The average retired worker now receives approximately $2,028 per month from Social Security, but that single number will not pay your grocery bill or cover rising utility costs. You likely check your bank account wondering if your benefits are keeping pace with actual expenses. Comparing your check to the national average provides a vital financial baseline, but the real progress happens when you optimize the money you already have. If your monthly deposit feels stretched thin, you need clear strategies to bridge the gap between a fixed income and modern living costs. Here is exactly how your benefits stack up against current national data, alongside actionable tactics to stretch your paycheck without sacrificing your quality of life.

The State of the Wallet: Understanding the National Average

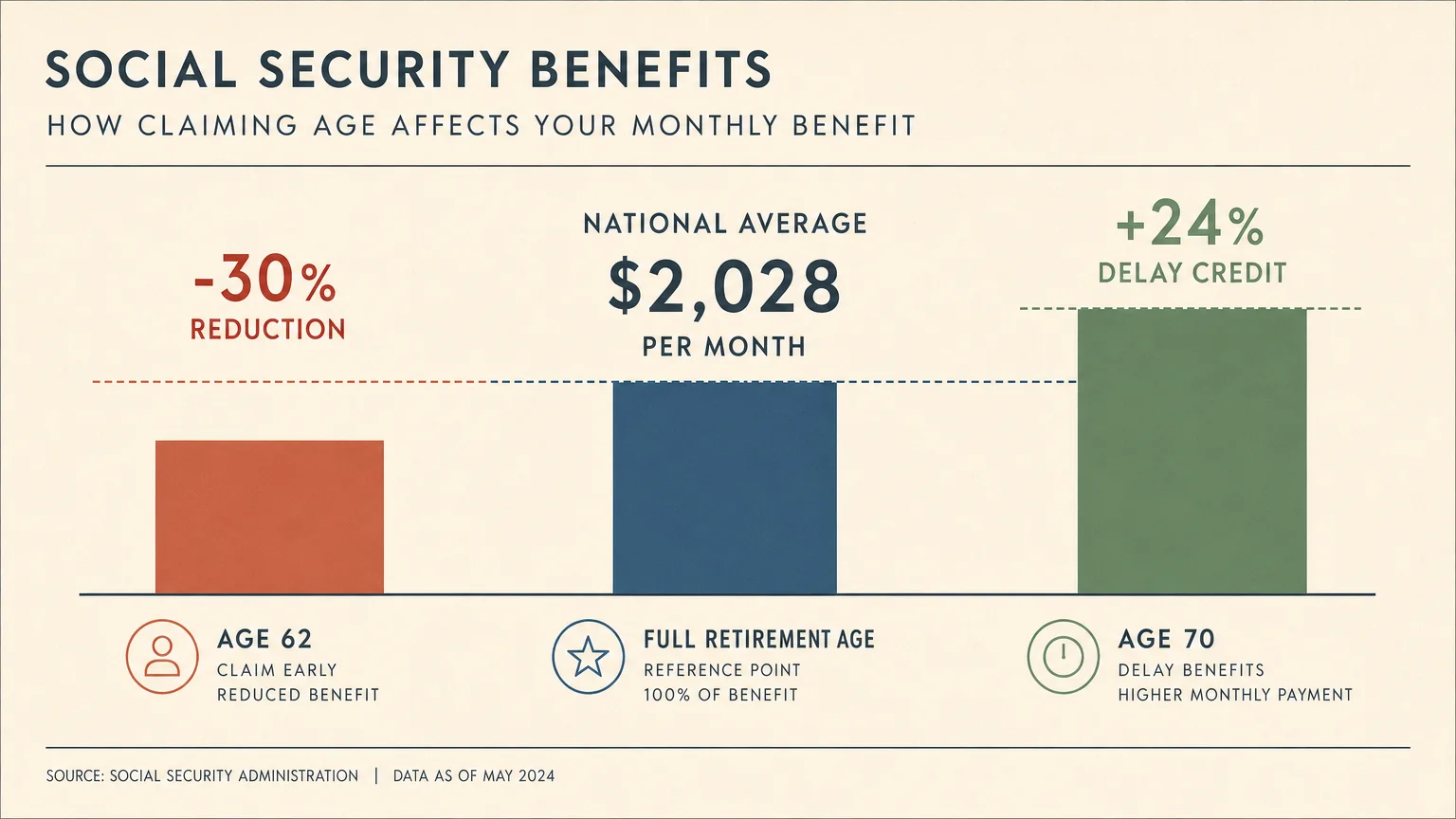

According to the latest data in mid-2026, the average monthly benefit for retired workers hovers right around $2,028. This figure incorporates recent cost-of-living adjustments designed to help your income keep pace with inflation. However, looking at an average can sometimes paint a misleading picture of American retirement; averages are heavily skewed by high earners who maxed out their taxable wage base for thirty-five consecutive years. A more accurate reflection for many middle-income households is the median benefit, which typically sits slightly lower. You might look at your own direct deposit and wonder why it falls short of the two-thousand-dollar mark, but this is perfectly normal and depends entirely on your specific earnings history alongside the exact age you decided to file for your benefits.

