Navigating retirement costs requires a sharper strategy today, as persistent economic shifts reshape the cost of living for seniors across the country. You worked decades to build a comfortable nest egg, but sudden price hikes on everyday essentials can quickly erode your hard-earned financial security. From higher property taxes to unpredictable medical bills, specific expenses are squeezing middle-income households harder than expected under current fiscal policies. By identifying these five core pressure points, you can implement protective budgeting techniques that stretch your fixed income further. We strip away the financial jargon to give you actionable steps to audit your cash flow and shield your retirement savings from immediate economic headwinds.

State of the Wallet: The New Economic Reality for Retirees

The macroeconomic landscape has shifted dramatically, introducing a unique set of challenges for middle-income households transitioning into or currently navigating their golden years. Recent fiscal policies prioritizing domestic manufacturing and tariffs have altered global supply chains, leading to a complex dynamic where certain sectors thrive while everyday consumer costs remain stubbornly elevated. For retirees living on fixed incomes, this combination of shifting tax codes and fluctuating market conditions creates an undeniable financial squeeze. You are not dealing with a simple case of historical inflation; you are managing a structural realignment of where your money goes each month.

When you examine recent Federal Reserve monetary policy reports, the data illustrates a clear division between wage growth for active workers and the purchasing power of fixed-income portfolios. While current economic policies aim to stimulate domestic growth, the immediate side effect for seniors is a heightened sensitivity to price volatility in non-discretionary categories. The relationship between inflation and retirees is particularly fraught right now because you cannot easily ask a boss for a raise to offset higher bills. Instead, your defense relies entirely on tactical money management and proactive adjustments to your withdrawal strategies.

Middle-income retirees face a particularly frustrating middle ground in this economy. You likely earn too much from Social Security and retirement accounts to qualify for crucial low-income assistance programs, yet you do not possess the sweeping generational wealth required to safely ignore rising costs. This reality demands a transition from passive budgeting to active cash-flow defense. Understanding exactly which expenses are draining your accounts is the first necessary step toward regaining control of your financial independence.

The 5 Expenses Squeezing Retiree Wallets Right Now

1. Unpredictable Healthcare and Prescription Drug Costs

Healthcare has long been the wildcard of retirement planning, but recent economic pressures have accelerated the financial burden on seniors. While Medicare provides a vital safety net, it does not function as an absolute shield against out-of-pocket expenses. Base premiums for Medicare Part B continue to inch upward, consuming a larger percentage of your annual Social Security cost-of-living adjustments before the money ever reaches your bank account. Supplemental insurance policies, often necessary to cover the gaps in traditional Medicare, are also repricing their risk models, resulting in steeper monthly bills for policyholders.

Prescription drugs present an even more volatile challenge. Trade policies and regulatory shifts impacting pharmaceutical supply chains frequently translate into higher prices at the pharmacy counter. Even with recent legislative efforts aimed at capping specific drug costs, numerous essential medications fall outside those protections. Comprehensive Kaiser Family Foundation research consistently highlights how out-of-pocket healthcare limits can devastate a modest retirement budget. If you require specialized treatments or brand-name maintenance medications, you must ruthlessly compare Part D plans during every single Open Enrollment period to prevent these costs from quietly draining your reserves.

2. Surging Property Taxes and Home Maintenance

Owning your home outright is a traditional cornerstone of the American retirement dream, yet the ongoing costs of keeping that home have skyrocketed. Local municipalities, facing their own budgetary shortfalls and rising operational costs, frequently turn to property tax reassessments to close the gap. Because housing demand remains robust in many regions, property valuations have surged. While a higher home value looks fantastic on paper, it triggers substantially higher property tax bills that you must pay using the same fixed monthly income.

Simultaneously, the cost of maintaining aging real estate has surged. Tariffs on imported building materials—such as lumber, steel, and electrical components—directly inflate the cost of necessary home repairs. Finding affordable, skilled labor has also become increasingly difficult, driving up the price of everything from a simple plumbing fix to a major roof replacement. Retiree expenses in this category often catch households off guard because these costs do not arrive in predictable, monthly increments; they hit as massive, sudden shocks to your cash flow.

3. The Hidden Creep of Utility Bills

Keeping the lights on and the house comfortably heated or cooled requires a larger portion of your budget than it did a decade ago. Energy markets remain sensitive to geopolitical tensions and domestic regulatory changes, causing prolonged periods of price volatility for natural gas and electricity. Utility companies frequently pass the massive costs of modernizing aging grid infrastructure directly down to residential consumers through approved rate hikes and specialized delivery fees.

