Maximizing your retirement income starts at the supermarket checkout line, where strategic shoppers effortlessly reclaim hundreds of dollars annually through overlooked loyalty benefits. You already know that grocery prices squeeze fixed incomes harder than almost any other budget category; however, tapping into targeted senior savings and optimized store loyalty programs transforms everyday errands into a powerful wealth-retention tool. While typical consumers passively collect generic points, astute retirees actively stack digital coupons, targeted age-based discount days, and fuel rewards to dramatically lower their monthly overhead. By shifting your approach from casual participation to deliberate points management, you can permanently reduce your grocery bill and free up significant cash flow for the activities you actually enjoy.

The State of the Retiree Wallet: Why Every Dollar Matters More Today

Transitioning from your wealth accumulation years into your distribution years completely changes your relationship with daily expenses. When you rely on a fixed pension, Social Security distributions, or a specific safe withdrawal rate from your investment portfolio, volatile prices directly threaten your long-term financial security. You feel the squeeze every time you walk down the grocery aisle, noticing that your favorite household staples cost significantly more than they did just three years ago. This economic pressure forces many middle-income households to make uncomfortable sacrifices, occasionally cutting back on travel, hobbies, or premium health items just to balance the monthly budget.

The data paints a clear picture of this widespread challenge. According to Federal Reserve analyses of household economic well-being, older adults consistently cite everyday inflation as a primary source of financial anxiety. Furthermore, Bureau of Labor Statistics consumer price data reveals that the food-at-home category has historically experienced sharp upward trajectories, heavily impacting consumers who spend a larger percentage of their income on necessities. When your grocery bill jumps by twenty percent, you cannot simply ask your former employer for a raise to cover the difference. You must find creative, structural ways to absorb those costs without draining your hard-earned nest egg.

Fortunately, store loyalty programs offer a highly effective, immediate inflation hedge that most shoppers severely underutilize. Retailers desperately want to retain your business in a highly competitive market, and they willingly exchange substantial discounts, free products, and gasoline rebates for your consistent patronage. Viewing these shopping discounts as an optional bonus is a financial mistake; you should treat optimized loyalty rewards as a mandatory component of your retirement income strategy. Reclaiming five to ten percent of your grocery budget through store loyalty programs is mathematically equivalent to generating a tax-free yield on a substantial cash investment.