The age at which you claim your benefits drastically alters your lifetime payout. Filing at age sixty-two permanently reduces your monthly check by up to thirty percent compared to waiting until your full retirement age. Conversely, delaying your claim until age seventy earns you delayed retirement credits, boosting your payout significantly. When you compare your check to the national average, you must factor in your personal claiming age. If you claimed early to accommodate a health issue or a sudden job loss, your check will naturally sit below the national average. Understanding this mathematical reality removes the emotional sting of comparison and allows you to focus purely on managing the income you actually possess.

Furthermore, the purchasing power of your Social Security check varies wildly depending on your geographic location. Earning two thousand dollars a month goes much further in a rural midwestern town than it does in a coastal metropolitan area. Rising property taxes, varying utility rates, and regional grocery costs all dictate how far your benefits will stretch over thirty days. The core issue is not simply the raw dollar amount printed on your annual statement; the real metric of financial health is how effectively that income covers your specific localized expenses. Acknowledging your unique regional challenges sets the stage for a realistic and highly personalized financial strategy.

Relying entirely on the national average as a benchmark can create a false sense of security for those above it—and unnecessary panic for those below it. The government designed Social Security to replace roughly forty percent of your pre-retirement income, meaning it was never intended to serve as a comprehensive retirement plan. You are essentially operating a business where the revenue is fixed, which means your primary tool for generating breathing room is precise expense management. By shifting your focus away from what others receive and turning your attention toward your own household ledger, you reclaim control over your financial destiny.