For seniors spending more time at home, energy consumption naturally increases. Running the air conditioning during increasingly hot summer afternoons or turning up the thermostat during winter freezes directly impacts your monthly bottom line. These bills represent a significant threat to the cost of living for seniors because they are largely non-negotiable. You can only lower the thermostat so much before compromising your comfort and health, making utility inflation one of the most stubborn hurdles in your financial planning.

4. Rising Grocery and Everyday Consumer Goods

Trips to the supermarket provide the most visible and frequent reminder of shifting economic tides. While broad inflation metrics may occasionally show cooling trends, the actual prices on the grocery store shelves rarely retreat to their previous baselines; they simply stop increasing as rapidly. Trade tariffs and domestic labor shortages across the agricultural and transportation sectors keep the baseline cost of food exceptionally high. Essential items like fresh produce, lean proteins, and dairy products demand a larger share of your wallet every week.

Tracking the Bureau of Labor Statistics consumer price index data reveals that food-at-home prices deeply impact middle-income households because groceries represent a non-negotiable slice of the monthly budget. To combat this, you must adopt hyper-vigilant shopping habits. This goes beyond simple coupon clipping; it requires modifying your meal planning around seasonal availability, leveraging bulk purchases for non-perishable goods, and heavily substituting expensive brand names for equally nutritious store-brand alternatives.

5. Increased Insurance Premiums for Auto and Home

The insurance industry is fundamentally recalibrating how it prices risk, and retirees are caught squarely in the crosshairs. Severe weather events, increased replacement costs for vehicles, and higher litigation expenses have prompted massive underwriting losses for major carriers. To recover, insurance companies are aggressively raising premiums across the board, sometimes hiking rates by twenty percent or more in a single year, even if you have maintained a flawless driving record and never filed a homeowner’s claim.

These sudden premium hikes disrupt carefully planned retirement costs because they represent massive, recurring obligations. When your auto insurance jumps by hundreds of dollars annually and your home insurance follows suit, the money must be pulled from other discretionary categories. You can no longer rely on brand loyalty to secure the best rates; you must aggressively shop your policies with independent brokers annually and consider adjusting your deductibles to keep your monthly premiums manageable.

