Trading your high-cost zip code for a picturesque small town can instantly stretch your retirement savings while dramatically upgrading your daily quality of life. Middle-income households often feel crushed by the rising costs of housing, property taxes, and daily necessities in major metropolitan areas, leaving little room for enjoyment or financial peace of mind. Relocating to a smaller community offers a powerful strategy to reclaim your budget without sacrificing access to excellent healthcare, vibrant social networks, or cultural amenities. By carefully selecting a retirement destination that balances affordability with robust infrastructure, you secure your financial future while stepping into a slower, more intentional pace of living.

The State of the Retirement Wallet

You already know that every dollar matters when transitioning from a working salary to a fixed income. Inflation continually tests the resilience of middle-income households, transforming previously comfortable budgets into tightly managed spreadsheets. Navigating this economic landscape requires proactive adjustments rather than passive hoping. Recent data from the Survey of Consumer Finances illustrates that a significant portion of older Americans hold the majority of their net worth in home equity rather than liquid retirement accounts. Unlocking that trapped equity by selling a home in an expensive metropolitan area and purchasing a more affordable property in a smaller town represents one of the most effective financial maneuvers available to you. This strategy, known as geographical arbitrage, immediately lowers your monthly overhead while fortifying your cash reserves for future needs.

Evaluating Affordability and Housing

Securing a comfortable retirement begins with aggressively managing your housing expenses. Moving to a smaller town drastically reduces your mortgage or rent obligations, slashes your property tax bills, and lowers your everyday spending on groceries and services. You must analyze both the purchase price of homes and the local tax environment to ensure your new town provides genuine, long-term financial relief.

Winchester, Virginia

Nestled in the beautiful Shenandoah Valley, Winchester provides a charming, historically rich environment at a fraction of the cost of nearby Washington, D.C. You benefit from significantly lower property taxes and a highly accessible housing market that welcomes middle-income budgets. The walkable downtown area reduces your reliance on a vehicle for daily entertainment and dining, keeping your transportation costs manageable. Furthermore, Virginia does not tax Social Security benefits, adding another layer of protection to your monthly cash flow.

Athens, Georgia

Relocating to a vibrant college town like Athens offers immense financial and cultural advantages. Georgia provides incredibly friendly tax policies for retirees, including substantial exemptions on retirement income for residents over the age of sixty-five. You can access world-class lectures, arts, and sporting events through the University of Georgia without paying premium metropolitan prices. The local housing market features diverse, affordable neighborhoods that allow you to downsize comfortably while maintaining a high standard of living.

Bella Vista, Arkansas

Originally designed as a resort community, Bella Vista seamlessly blends affordability with an active outdoor lifestyle. Arkansas maintains a remarkably low cost of living, and the state’s property taxes rank among the lowest in the nation. You stretch your retirement dollars further here while enjoying direct access to numerous lakes, golf courses, and walking trails. This unique environment allows you to maintain peak physical health and social engagement without spending thousands of dollars on expensive country club memberships.

Prioritizing Healthcare and Wellness Access

You cannot compromise on medical access during your retirement years. A low cost of living quickly loses its appeal if you must travel hours to see a specialist or receive emergency care. The smartest relocation strategies focus on towns that host regional medical centers or sit just outside the radius of major urban hospital networks. Evaluating local healthcare infrastructure using tools like Medicare Care Compare ensures you never trade your physical well-being for financial savings.

Traverse City, Michigan

Traverse City stands out as a premier destination for retirees who want robust healthcare access alongside stunning natural beauty. The town is anchored by Munson Medical Center, a highly rated regional hospital system that attracts top-tier specialists to the area. You gain the peace of mind that comprehensive medical care sits right in your backyard. Beyond healthcare, the town offers a gorgeous freshwater coastline, thriving farmers markets, and a deeply engaged community that prioritizes active, healthy aging.

Brevard, North Carolina

Situated in the heart of Transylvania County, Brevard offers a moderate climate and immediate access to pristine national forests. Crucially, it positions you within a short, manageable drive to the advanced medical facilities located in neighboring Asheville. You enjoy the quiet, affordable serenity of a mountain town while maintaining a direct lifeline to specialized healthcare providers. North Carolina also exempts Social Security from state income taxes, helping you keep more of your money to spend on wellness and local recreation.

Fostering Community and Engagement

Financial savings represent only one half of a successful retirement equation; the other half relies on strong social connections. Isolation accelerates cognitive decline and deeply impacts your overall happiness. You need a destination that naturally facilitates friendships through volunteer opportunities, cultural events, and accessible public spaces. According to livability research by AARP, neighborhoods with strong civic engagement metrics consistently produce happier, healthier older adults.

