State aging agencies provide a treasure trove of free and reduced-cost services designed to keep retirees financially secure. By tapping into these localized senior services, you can stretch your fixed income further while accessing essential resources like nutrition assistance, utility relief, and caregiver support. Managing money in retirement often feels like plugging a leaky dam, especially when unexpected expenses arise. Instead of depleting your savings to cover rising costs, leverage the aging resources funded by the Older Americans Act. These programs exist specifically to help middle-income households navigate the financial pressures of getting older. Understanding exactly what your local Area Agency on Aging offers is the first step toward building a more resilient retirement budget.

State of the Wallet: The Rising Cost of Aging

The financial landscape for modern retirees looks vastly different than it did a decade ago. If you feel like your fixed income buys less at the grocery store and the pharmacy, the economic data validates your experience. Recent consumer research highlights a growing gap between standard Social Security cost-of-living adjustments and the actual inflation experienced by older adults, particularly in essential categories like healthcare and housing. Many middle-income households find themselves in a frustrating gray zone; you might have too much in savings to qualify for federal poverty programs, but not enough wealth to absorb consistent price hikes without financial stress. This squeeze forces families to make impossible choices between refilling necessary prescriptions and keeping the thermostat at a comfortable temperature.

Recognizing this widespread vulnerability, the government funnels resources through the Older Americans Act to local levels. According to research published by the Consumer Financial Protection Bureau, a significant percentage of older adults struggle to absorb an unexpected financial shock of just a few hundred dollars. Area Agencies on Aging step into this gap to provide a localized safety net that protects your hard-earned nest egg. These agencies operate in every state, acting as central hubs for senior assistance designed to maintain your independence and financial dignity. By understanding the breadth of these offerings, you can reclaim control over your monthly cash flow and redirect your funds toward the aspects of retirement you actually enjoy.

Strategy Pillar One: Unlocking Nutrition and Preventive Health Resources

Food costs remain one of the most volatile line items in any household budget; state aging agencies offer powerful tools to help you stabilize this expense. Through localized nutrition programs, you can access fresh, healthy meals that reduce your grocery bill while supporting your overall well-being. The most recognized of these initiatives is the Meals on Wheels program, which delivers prepared food directly to your door. However, many retirees overlook congregate meal sites hosted at local senior centers or community halls. These community meals provide an excellent opportunity to socialize while enjoying a nutritious lunch for a nominal, voluntary donation. Because heavy subsidies back these programs, participating can easily shave fifty to one hundred dollars off your monthly food expenses.

Beyond the dining table, aging resources frequently encompass preventive health and wellness services. State agencies coordinate evidence-based programs focused on chronic disease self-management, fall prevention, and diabetes care. By participating in these free or low-cost workshops, you gain practical strategies to manage your health proactively. This preventative approach directly impacts your wallet by reducing the likelihood of expensive emergency room visits or prolonged hospital stays. Furthermore, many agencies partner with local health departments to offer free vaccination clinics and basic health screenings for blood pressure and cholesterol. Utilizing these localized senior services allows you to protect your physical health without paying steep co-pays at a traditional medical clinic.

Strategy Pillar Two: Slashing Utility and Housing Costs

Keeping a roof over your head and the lights on consumes a massive portion of any retirement budget. State aging agencies act as vital conduits for programs that dramatically reduce your monthly overhead. One of the most impactful resources is the Low Income Home Energy Assistance Program, commonly referred to as LIHEAP. While the name implies a strict poverty requirement, many states implement sliding scale eligibility criteria that accommodate middle-income retirees facing high energy burdens. Local aging advocates can help you navigate the application process to secure grants that pay a portion of your heating and cooling bills directly to your utility provider.

In addition to direct bill assistance, your local agency can connect you with robust weatherization programs. These initiatives provide free home energy audits and fund essential upgrades—such as adding attic insulation, sealing drafty windows, or repairing inefficient heating systems. Upgrading your home’s energy efficiency delivers compounding returns, permanently lowering your monthly utility expenses without requiring any upfront capital from your savings. Furthermore, state aging agencies frequently maintain directories of localized property tax relief programs. Many municipalities offer significant property tax exemptions or deferrals specifically for senior citizens, yet these benefits require proactive applications. Securing a property tax freeze or a substantial reduction can instantly free up hundreds of dollars a month, transforming a tight budget into one with comfortable breathing room.

