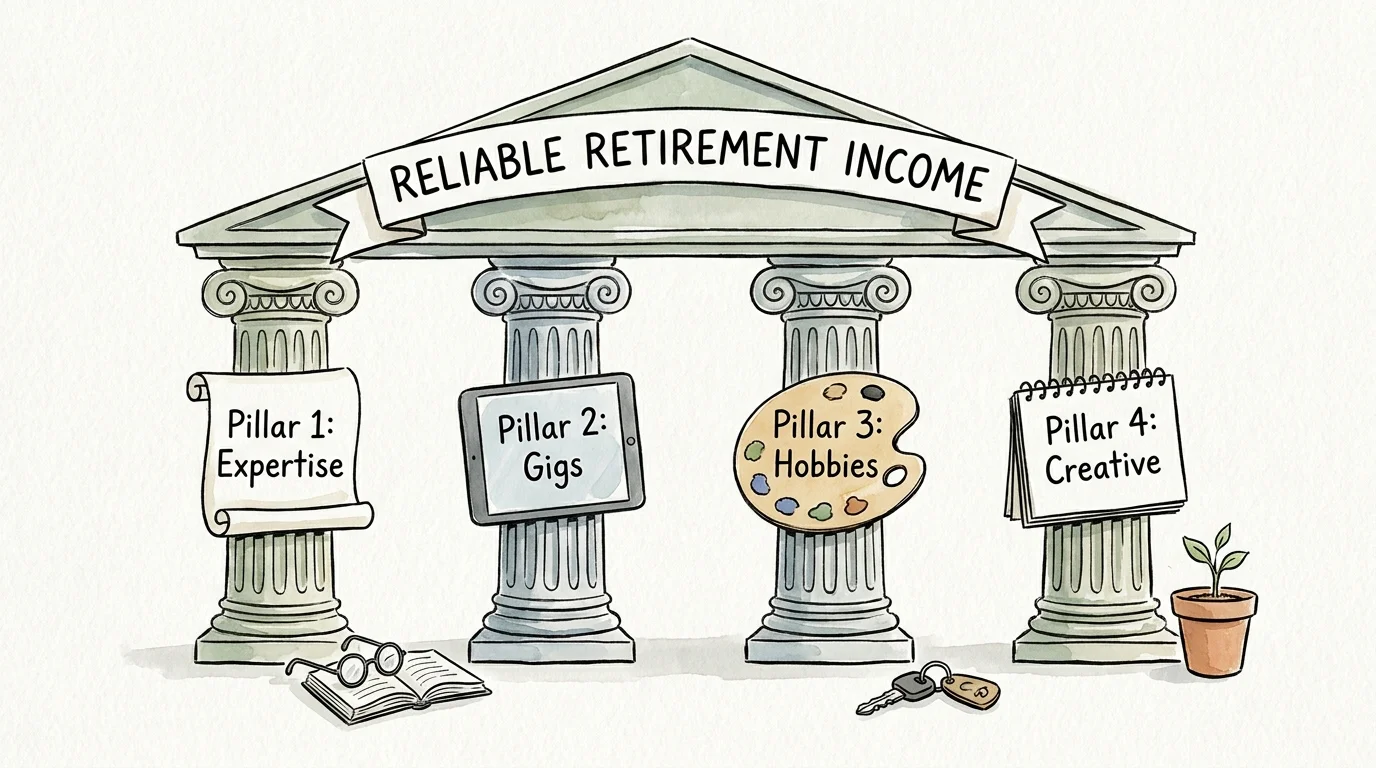

Strategy Pillars: Discovering Your Ideal Retirement Side Income

Building a sustainable income stream requires aligning your unique skills with market demands. Let us explore four core strategy pillars that house the most reliable and flexible jobs for retirees. By understanding these categories, you can select an approach that naturally fits your personality and lifestyle.

Pillar 1: Monetizing Lifelong Professional Expertise

After spending thirty or forty years in a specific industry, you possess a wealth of institutional knowledge that younger companies desperately need but often cannot afford on a full-time basis. You can package this expertise into highly lucrative, part-time opportunities. Our first idea is independent industry consulting. Instead of grinding through forty-hour weeks, you can contract with former employers or smaller local competitors to audit their operations, mentor junior executives, or manage short-term transition projects. Because you operate as an independent contractor, you set your hourly rate and dictate your availability, ensuring the work never intrudes on your personal life.