Strategy Pillar One: Conducting a Comprehensive Cash-Flow Audit

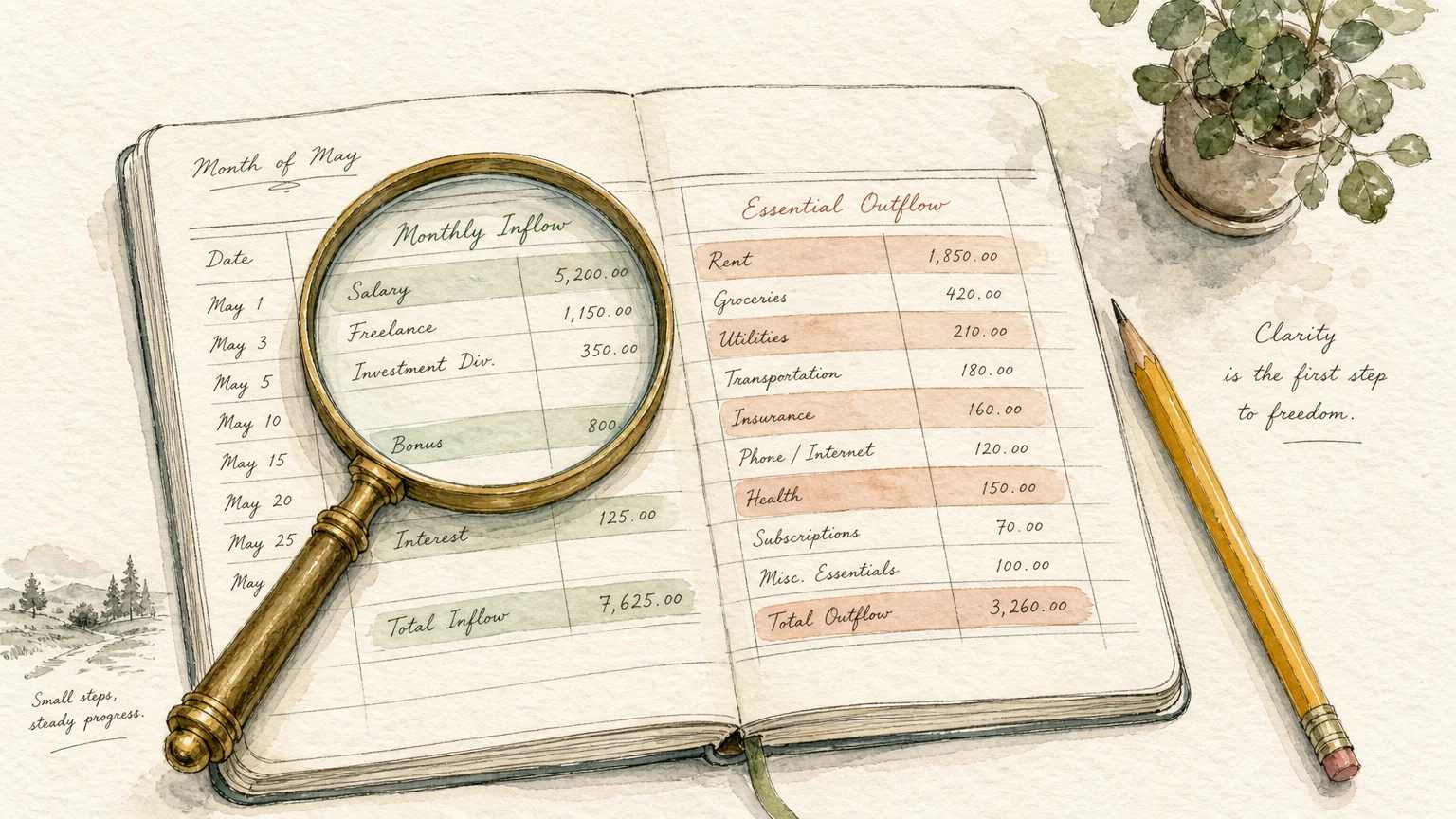

Managing a fixed income requires a surgical understanding of exactly where your money goes every single month. A comprehensive cash-flow audit moves beyond generic budgeting; it forces you to confront your daily financial habits with absolute clarity. Begin by gathering your bank and credit card statements from the past three months. You must examine these documents line by line to identify patterns that quietly drain your resources. Many retirees are shocked to discover how much money disappears into recurring subscription services, unused gym memberships, or premium cable channels they rarely watch. Highlighting these expenses is the first critical step toward reclaiming your hard-earned cash.

Once you have a clear picture of your historical spending, you must separate your absolute necessities from your discretionary choices. Housing, basic utilities, essential groceries, and critical healthcare form your baseline survival number. Everything else—including dining out, streaming services, and hobby expenses—falls into the variable category. By drawing a hard line between needs and wants, you empower yourself to make strategic cuts when inflation pushes your grocery or utility bills higher. You do not have to eliminate every luxury from your life, but you must actively choose which luxuries provide the most joy and eliminate the ones that merely offer convenience.

Adopting a zero-based budgeting approach can revolutionize how you handle your monthly Social Security check. This method requires you to assign a specific job to every single dollar before the month even begins. When your deposit hits your checking account, you immediately allocate funds to your housing, your groceries, your medical bills, and your savings. If there are fifty dollars left over, you proactively assign that money to a designated purpose—perhaps a grandchildren fund or a home maintenance reserve. Leaving unassigned money in your primary checking account is a dangerous temptation; it almost always evaporates into impulsive purchases.

You can leverage free tools and resources to streamline this auditing process. Reviewing guidance from the Consumer Financial Protection Bureau provides excellent frameworks for building a sustainable budget without feeling overwhelmed. If technology feels cumbersome, a simple notebook and pen work just as effectively as the most advanced budgeting software. The goal is not to create a complex accounting system, but rather to establish a reliable routine that keeps you acutely aware of your cash flow. Regular auditing prevents minor financial leaks from turning into catastrophic debt spirals.