Strategic Pillars to Protect Your Fixed Income

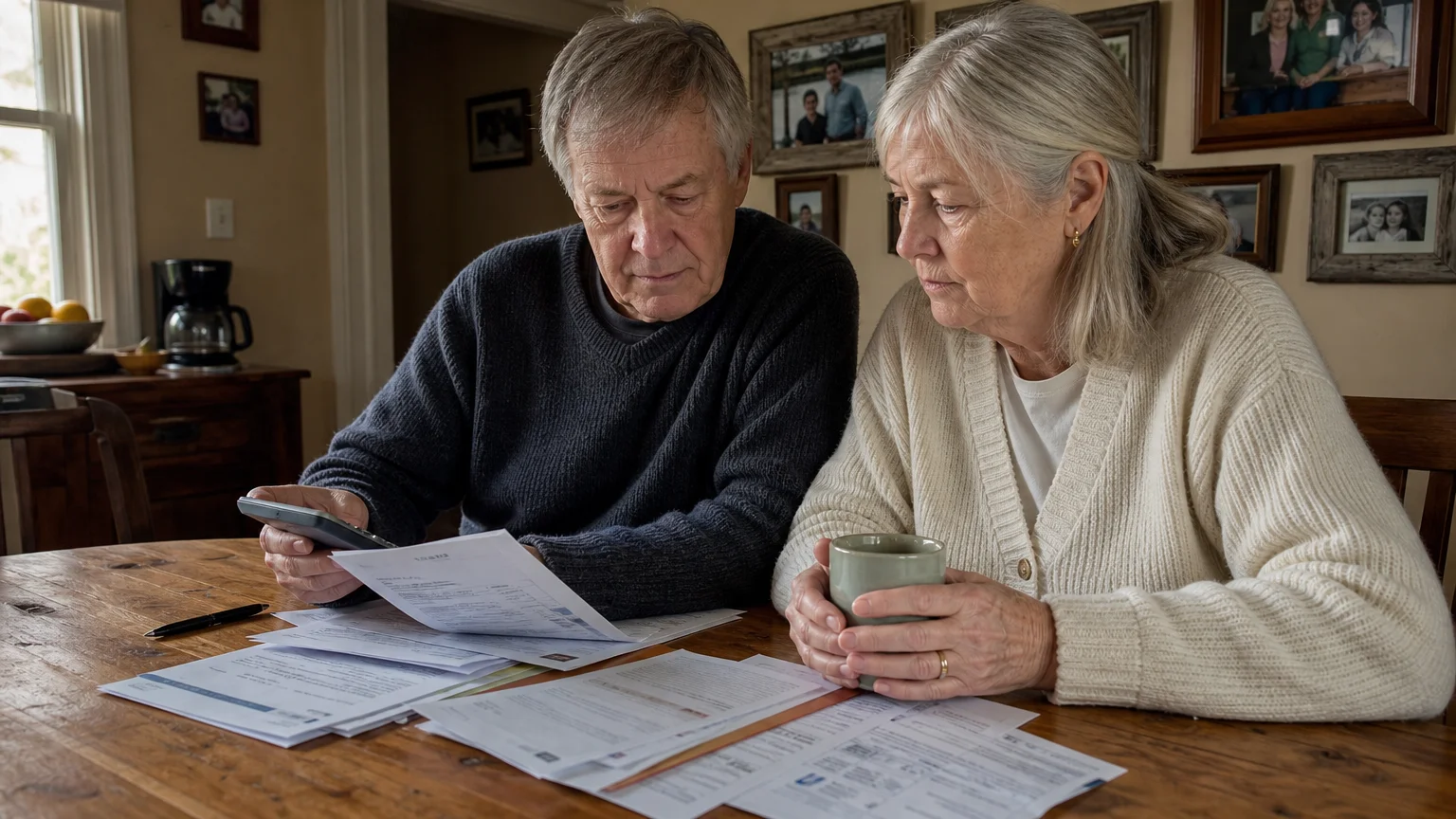

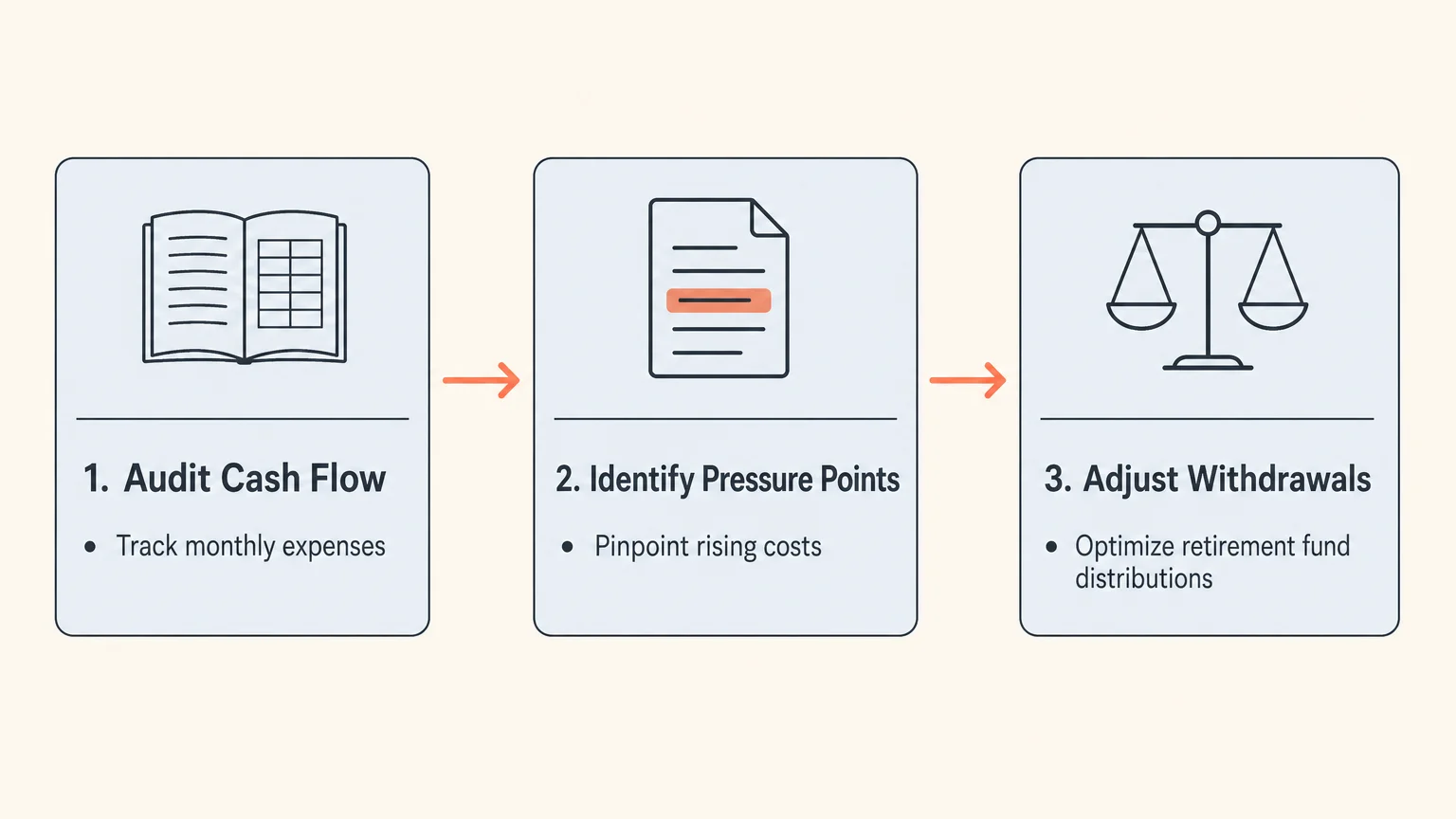

Conduct a Comprehensive Cash Flow Audit

You cannot defend your portfolio against rising costs if you do not know exactly where your money is flowing. A comprehensive cash flow audit involves scrutinizing three months of bank and credit card statements to categorize every single outbound dollar. This exercise strips away assumptions and reveals the stark reality of your current spending habits. You will likely discover recurring subscription services you no longer use, excessive spending on convenience meals, or insurance policies that overlap.

Once you categorize your spending into essential and discretionary buckets, you can establish a robust baseline for your retirement budgeting. Treat this audit as a diagnostic tool rather than a restrictive punishment. By identifying the exact dollar amount required to keep your household running—your true baseline—you empower yourself to make informed, strategic decisions about how to allocate the remainder of your income toward quality-of-life enhancements.

Automate Your Savings and Bill Pay Mechanisms

Financial automation removes the emotion and hesitation from saving money. In an environment where every dollar counts, maximizing the yield on your cash reserves is critical. Open a high-yield savings account that keeps pace with current interest rates, and set up automated transfers that trigger the moment your Social Security or pension checks deposit. Directing a specific percentage of your income into separate digital envelopes—such as a dedicated property tax fund or a medical deductible fund—ensures the money is reserved before you have a chance to spend it.

Automating your fixed household bills also protects you from costly late fees and secures potential auto-pay discounts offered by utility and telecom providers. When you segment your cash flow automatically, you create a psychological boundary; the money sitting in your primary checking account is safe to spend, while your major impending obligations are already funded and growing securely in a high-yield environment.