If consulting feels too corporate, our second idea is academic or professional tutoring. If you have a background in accounting, engineering, nursing, or education, your highly technical skills are marketable to university students or working professionals seeking board certification. Tutoring platforms and community colleges allow you to log on for just a few hours a week, share your expertise, and generate a predictable retirement side income without ever leaving your home office. You get to enjoy the intellectual stimulation of teaching without the bureaucratic headaches of traditional academia.

Pillar 2: Tapping Into the Flexible Gig Economy

The second pillar centers on the modern gig economy, which provides instant access to paying customers. This approach works best if you prefer tasks that keep you physically active and engaged with your local community. Idea number three is professional pet sitting and dog walking. Many middle-income retirees find immense joy and stress relief in caring for animals; this gig offers the dual benefit of mandatory daily exercise and immediate payment. You can easily build a small, trusted clientele in your own neighborhood through local community boards or dedicated apps, ensuring you never have to commute far or deal with difficult corporate managers.

Idea number four involves specialized local transportation. While driving for traditional late-night ridesharing services might feel overwhelming or unsafe, providing scheduled rides for fellow seniors addresses a massive community need. Local community centers, non-emergency medical transit services, and specialized apps often seek reliable, mature drivers. These organizations value older drivers who offer patience, defensive driving experience, and excellent conversational skills. You help your peers maintain their independence while padding your own savings account.

Pillar 3: Turning Hobbies and Space Into Cash Flow

Our third strategy pillar focuses on turning your existing passions and unused physical space into steady cash flow. Idea number five revolves around crafting and selling niche physical goods. If you spent your working years woodworking, knitting, painting, or refurbishing antique furniture as a weekend hobby, you can transition these passions into profitable small business ventures. You can showcase your work at local farmers markets, craft fairs, or through digital storefronts. The secret to success here is pricing your items at a premium to reflect your craftsmanship, deliberately avoiding the race to the bottom against mass-produced goods.

Idea number six maximizes your real estate assets through strategic space rentals. If you have downsized your daily life but still have an empty two-car garage, an unused driveway near a sports stadium, or a finished basement, you can rent these spaces out. Generating extra income after retirement becomes surprisingly effortless when you leverage the property you already own to provide long-term storage for boats and RVs, or secure parking solutions for your neighbors. It requires minimal ongoing physical effort once the initial rental agreement is signed.

Pillar 4: Administrative and Creative Freelancing

The final pillar is administrative and creative freelancing, which provides the ultimate location independence. This is perfect for retirees who plan to travel or split their time between different climates. Idea number seven is working as a specialized virtual assistant. Small business owners frequently struggle with managing their client inboxes, scheduling appointments, and handling basic bookkeeping. By offering just ten to fifteen hours of remote administrative support per week, you secure a reliable income stream while maintaining total freedom over your geographic location.

Idea number eight focuses on freelance writing, proofreading, and editing. Corporate blogs, trade magazines, and local businesses constantly need polished, authoritative content. If you have strong communication skills, you can pitch technical articles related to your former career field or offer to edit newsletters for local nonprofits. These senior money making ideas require nothing more than a reliable laptop and a basic internet connection, allowing you to earn money from a coffee shop in your hometown or a balcony on a cruise ship.

Real-World Voices: What Behavioral Economists Say About Working Longer

Behavioral economists and certified financial planners advocate strongly for maintaining a hybrid approach to your later years. Transitioning abruptly from a high-pressure career to a life of complete leisure often triggers a profound loss of identity and sudden social isolation. Maintaining a part-time professional footprint provides a psychological anchor during this massive life transition. Experts emphasize that the benefits of earning extra income after retirement extend far beyond the balance sheet; the daily routine of work provides vital structure to your week.

Research compiled by the National Council on Aging indicates that older adults who maintain part-time employment consistently report higher levels of life satisfaction and a delayed onset of age-related cognitive decline. Earning a retirement side income validates your ongoing utility to society and keeps your mind sharp. You remain plugged into the broader economic conversation, engaging with new technologies and diverse groups of people.

This engagement fundamentally shifts your mindset from that of a passive consumer to an active, contributing producer. This renewed sense of purpose is a critical component of holistic financial wellness. It proves that a truly successful retirement is about managing your mental and emotional health just as effectively as you manage your monetary assets.