Strategy Pillar Two: Implementing Smarter Saving Automations

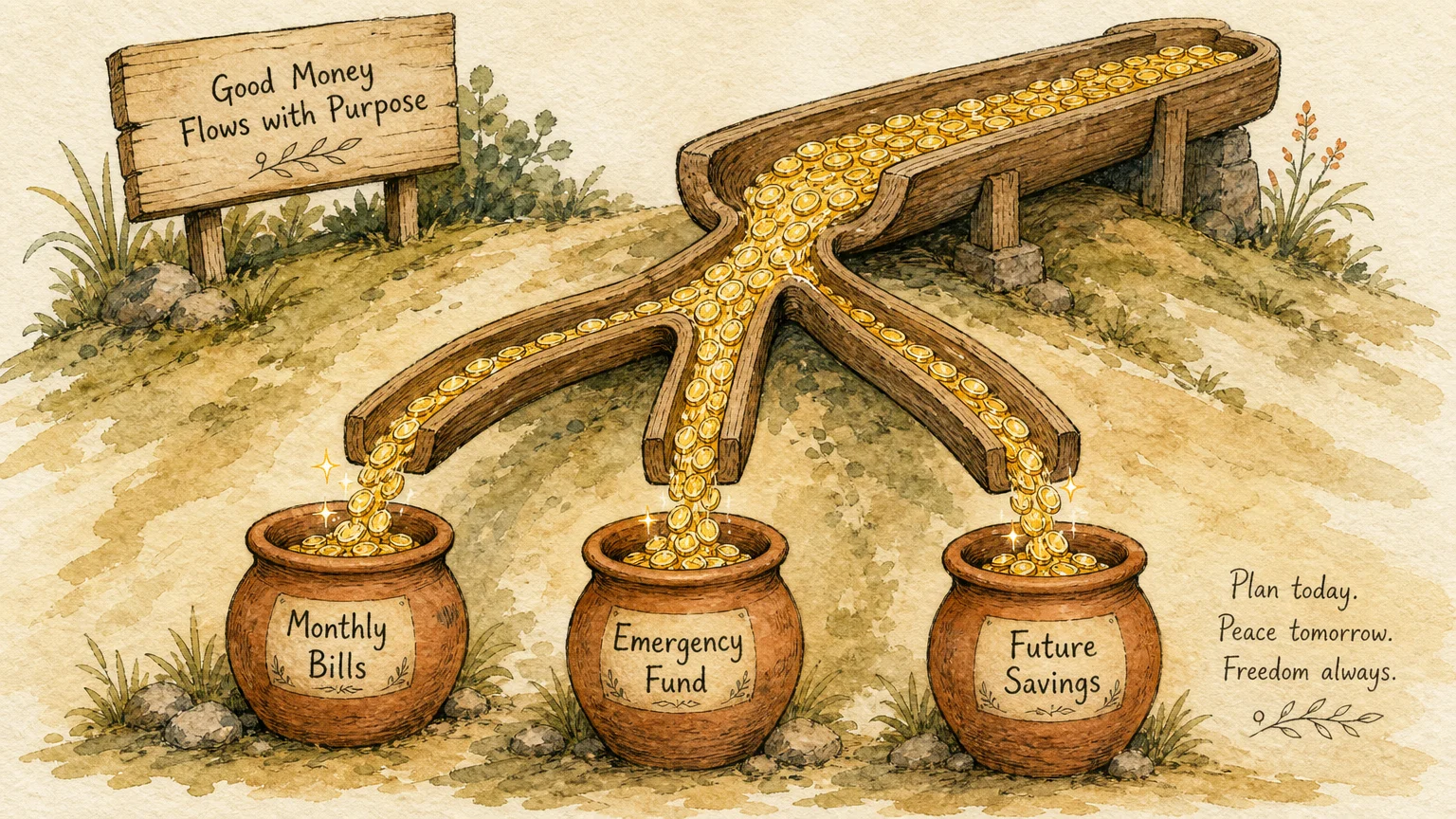

The concept of saving money while living on a fixed income often feels counterintuitive, but it is entirely possible and absolutely necessary. When your Social Security check represents your primary revenue source, a sudden car repair or medical emergency can completely derail your financial stability. Smarter saving automations remove the friction from building your safety net. You must treat your savings contribution exactly like a non-negotiable utility bill. Setting up an automatic transfer on the exact day your Social Security check clears ensures that you pay yourself first, long before discretionary spending tempts you.