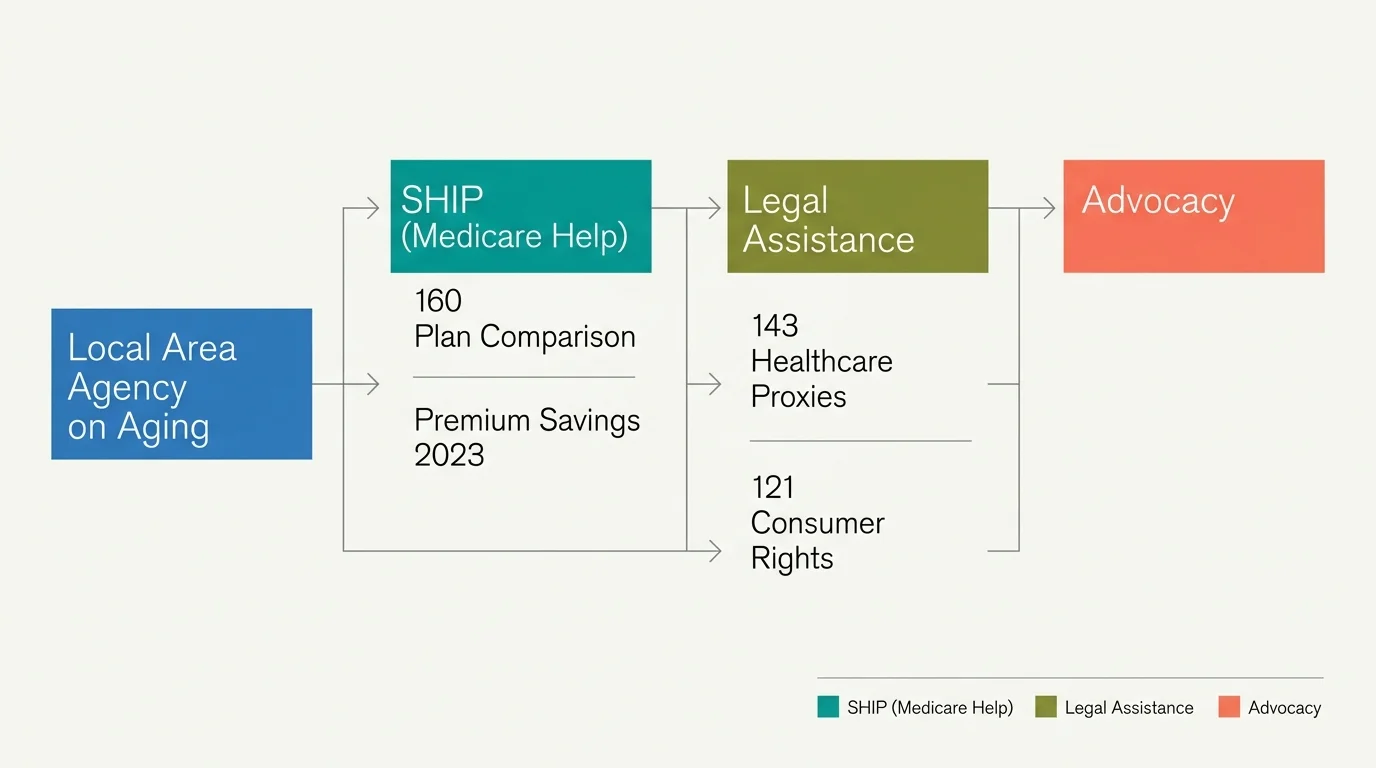

Strategy Pillar Three: Navigating Medicare and Legal Assistance

Navigating the complexities of healthcare insurance often feels like a full-time job, and selecting the wrong plan can cost you thousands of dollars in uncovered medical expenses. Fortunately, state aging agencies manage the State Health Insurance Assistance Program, which provides free, unbiased Medicare counseling. Unlike insurance brokers who earn commissions based on the policies they sell, these state-funded counselors offer objective advice tailored entirely to your medical needs and financial situation. They will sit down with you to review your current prescriptions, analyze your preferred doctors, and compare available Medicare Part D and Medicare Advantage plans in your zip code. Switching to a more optimized plan during the annual open enrollment period frequently yields massive savings on prescription drug costs and monthly premiums. You can learn more about finding these counseling services directly through authoritative hubs like Medicare.gov.

Equally important is the subsidized legal assistance coordinated by these agencies. Hiring a private attorney to draft estate documents or resolve civil disputes carries a hefty price tag that many retirees simply cannot afford. Through the Older Americans Act, local agencies partner with legal aid societies to offer free or deeply discounted legal services for older adults. These legal professionals can help you draft living wills, establish powers of attorney, and navigate complex landlord-tenant disputes. Securing your estate and protecting your consumer rights without draining your bank account provides profound peace of mind, ensuring that your assets remain secure for your use and your family’s future.