Action Lab: Calculating Your True Side Income Needs

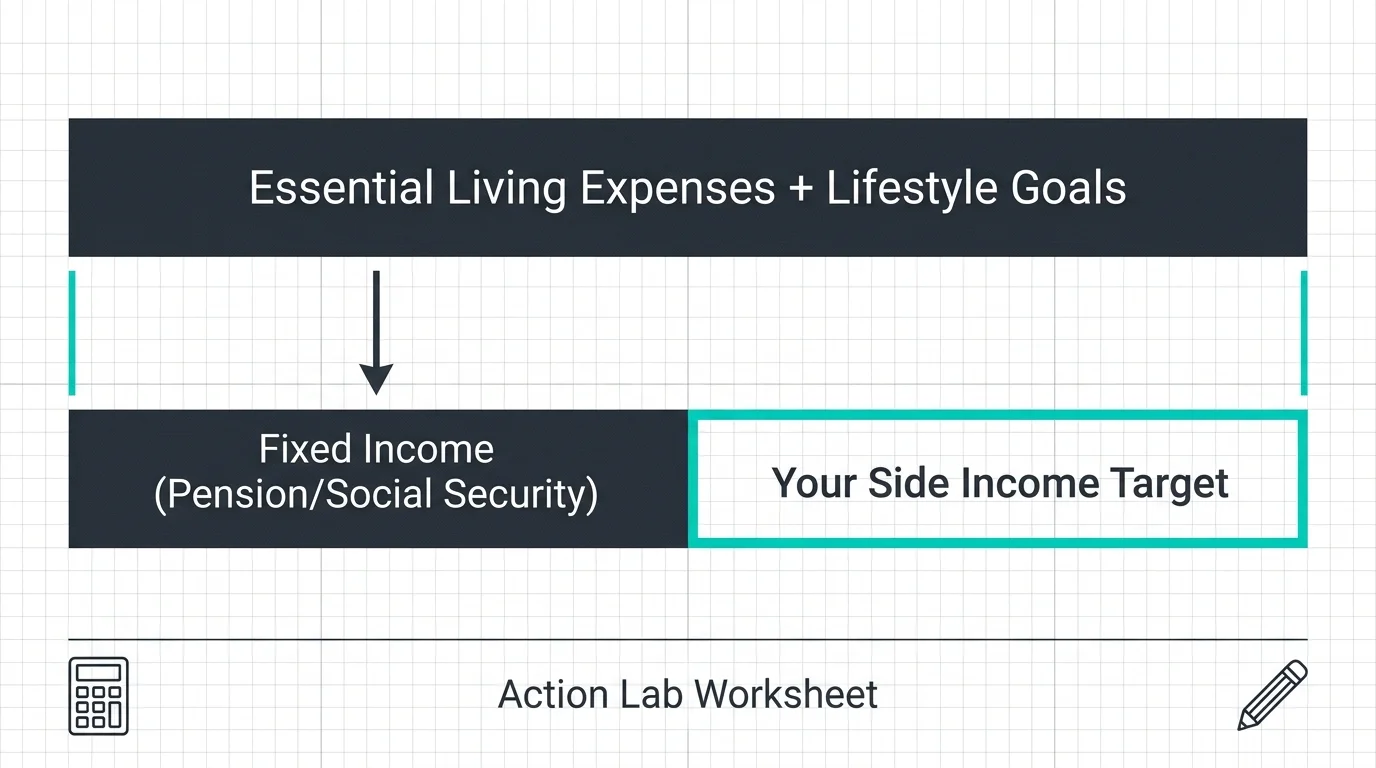

To integrate these strategies successfully without feeling overwhelmed, you must conduct a thorough cash-flow audit and calculate your exact earning targets. Let us walk through a practical example of how to right-size your side hustle goals. Suppose you sit down and determine that your essential monthly expenses—covering housing, food, Medicare premiums, and utilities—total four thousand dollars. However, your combined Social Security and pension distributions only provide three thousand five hundred dollars. You face a structural monthly deficit of five hundred dollars.

Instead of withdrawing that five hundred dollars from a volatile investment account, you decide to leverage idea number seven and offer virtual bookkeeping services to a local plumber. If you charge twenty-five dollars an hour, you only need to work twenty billable hours per month to completely cover your shortfall. That breaks down to just five hours a week, or roughly one hour a day. By viewing your required retirement side income through this micro-lens, the task feels entirely manageable and highly achievable.