Strategy Pillar One: Conducting a Loyalty-Focused Cash-Flow Audit

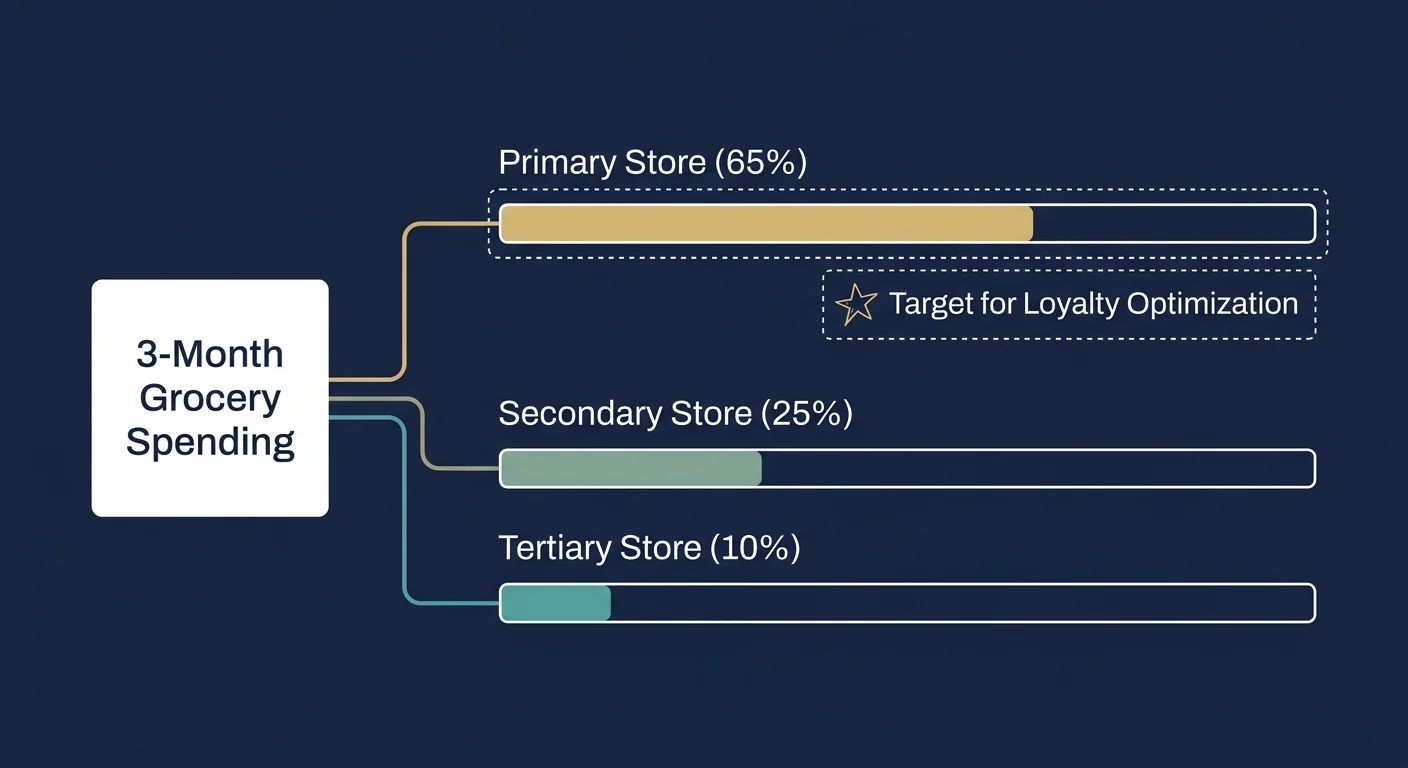

Before you can maximize your senior savings, you must understand exactly where your grocery dollars currently go. You cannot optimize a chaotic system, and many households accidentally dilute their purchasing power by spreading their shopping across too many different retailers. A loyalty-focused cash-flow audit requires you to sit down with your bank statements and credit card bills from the past three months. Your goal is to identify your primary, secondary, and tertiary shopping destinations, calculating the exact amount of money you funnel into each specific corporate ecosystem.

Once you aggregate your spending data, the results often surprise even the most diligent budgeters. You might discover that you spend four hundred dollars a month at a regional supermarket chain, two hundred dollars at a big-box retailer, and another hundred dollars at a neighborhood pharmacy. By dividing your purchases so broadly, you likely fail to hit the highest reward tiers at any single location. Loyalty programs mathematically reward concentration. When you consolidate your purchases into one or two primary ecosystems, you accelerate your point accumulation, unlocking higher-value rewards and targeted promotional offers much faster.

Your audit should also reveal the hidden leakage in your current routine. Leakage occurs when you shop at a secondary store out of sheer convenience and completely forfeit the points you would have earned at your primary store. After identifying your main grocery hub, you must investigate the specific structure of its loyalty program. Look for dedicated senior discount days—many regional grocers offer five to ten percent off your entire cart if you shop on the first Tuesday or Wednesday of the month. Aligning your newly audited grocery budget with these specific calendar days creates an immediate structural drop in your monthly expenses.

Strategy Pillar Two: Automating Your Grocery Rewards and Senior Savings

The era of spending Sunday mornings clipping physical coupons from the newspaper is largely behind us. Modern store loyalty programs run on digital infrastructure, and harnessing this technology is the secret to accessing the deepest shopping discounts. You must transition your strategy to the digital realm by downloading your primary grocery store’s official mobile application and fully completing your digital profile. Retailers route their highest-value digital coupons and personalized senior savings directly through these digital portals, completely bypassing shoppers who only scan a plastic card at the register.

Automation removes the friction from saving money. Most modern grocery applications feature a dedicated section for weekly digital coupons that you can load directly to your account with a single tap. Some advanced platforms even offer an automatic clipping feature, which scans the weekly circular and applies relevant discounts to your loyalty account without requiring manual intervention. You should spend ten minutes every Monday morning opening your preferred store app, reviewing the personalized offers generated by your past purchase history, and digitally clipping every relevant discount to your virtual wallet.

Furthermore, you must link your loyalty account to your preferred payment methods whenever possible. By tying your phone number or digital barcode to a dedicated cash-back credit card, you seamlessly integrate two distinct savings vehicles. When you arrive at the checkout lane, scanning your digital application instantly triggers your loaded manufacturer coupons, applies the store’s weekly promotional pricing, deducts your age-based discount, and earns you fresh loyalty points for your next trip. Automating this entire sequence ensures you never walk away from the register having paid full retail price for a basic necessity.