Real-World Voices: Insights from Financial Planners

Financial planners who specialize in retirement income consistently emphasize the importance of leveraging community resources, yet they observe a recurring psychological barrier among their clients. Many middle-income retirees hesitate to utilize state senior assistance programs due to a misplaced sense of pride or the mistaken belief that these services should be reserved exclusively for the destitute. Behavioral economists refer to this phenomenon as benefit friction; the combination of social stigma and bureaucratic complexity prevents households from claiming the financial support they desperately need.

Wealth advisors argue that you must reframe how you view these aging resources. You spent decades paying taxes into the very systems that fund the Older Americans Act. Utilizing a state-funded legal clinic or consulting with a Medicare counselor is not a handout; it is the realization of a benefit you actively financed during your working years. Consumer research firms studying retirement readiness note that households willing to engage with their Area Agency on Aging demonstrate significantly higher financial resilience. By overcoming the initial hesitation and making that first phone call, you unlock a hidden tier of your retirement portfolio. Financial experts advise treating your local aging agency like a trusted financial advisor—one who charges no fees and works exclusively to keep your money in your pocket.

Action Lab: A Step-by-Step Benefit Audit

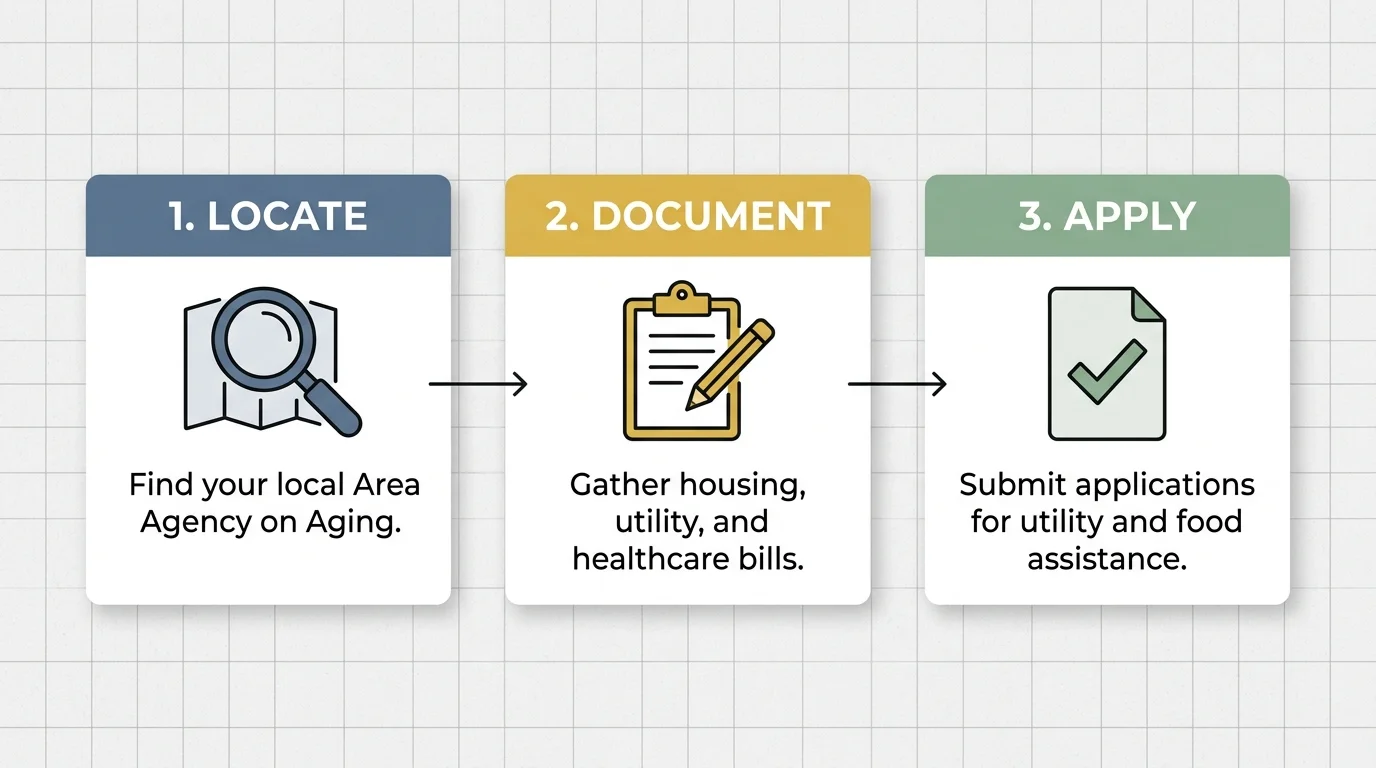

Theory only takes you so far; applying these concepts requires a dedicated action plan. Let us walk through a practical scenario to illustrate how a systematic benefit audit can transform your financial trajectory. Imagine you currently spend a significant portion of your fixed income on groceries, high utility bills, and expensive prescription co-pays. Your first step is to locate your specific Area Agency on Aging using the Eldercare Locator administered by the federal government. Once you identify your local office, you will schedule a comprehensive benefits screening.