Once you establish this income, you must actively protect it. You can easily automate your financial workflow by directing any surplus gig earnings immediately into a high-yield savings account. The Consumer Financial Protection Bureau strongly recommends setting up completely separate checking and savings accounts for your gig income. This simple banking automation prevents subtle lifestyle creep, organizes your bookkeeping for tax season, and ensures your extra funds remain strictly dedicated to your long-term security.

Guardrails and Pitfalls: Protecting Your Time and Benefits

While pursuing flexible jobs for retirees offers numerous advantages, you must navigate several crucial guardrails to protect your time, your identity, and your federal benefits. The most significant pitfall involves misunderstanding how earned income impacts your Social Security benefits if you claim them before reaching your full retirement age. The Social Security Administration enforces strict annual earnings limits for early claimers; if you exceed this threshold, they will temporarily withhold a significant portion of your monthly benefits. You must meticulously track your gross gig earnings to ensure your side hustle does not inadvertently penalize your primary fixed income stream.

Additionally, you must remain incredibly vigilant against predatory schemes targeting older adults looking for remote work. The AARP Fraud Watch Network routinely highlights sophisticated employment scams that demand upfront payment for bogus training materials, background checks, or home office equipment. You must remember a cardinal rule of freelance work: a legitimate employer or client will never ask you to pay your own money for the privilege of working for them. If a remote job offer seems too good to be true and requires a credit card number to start, walk away immediately.

Finally, you must carefully consider the tax implications of independent contractor work. Because income taxes are not automatically withheld from your freelance checks or app payments, you are entirely responsible for paying them later. You must proactively set aside roughly twenty to twenty-five percent of your gross gig earnings in a separate account to cover federal and state self-employment taxes. Failing to prepare for this mandatory obligation can result in a painful financial surprise when you file your annual tax return in April.

Frequently Asked Questions About Side Gigs for Seniors

How much do I need to earn to make a noticeable difference?

You might wonder if working just a few hours a week is actually worth the effort. The reality is that earning even two to three hundred dollars a month creates substantial breathing room in a fixed budget. This modest amount easily covers fluctuating grocery costs, unexpected healthcare copays, or helps build a dedicated travel fund. By removing the stress of these variable expenses, a small side income dramatically improves your overall quality of life.

Do I need advanced technological skills to succeed in the gig economy?

Many older adults hesitate to explore modern freelance work because they fear the technology barrier. You absolutely do not need to be a software developer to thrive today. Most freelance platforms, scheduling apps, and communication tools require only basic computer literacy—skills you likely already possess from using email or social media. Furthermore, numerous free online tutorials cater specifically to beginners, allowing you to easily master the specific platforms necessary to manage your new venture.

Will taking on a side job ruin the relaxation of my retirement?

A common fear is that returning to work will feel like stepping back into the corporate rat race. The secret to a successful retirement gig lies in rigorous boundary management. Because you dictate your own hours and choose your clients, you can schedule your work strictly around your life, not the other way around. If a particular client becomes overly demanding or a gig feels too stressful, you possess the ultimate luxury: the financial freedom to simply walk away and choose a different, more relaxing path.

Should I form an LLC for my retirement side gig?

When you start earning independent income, the question of legal structure inevitably arises. For most casual side gigs—like occasional tutoring, freelance writing, or pet sitting—operating as a simple sole proprietor is perfectly sufficient and requires zero initial paperwork. However, if your chosen venture involves physical risk to others, or if you begin earning substantial commercial revenue, consulting with a certified public accountant about establishing a Limited Liability Company provides valuable personal asset protection.

Stepping Confidently Into Your Next Chapter

Reimagining your post-career life opens the door to immense personal growth and profound financial relief. You have spent decades acquiring valuable skills, mastering interpersonal communication, and building a strong work ethic. There is absolutely no reason to lock those assets away the moment you stop working full-time. Instead, you can selectively deploy your talents on your own terms, transforming your spare time into a powerful financial buffer.

Your challenge this week is straightforward: review the eight ideas detailed above and select just one that sparks your interest. Spend thirty minutes researching local demand or exploring a relevant freelance platform. Taking that initial, low-stakes step demystifies the process and builds immediate momentum. By embracing the flexibility of modern part-time work, you take definitive control over your financial destiny, ensuring your retirement is defined by abundance, purpose, and peace of mind.