You should utilize sinking funds to prepare for inevitable, yet irregular, expenses. A sinking fund is a dedicated savings bucket for a specific future cost. For example, if you know your annual property taxes or homeowners insurance will cost twelve hundred dollars, you automatically route one hundred dollars each month into a separate account. This strategy eliminates the panic of trying to cash-flow a massive bill from a single month of Social Security income. You can create distinct sinking funds for vehicle maintenance, holiday gifts, and medical deductibles. Breaking large obligations into manageable monthly fractions smooths out your cash flow and dramatically reduces financial anxiety.

Where you store your savings matters just as much as the act of saving itself. Traditional brick-and-mortar banks often pay abysmal interest rates that fail to keep pace with inflation. You should strongly consider opening a high-yield savings account through an online institution. These accounts frequently offer interest rates several times higher than conventional banks, turning your emergency fund into an active asset that generates passive income. Every additional dollar earned through interest is a dollar you do not have to pull from your fixed monthly benefits. Just ensure any institution you choose is backed by the Federal Deposit Insurance Corporation for total peace of mind.

Even small automated transfers yield impressive results over time. Routing twenty-five dollars a week into a designated reserve might seem insignificant, but it builds a robust buffer against unexpected financial shocks over the course of a year. Behavioral finance proves that humans adapt quickly to restricted cash flows; if you automate the transfer, you will naturally adjust your spending to accommodate the slightly lower balance in your checking account. This out-of-sight methodology is the single most effective way to build wealth and financial resilience during your retirement years.

Strategy Pillar Three: Mindful Spending and Stretching Your Dollars

Once you have audited your cash flow and automated your savings, your next objective is maximizing the purchasing power of your remaining dollars. Mindful spending requires a proactive approach to your daily transactions. Grocery shopping represents one of the largest variable expenses for retirees, making it a prime target for optimization. Planning your meals around weekly sales flyers, utilizing store loyalty programs, and embracing generic brands can slash your monthly food costs significantly. You must view grocery shopping not as a chore, but as a strategic operation where deliberate choices directly increase your financial margin.

Utility costs and recurring bills are not as fixed as most people assume. You hold significant power as a consumer, and a few polite phone calls can yield substantial monthly savings. Contact your cable or internet provider and ask to speak with the retention department; these representatives possess the authority to offer unadvertised promotional rates to keep your business. Similarly, you should aggressively shop your auto and homeowners insurance rates every single year. Loyalty to a single insurance company rarely pays off; switching providers can often save you hundreds of dollars annually without reducing your coverage levels.

You should never hesitate to leverage your age for financial advantage. Countless retailers, restaurants, and service providers offer senior discounts that they do not actively advertise. Asking a simple question at the checkout counter can instantly reduce your bill by ten to fifteen percent. Over the course of a year, these minor discounts aggregate into meaningful financial relief. Furthermore, investigate community resources designed specifically for retirees on fixed incomes. Many municipalities offer reduced property tax programs, subsidized utility rates, or transportation assistance that can dramatically lower your baseline living expenses.

Healthcare costs frequently threaten the stability of a fixed-income household, but you can navigate these expenses mindfully. Reviewing your Medicare Part D prescription drug plan during the annual open enrollment period ensures you are not overpaying for your medications. Generic drug substitution and mail-order pharmacies often provide the exact same medical efficacy at a fraction of the cost. Additionally, relying on objective data from organizations like the research from the Federal Reserve highlights how proactive medical expense management is a common trait among financially secure retirees. Protecting your health and protecting your wallet are intimately connected endeavors.

Real-World Voices: How Savvy Households Bridge the Gap

Theoretical advice only matters when it works in practice. Financial planners constantly observe how small behavioral shifts separate stressed households from secure ones. The most successful retirees do not necessarily possess the highest Social Security checks; rather, they master the art of intentional living. Consider the approach of adjusting social habits without sacrificing social connection. Instead of meeting friends for expensive dinners, savvy individuals host potluck gatherings or organize morning walks in local parks. These micro-decisions preserve their budget while actually deepening their community ties. It is a brilliant pivot from consumption-based socializing to relationship-based socializing.

Many middle-income households also bridge the financial gap by embracing the sharing economy or monetizing lifelong hobbies. Whether it is selling handmade crafts, offering specialized consulting based on decades of career experience, or occasionally renting out a spare room, the modern economy offers flexible ways to supplement a fixed income. Even generating an additional two hundred dollars a month completely transforms a tight budget. By listening to the success stories of your peers, you quickly realize that retirement does not mean the end of your economic productivity; it simply marks a transition into more enjoyable and self-directed forms of income generation.