Oxford, Mississippi

Oxford delivers an unparalleled blend of Southern hospitality, literary history, and collegiate energy. Mississippi offers some of the most aggressive tax breaks in the country, entirely exempting all qualified retirement income from state taxes. This financial freedom allows you to fully engage with the vibrant community centered around Ole Miss. You can spend your days attending local art shows, dining in the historic town square, and participating in university-sponsored community education programs alongside fellow active retirees.

Walla Walla, Washington

If you desire a refined lifestyle without the coastal price tag, Walla Walla warrants your immediate attention. Washington levies no state income tax, which dramatically enhances your month-to-month liquidity. The town boasts a world-renowned wine industry, excellent local dining, and a highly engaged, welcoming community. You will find it remarkably easy to build a new social network through local tasting rooms, volunteer organizations, and community festivals that run throughout the mild, distinct four seasons.

Fredericksburg, Texas

Located in the scenic Texas Hill Country, Fredericksburg combines deep German heritage with robust modern amenities. Texas famously collects no state income tax, making it a financial haven for fixed-income households. The town features a thriving Main Street filled with local businesses, ensuring you never run out of places to explore or neighbors to meet. A strong local hospital and numerous community organizations provide both the safety net and the social infrastructure required for a deeply fulfilling retirement.

Real-World Voices on Relocation

Financial planners consistently emphasize that successful geographical arbitrage requires balancing math with emotional readiness. Moving solely for cheaper housing often leads to dissatisfaction if the new town lacks cultural resonance or social infrastructure. Experts from the Consumer Financial Protection Bureau encourage older adults to evaluate housing transitions holistically, considering maintenance burdens, utility costs, and accessibility features alongside the raw purchase price. Savvy retirees who successfully navigate this transition treat the move as a comprehensive lifestyle redesign. They report that shedding the financial anxiety of a high-cost city opens up vast reserves of mental energy, allowing them to focus on hobbies, travel, and family rather than constantly worrying about property tax hikes.