Implement Mindful Spending Frameworks

Mindful spending requires aligning your daily purchases with your overarching retirement values. Before making any non-essential purchase over a certain threshold—for example, one hundred dollars—enforce a strict forty-eight-hour waiting period. This simple behavioral hurdle eliminates impulse buying and provides the necessary time to evaluate whether the purchase genuinely enhances your quality of life or merely offers a fleeting dopamine hit.

This framework is not about depriving yourself of joy; it is about ensuring your money flows toward experiences and items that actually matter to you. If traveling to see your grandchildren is your primary goal, mindful spending helps you gladly decline expensive local dining options to fund those plane tickets. By intentionally directing your resources, you reclaim power over your budget regardless of the broader economic climate.

Real-World Voices and Expert Perspectives

Conversations with fiduciary wealth managers and behavioral economists consistently reveal a shared theme: the psychological transition from wealth accumulation to wealth distribution is profoundly stressful. When you spend forty years saving money, actively drawing down those accounts can trigger deep financial anxiety, especially when external economic factors drive prices higher. Experts emphasize that acknowledging this anxiety is a crucial step in preventing irrational financial decisions, such as hoarding cash in zero-interest accounts out of fear or abandoning well-diversified investment portfolios during temporary market dips.

To combat this stress, financial planners advocate for building significant cash buffers. Maintaining one to two years of living expenses in liquid, safe vehicles prevents you from selling investments at a loss during market downturns. Exploring Consumer Financial Protection Bureau resources for older adults can provide further empirical validation for these strategies, offering blueprints on how to structure your withdrawals to minimize tax liabilities and preserve principal. The consensus is clear: flexibility and proactive planning are your greatest shields against economic unpredictability.