Action Lab: Your Tonight-Tweak Calculation

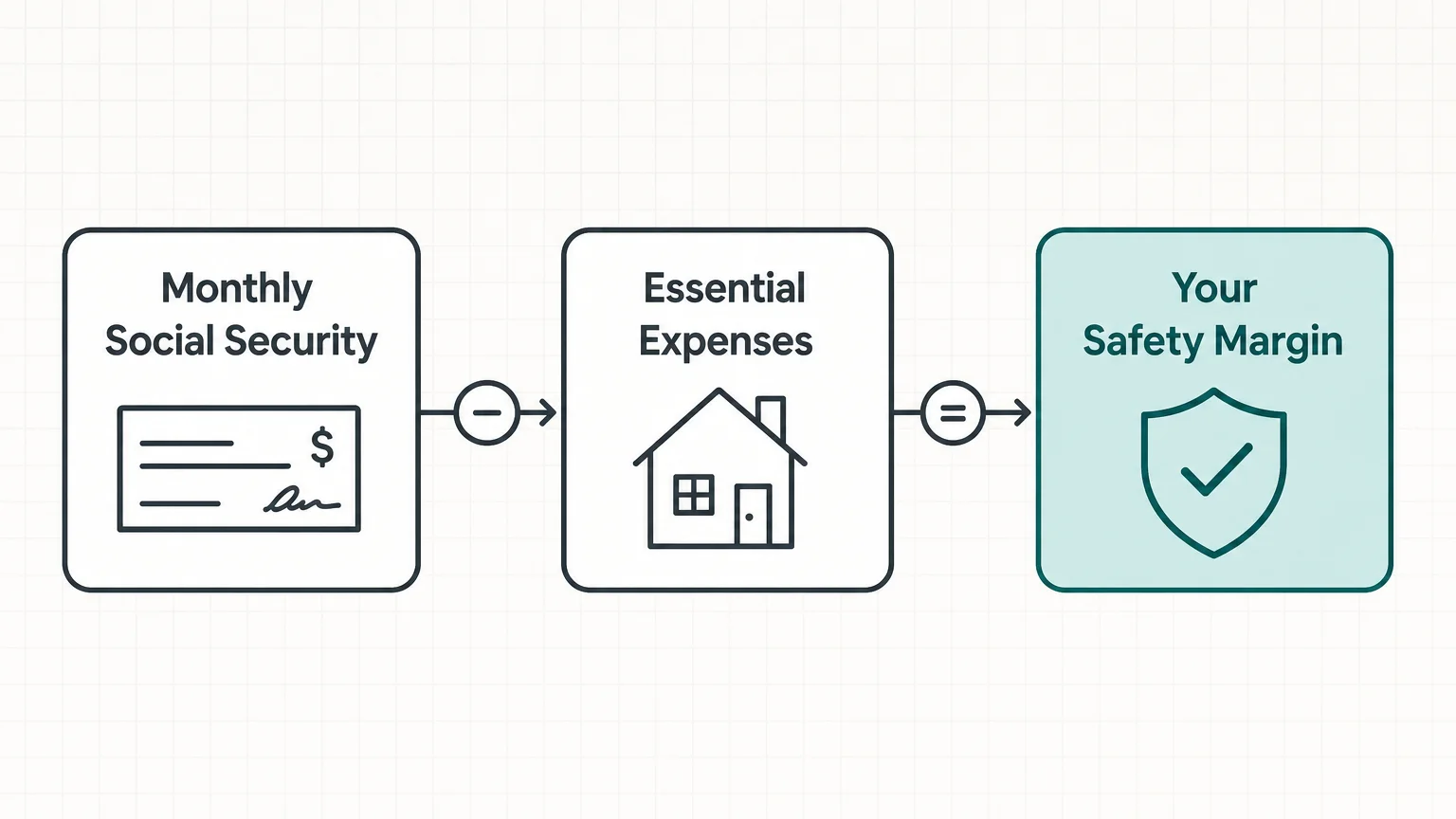

Reading about financial strategies is helpful, but immediate action generates tangible results. Tonight, you are going to perform a simple calculation to uncover your exact financial margin—the space between your guaranteed income and your survival expenses. First, write down the exact dollar amount of your monthly Social Security check and any other guaranteed pension income. Next, list your bare-bones survival expenses. This category exclusively includes housing, essential groceries, basic utilities, and vital medications. Finally, subtract your total survival expenses from your guaranteed income. The resulting number is your personal gap metric.