Strategy Pillar Three: Mindful Spending Through Strategic Stacking

Strategic stacking is the most lucrative tactic in the frugal shopper’s playbook. Stacking simply means combining multiple distinct discount methods on a single transaction to drive the out-of-pocket cost as close to zero as possible. To master this technique, you must deeply understand how your chosen supermarket structures its sales. Most grocery chains start their promotional week on Wednesday, which often overlaps with specialized senior discount days. By shopping on this specific overlap day, you immediately set the foundation for a heavily discounted haul.

Let us walk through the anatomy of a perfect stack. You find a premium brand of laundry detergent on a temporary store promotion, marked down from fifteen dollars to twelve dollars. Through your grocery app, you previously clipped a digital manufacturer coupon worth three dollars off that specific brand. Because you are shopping on the designated senior savings day, the store applies an additional ten percent discount to the sale price. Your final cost drops drastically, and the remaining balance still earns you fuel points toward your next trip to the gas station. This overlapping methodology separates standard shoppers from elite savers.

However, stacking requires intense psychological discipline. You must practice mindful spending, aggressively resisting the urge to buy products simply because they feature an attractive discount. The golden rule of loyalty programs is that a discount on an item you do not actually need offers zero financial benefit; it simply represents money wasted. You can reinforce your mindful spending habits by building a strict weekly meal plan based entirely on the front page of your digital store circular. When your shopping list originates from the weekly digital promotions, your strategic stacking feels effortless and highly intentional.

Real-World Voices: What Behavioral Economists and Financial Planners Tell Us

Financial professionals who specialize in retirement planning consistently emphasize that lowering fixed overhead is far more reliable than attempting to chase higher investment returns. When advising middle-income households on stretching their assets, planners point to grocery optimization as the lowest-hanging fruit in personal finance. Because food costs represent a massive, recurring variable expense, shaving just ten percent off your annual supermarket expenditure yields thousands of dollars in retained capital over a decade. This retained capital continues to compound safely within your retirement accounts, extending the longevity of your portfolio.

Behavioral economists provide fascinating insights into why so many consumers fail to optimize their store loyalty programs. The concept of mental accounting explains that people often view loyalty points as imaginary currency rather than real money. Because points do not sit in a traditional bank account, shoppers frequently let them expire or waste them on frivolous impulse buys. To combat this psychological trap, you must explicitly assign a strict dollar value to your grocery rewards. When you reframe five hundred store points as a tangible ten-dollar bill sitting in your wallet, you suddenly manage those points with the exact same rigor you apply to your checking account.

Advocacy groups actively promote these optimization techniques to protect older adults from economic shocks. Organizations providing Consumer Financial Protection Bureau guidance on managing fixed incomes frequently recommend leveraging corporate discount structures to safely stretch pension checks. The consensus among financial experts is clear: participating in loyalty programs is not a trivial couponing hobby; it is a serious, proven strategy for maintaining your standard of living in the face of relentless consumer inflation.

Action Lab: Calculating Your Real Reward Returns

Theory only benefits you when you apply it to your real-world budget. Let us conduct a practical exercise to demonstrate the raw mathematical power of an optimized loyalty strategy. Imagine you are a retiree who typically spends five hundred dollars a month on groceries, household supplies, and personal care items. Instead of shopping randomly, you decide to execute a fully optimized, single-store strategy at a major regional supermarket that offers a fuel rewards program, digital manufacturer coupons, and a monthly senior discount day.

You strategically schedule your major monthly stock-up trip for the first Tuesday of the month to trigger the store’s ten percent senior citizen discount. Before leaving the house, you open your mobile app and digitally clip twenty dollars’ worth of manufacturer coupons directly aligned with your shopping list. When you hit the register, your five-hundred-dollar cart drops to four hundred and fifty dollars from the age-based discount. Your digital coupons automatically activate, dropping the total further to four hundred and thirty dollars. You just saved seventy dollars at the point of sale with virtually no extra effort.