During this screening, you discover that you qualify for a state-sponsored pharmacy assistance program that reduces your out-of-pocket medication costs by sixty dollars a month. Next, the agency connects you with a local weatherization program that seals your home, slashing your winter heating bill by an average of forty dollars a month. Finally, you sign up for a community congregate meal program twice a week, which offsets roughly fifty dollars of your monthly grocery spending. When you add these up, you have effectively reclaimed one hundred and fifty dollars every single month. Over the course of a year, that translates to eighteen hundred dollars in pure cash flow. Instead of letting that money evaporate into everyday expenses, you can automate a transfer, moving that newly found capital directly into a high-yield savings account. This step-by-step audit proves that small, localized interventions compound rapidly into massive financial relief.

Guardrails and Pitfalls: Avoiding Common Mistakes

While state aging agencies offer incredible value, navigating the landscape of senior assistance requires vigilance and strategic thinking. The most common mistake retirees make is self-disqualifying based on assumptions about income limits. Because programs operate under different funding streams, eligibility rules vary wildly. A program offering property tax relief might have strict income caps, while a caregiver support initiative might be available to anyone over the age of sixty, regardless of wealth. Never assume you earn too much to receive help; always let the agency professionals conduct a formal screening. You can also utilize digital screening tools provided by organizations like the National Council on Aging to independently cross-reference your eligibility for various state and federal programs before you make a call.

Another critical pitfall involves falling prey to sophisticated scams disguised as government assistance. Criminals frequently target older adults with fraudulent phone calls or emails, claiming to represent state agencies and demanding immediate payment or personal banking details to unlock benefits. Legitimate Area Agencies on Aging will never pressure you for immediate payment or ask for your bank routing number over an unsolicited phone call. If you suspect fraudulent activity, report it immediately to the Federal Bureau of Investigation, which maintains resources dedicated to elder fraud prevention. Finally, avoid the trap of bureaucratic fatigue. Applying for state resources sometimes involves paperwork and waiting lists. Giving up after a single confusing application means leaving thousands of dollars on the table.

Frequently Asked Questions About Senior Assistance Programs

What is the difference between a state aging agency and a local Area Agency on Aging?

The state aging agency serves as the centralized governing body that receives federal funds and establishes statewide policies. The local Area Agency on Aging operates directly in your specific county or region. The local agency acts as the direct service provider, meaning you will interact with the local office to apply for programs, attend workshops, and receive tailored assistance.

Are these retiree benefits only available to low-income households?

No; this is a pervasive myth that prevents middle-income families from seeking help. While certain resources like Medicaid require strict low-income thresholds, many programs funded by the Older Americans Act use sliding scales or base eligibility entirely on age. Services like unbiased Medicare counseling, caregiver support groups, and congregate meals are generally available to all seniors, making them excellent resources for middle-income households looking to optimize cash flow.

How long does it typically take to get approved for senior assistance?

Approval timelines vary significantly based on the specific program and your geographic location. Crisis interventions, such as emergency utility assistance to prevent a winter shut-off, can be processed in a matter of days. Conversely, programs requiring extensive home assessments, like structural weatherization upgrades, might involve waiting lists that stretch for several months. Initiating contact with your local agency early ensures you are positioned to receive help when you need it most.

Can my adult children apply for aging resources on my behalf?

Yes, adult children or designated caregivers can seamlessly facilitate the application process. State agencies recognize that family members often bear the administrative burden of managing a loved one’s care. Many Area Agencies on Aging feature dedicated caregiver support divisions specifically designed to help your adult children navigate the paperwork, coordinate meal deliveries, and secure respite care services on your behalf.

Empower Your Retirement Finances Today

Securing your financial comfort in retirement requires a proactive approach to managing your overhead costs. You have spent a lifetime building your nest egg, and you deserve to stretch those funds as far as possible without sacrificing your quality of life. The free and reduced-cost services provided by state aging agencies represent a powerful, underutilized toolkit for middle-income households. By taking the time to uncover localized nutrition programs, secure utility relief, and optimize your healthcare coverage through unbiased counseling, you can significantly reduce the pressure on your monthly budget.

Your next step is clear and highly actionable. Set aside thirty minutes this week to locate your regional Area Agency on Aging online or via a quick phone call. Request a comprehensive benefits screening and approach the conversation with an open mind. Treat this exercise just like a strategic meeting with a financial planner; every dollar you save on basic necessities is a dollar you can redirect toward family, hobbies, and peace of mind. Embrace these aging resources as the dividends of your lifelong contributions to your community, and take control of your financial future today.