If your calculation yields a positive number, you have breathing room. Your immediate task is to divide that remaining money between your automated savings goals and your discretionary spending. If the number is negative, you are currently relying on credit cards or draining your savings to survive. In this scenario, you must immediately implement the auditing and mindful spending tactics discussed earlier to lower your survival baseline. Do not let a negative result paralyze you; treat it as a clinical diagnosis that requires a specific, actionable treatment plan. Clarity is the absolute best antidote to financial anxiety.

Guardrails and Pitfalls: What to Avoid on a Fixed Income

Navigating life on a fixed income requires you to remain vigilant against common financial traps. The most dangerous pitfall is relying on credit cards to bridge monthly deficits. When you carry a balance on a high-interest credit card, you are essentially borrowing against your future Social Security checks. The compound interest quickly outpaces any cost-of-living adjustments you might receive, locking you into a cycle of permanent debt. If you cannot afford a discretionary purchase with cash, you simply cannot afford it. Protecting your fixed income means fiercely defending yourself against consumer debt.

You must also beware of predatory financial products marketed specifically to seniors. Payday loans, high-fee reverse mortgages, and overly complex annuities often promise quick relief but deliver long-term devastation. Always consult with a fiduciary financial advisor or a trusted family member before signing any contract that leverages your home equity or requires a substantial upfront fee. Finally, never drain your emergency savings to help adult children with their own financial struggles. You cannot secure a loan for your retirement, whereas younger generations have ample time to recover from financial setbacks. Securing your own oxygen mask first is the ultimate act of financial responsibility.

Frequently Asked Questions

Does the national average include spousal and survivor benefits?

When you read about the national average Social Security check, you must pay attention to the specific category being cited. The figure of roughly two thousand dollars per month typically refers exclusively to retired workers. Spousal benefits and survivor benefits represent entirely different statistical categories, which are calculated using different formulas. A spousal benefit generally maxes out at fifty percent of the primary earner’s full retirement age amount, meaning the average check for spouses is significantly lower than the average for primary workers.

Will working a part-time job reduce my Social Security payments?

If you have not yet reached your full retirement age, earning income above a specific annual limit will temporarily reduce your Social Security benefits. The official data from the Social Security Administration dictates exact earnings limits each year, and the administration withholds a portion of your benefits if you exceed that threshold. However, this money is not lost forever; your benefit amount is recalculated upward once you reach full retirement age. Once you surpass your full retirement age, you can earn an unlimited amount of money without facing any reductions to your monthly check.

How can I estimate my future cost-of-living adjustments?

The Social Security Administration determines the annual cost-of-living adjustment by tracking the Consumer Price Index for Urban Wage Earners and Clerical Workers during the third quarter of the year. While you cannot predict the exact percentage in advance, monitoring general inflation trends provides a strong hint. When the cost of groceries and gasoline rises sharply throughout the summer, you can reasonably expect a higher adjustment the following year. Conversely, during periods of economic stability and low inflation, the annual increase will naturally be much smaller.

Are my Social Security benefits subject to federal income taxes?

Many retirees are surprised to learn that the federal government taxes Social Security benefits if your combined income exceeds certain thresholds. Your combined income is calculated by adding your adjusted gross income, any nontaxable interest, and half of your Social Security benefits. If this total surpasses the base amount set by the IRS, up to eighty-five percent of your benefits may be taxable. Working closely with a tax professional ensures you are not caught off guard by an unexpected tax bill when filing your annual return.

Moving Forward With Confidence

Comparing your financial reality to a national statistic provides context, but your daily actions ultimately dictate your financial comfort. You possess the power to shape your retirement experience through intentional budgeting, strategic savings, and relentless expense optimization. You do not need a massive income to achieve peace of mind; you simply need a plan that aligns your available resources with your core priorities. Start small this week. Cancel one unused subscription, automate a twenty-dollar transfer into a high-yield savings account, and negotiate a single recurring bill. These micro-victories build the momentum necessary to permanently transform your financial trajectory. Your Social Security check is the steady foundation of your retirement, and with focused effort, you can build a resilient and joyful life upon it. Keep stepping forward, keep questioning your expenses, and watch your financial confidence grow.