The calculation does not end there; we must factor in the backend rewards. Your four hundred and thirty dollars of net spending generates four hundred and thirty loyalty points. Under this specific program’s rules, every hundred points equals ten cents off per gallon of gasoline. You redeem your four hundred points to receive forty cents off per gallon on a fifteen-gallon fill-up, saving you an additional six dollars at the pump. Your total monthly savings equal seventy-six dollars. Over a twelve-month period, this simple routine injects more than nine hundred dollars of liquid cash back into your retirement budget—enough to fund a modest vacation, cover an emergency car repair, or pad your emergency savings.

Guardrails and Pitfalls: Avoiding Common Loyalty Program Traps

While the financial upside of store loyalty programs is immense, navigating these corporate ecosystems requires a defensive mindset. The most common trap retirees fall into is loyalty-induced lifestyle creep. Retailers deliberately design their reward structures to incentivize larger basket sizes, often dangling massive bonus point offers if you spend over a certain threshold. You must aggressively protect your budget from these manipulative gamification tactics. Never buy an expensive brand-name product merely to earn bonus points if the generic store brand remains significantly cheaper out of pocket.

You must also pay close attention to reward expiration policies. Supermarkets routinely purge unused points at the end of every calendar month or quarter to reduce their financial liabilities. If you allow your hard-earned grocery rewards to expire, you surrender all the financial leverage you built during your shopping trips. You can easily prevent this catastrophic waste by setting a recurring alert on your digital calendar a few days before the end of the month, reminding you to redeem your points at the fuel pump or convert them into cash discounts at the register.

Finally, approach your digital privacy with a critical eye. Store loyalty programs essentially operate as massive data collection engines; supermarkets happily give you shopping discounts in exchange for tracking your granular purchasing habits. You should regularly review the privacy settings within your mobile grocery applications. Opt out of third-party data sharing whenever the platform allows, and ensure you remain comfortable with the amount of personal information you trade for your senior savings. Maintaining strict privacy boundaries allows you to reap the financial benefits without heavily compromising your personal data.

Frequently Asked Questions About Maximizing Shopping Discounts

Do I need a smartphone to access these savings?

While a smartphone heavily streamlines the process of digitally clipping coupons and tracking your point balances in real-time, it is not strictly mandatory for participation. Many major supermarkets allow you to manage your loyalty account via a standard desktop computer or tablet. You can log into the store’s website from home, load digital offers directly to your account, and simply type your registered phone number into the keypad at the physical register to apply all your synchronized discounts.

How do store credit cards differ from standard loyalty programs?

Standard store loyalty programs are completely free to join, require no credit check, and simply track your purchases to issue rewards. In contrast, store credit cards represent formal debt instruments that involve hard credit inquiries and typically carry exorbitant interest rates. You should generally stick to free loyalty programs paired with a standard, low-interest cash-back credit card, strictly avoiding retail-specific credit lines that threaten to trap you in high-interest consumer debt.

Will joining multiple programs negatively impact my credit score?

Enrolling in free grocery rewards programs has zero impact on your credit score because no financial institution is pulling your credit report or extending you a line of credit. You can safely join a loyalty program at every supermarket, pharmacy, and big-box retailer in your entire region without worrying about hard inquiries appearing on your credit file. These programs simply function as digital membership clubs, not financial lending products.

What should I do if my preferred store lacks a formal rewards structure?

If your primary grocer operates without a loyalty program—a model frequently used by massive warehouse clubs or hard-discount grocers—you must focus entirely on cash-flow audits and mindful spending principles. In these specific scenarios, you can also leverage trusted third-party receipt-scanning applications that offer universal cash rebates regardless of where you purchase your everyday household items. Consistently evaluating unit prices at these discount grocers often replaces the need for a traditional point system entirely.

Your Next Steps Toward Financial Efficiency

Mastering store loyalty programs and age-based shopping discounts does not require you to become an obsessive coupon hoarder; it simply demands a slight adjustment to your existing weekly routines. You already spend a significant portion of your fixed income on household necessities, so you might as well extract the maximum possible value from every transaction. The journey to reclaiming hundreds of dollars a year begins with a single, deliberate action you can take right now.

Choose your primary grocery store today and download its official application to your device. Spend just ten minutes exploring the digital coupon section, familiarizing yourself with the reward tiers, and verifying the specific day of the week they offer targeted senior savings. By aligning your next major shopping trip with these structural discounts, you immediately take back control of your purchasing power. Embrace this pragmatic approach to your grocery budget, and watch as those small, consistent savings quietly transform into substantial financial breathing room for your retirement.