Action Lab: Conducting Your Geographical Arbitrage Audit

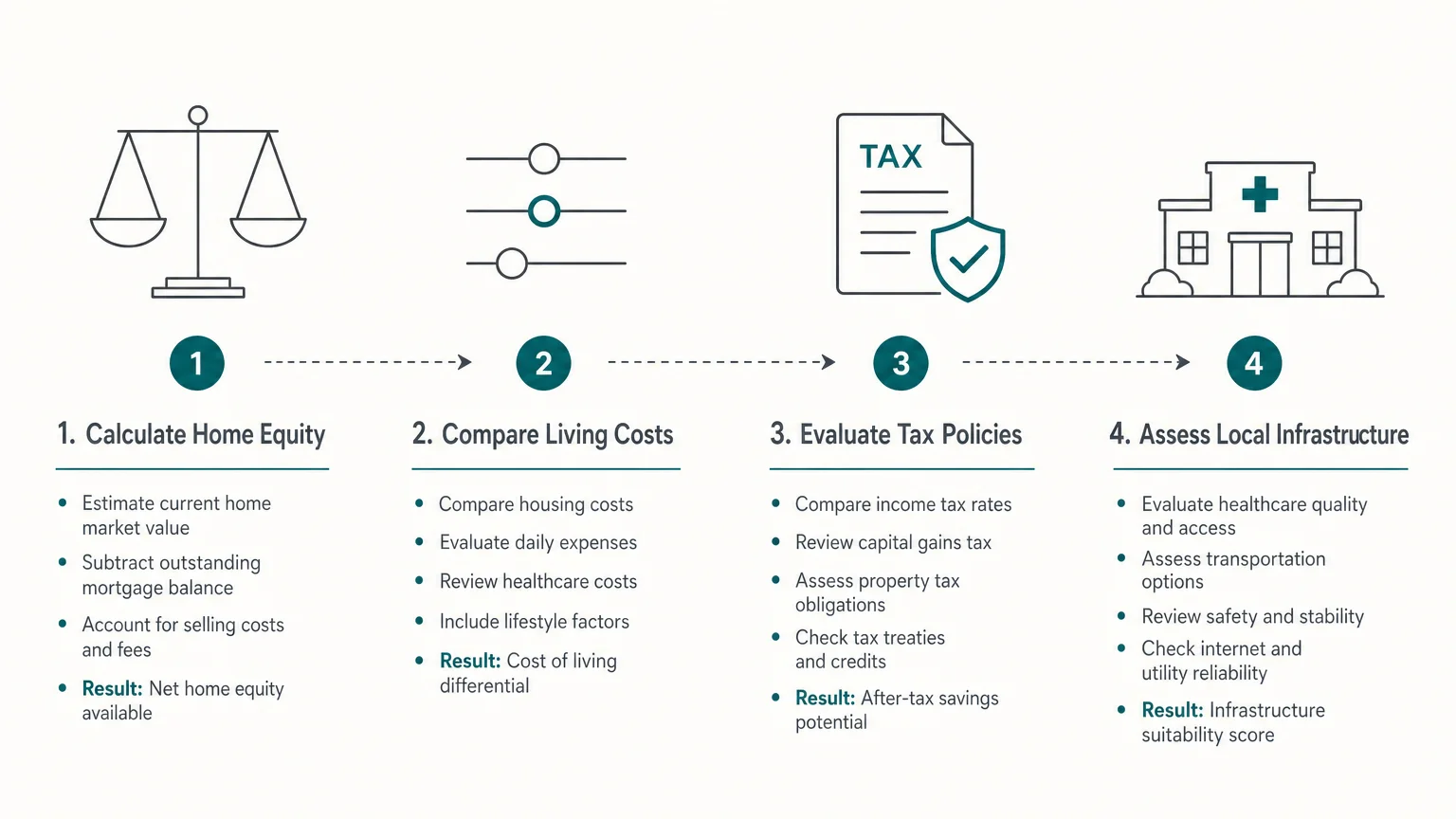

You can test the financial viability of a move right now by conducting a simple spreadsheet audit based on frameworks used by the Bureau of Labor Statistics. First, open a blank document and list your current monthly expenses, focusing heavily on property taxes, home insurance, utility averages, and groceries. Next, research those exact same categories for your target small town using local real estate listings and municipal tax websites. Subtract the projected small-town expenses from your current expenses to reveal your gross monthly savings. Finally, estimate your moving costs and any required home renovations. Divide this transition cost by your monthly savings to determine your break-even timeline. If the move pays for itself in less than three years, you have uncovered a highly viable financial strategy.

Guardrails and Pitfalls to Avoid

Relocating for retirement carries specific risks that demand your careful attention. The most common mistake involves purchasing a home entirely unseen or based solely on a brief weekend vacation. Small towns operate very differently during the off-season, and you must experience the local climate, traffic, and business hours during an ordinary month before committing your capital. You must also guard against hidden local taxes. While a state might not collect income tax, local municipalities often compensate by imposing exorbitant sales taxes or specialized vehicle registration fees. Always audit the entire local tax burden. Finally, accurately measure the distance to a major airport; if you plan to travel frequently or expect family to visit, a remote town three hours from a terminal will quickly become a logistical and financial nightmare.

Frequently Asked Questions

How do state taxes impact my retirement income?

State tax codes vary wildly and directly impact your bottom line. Some states exempt Social Security benefits but heavily tax pension income or withdrawals from your 401k and IRA accounts. You must research how your specific streams of income will be treated in your target state to accurately project your monthly cash flow.

Should I rent or buy when relocating to a new town?

You should almost always rent a home or apartment for six to twelve months before purchasing real estate in an unfamiliar town. Renting protects your capital and gives you the vital time needed to learn which specific neighborhoods offer the best amenities, noise levels, and proximity to grocery stores and medical clinics.

What healthcare factors must I research before moving?

You must verify that the local hospital system accepts your specific Medicare Advantage or supplemental insurance plan. Furthermore, investigate the availability of primary care physicians who are actively accepting new Medicare patients, as many rural areas face severe doctor shortages that can delay your routine care.

How can I test a town before making a permanent move?

Book a short-term rental for at least four weeks during the town’s least appealing season. Use this time to perform daily routines—visit the grocery store, drive to the local hospital, attend a community meeting, and monitor the internet speeds. This practical immersion quickly reveals whether the town aligns with your daily reality.

Seize Your Next Chapter

Taking control of your retirement budget does not require extreme sacrifice; it simply requires strategic placement. You possess the power to radically shift your financial trajectory by choosing a community that respects your savings and enriches your daily life. Pick one town from this guide tonight, spend thirty minutes researching its local housing market, and run a basic comparison against your current expenses. That small, decisive step is the key to unlocking a retirement defined by comfort, community, and lasting peace of mind.