Action Lab: Rebalancing Your Monthly Budget

Let us translate these concepts into a tangible exercise you can execute at your kitchen table tonight. Imagine your household brings in four thousand dollars a month from combined Social Security benefits and modest portfolio withdrawals. During your cash flow audit, you discover that your utility bills have increased by seventy-five dollars a month over the past year, and your grocery expenses have climbed by one hundred and fifty dollars. You are now running a hidden deficit of two hundred and twenty-five dollars monthly, which you have unknowingly been covering by dipping into your emergency savings.

To rebalance this equation, you must locate two hundred and twenty-five dollars in discretionary reductions. You review your spending and decide to cancel a premium cable package, saving ninety dollars. You then replace one weekly restaurant dinner with a home-cooked meal, recovering another one hundred and forty dollars. You have successfully freed up two hundred and thirty dollars. Instead of leaving this money to be accidentally spent, you immediately set up an automatic monthly transfer moving that exact amount into a high-yield savings account designated for household inflation costs. You have now neutralized the threat without permanently sacrificing your lifestyle.

Common Guardrails and Financial Pitfalls to Avoid

When fixed incomes feel tight, the temptation to rely on high-interest credit cards to bridge the gap becomes dangerous. Utilizing credit cards for daily expenses to earn points is mathematically sound only if you pay the balance in full every single month. Carrying a balance in a high-interest-rate environment compounds your financial stress rapidly, as interest charges quickly outpace any inflationary increases on consumer goods. You must fiercely protect your balance sheet from toxic debt.

Another major pitfall involves ignoring the power of optimized investment allocations. Fearing market volatility, some retirees shift their entire portfolios into cash. While cash is safe from market drops, it is entirely exposed to inflation risk. Failing to maintain a balanced allocation that includes growth-oriented assets virtually guarantees that your purchasing power will decline over a twenty-year retirement. Reviewing U.S. Securities and Exchange Commission guidance on saving can reinforce the importance of maintaining a diversified portfolio tailored to your specific time horizon and risk tolerance.

Frequently Asked Questions About Retirement Budgeting

How often should I adjust my portfolio withdrawal rate?

You should evaluate your withdrawal rate annually, ideally during a comprehensive year-end financial review. If your portfolio has experienced significant growth, you might safely increase your distribution to combat higher living costs. Conversely, during sustained market downturns, temporarily reducing your discretionary withdrawals protects your principal from sequence-of-returns risk. Flexibility is far more sustainable than adhering strictly to an outdated, rigid withdrawal percentage.

Are there state or local programs to help with rising property taxes?

Yes, many jurisdictions offer specific property tax relief programs for senior citizens. These can include property tax freezes, homestead exemptions, or deferral programs that delay tax payments until the home is sold. Because these programs are highly localized and rarely advertised, you must actively contact your county tax assessor’s office to inquire about eligibility requirements and application deadlines.

Does Medicare cover all my inflation-related healthcare costs?

No, original Medicare does not cover everything. It typically covers eighty percent of approved Part B services, leaving you responsible for the remaining twenty percent, with no annual out-of-pocket maximum. Furthermore, traditional Medicare does not cover routine dental, vision, or hearing care, which are significant expenses that naturally inflate over time. Securing a robust Medigap policy or carefully evaluating Medicare Advantage plans is essential to cap your financial exposure.

Should I pay off my mortgage early to reduce my monthly expenses?

The decision to pay off a mortgage depends heavily on your interest rate and your liquidity. If you hold a mortgage with a highly favorable, low fixed rate, the cash you would use to pay it off might earn a significantly higher return in a safe bond or high-yield savings account. However, if eliminating that monthly payment drastically improves your cash flow and provides profound psychological relief, prioritizing the payoff can be a valid, strategic choice.

Moving Forward with Financial Confidence

Economic landscapes will constantly evolve, shifting the exact nature of the financial pressures you face. While you cannot control federal trade policies, global supply chains, or the actions of central banks, you possess complete authority over your household cash flow. By confronting these five rising costs head-on, executing a thorough audit, and deliberately redirecting your resources, you build a resilient financial fortress. Challenge yourself this week to review your largest recurring expense and take one concrete step toward optimizing it; that single action will immediately begin fortifying your financial independence for the years ahead.