Timing your major purchases can save you thousands of dollars each year and dramatically extend the life of your fixed income. When you leave the daily workforce, every dollar in your pension or portfolio must stretch further, making strategic buying habits an essential tool for your long-term financial security. You no longer have the luxury of out-earning impulsive spending, but you possess a powerful new asset: total control over your schedule. Because you can shop on a random Tuesday morning or delay replacing a refrigerator until the seasonal sales cycle peaks, you hold significant leverage over retailers. By mastering the retail calendar and understanding exactly when consumer demand dips, you can consistently secure premium goods at steep discounts.

State of the Wallet: Why Timing Matters More Than Ever

In recent years, unpredictable inflation has forced middle-income households to rethink their relationship with everyday money management. For retirees, this dynamic is particularly pronounced and requires immediate adaptation. A fixed monthly income does not automatically adjust to absorb the rising costs of raw materials, global manufacturing, and supply chain shipping. This harsh reality transforms casual shopping into a highly strategic endeavor. You are no longer just buying a washing machine or upgrading a mattress; you are allocating a carefully preserved, finite resource. When you pay full retail price for a major necessity, you lose out on months of potential compound interest that those funds could have generated in a high-yield savings account.

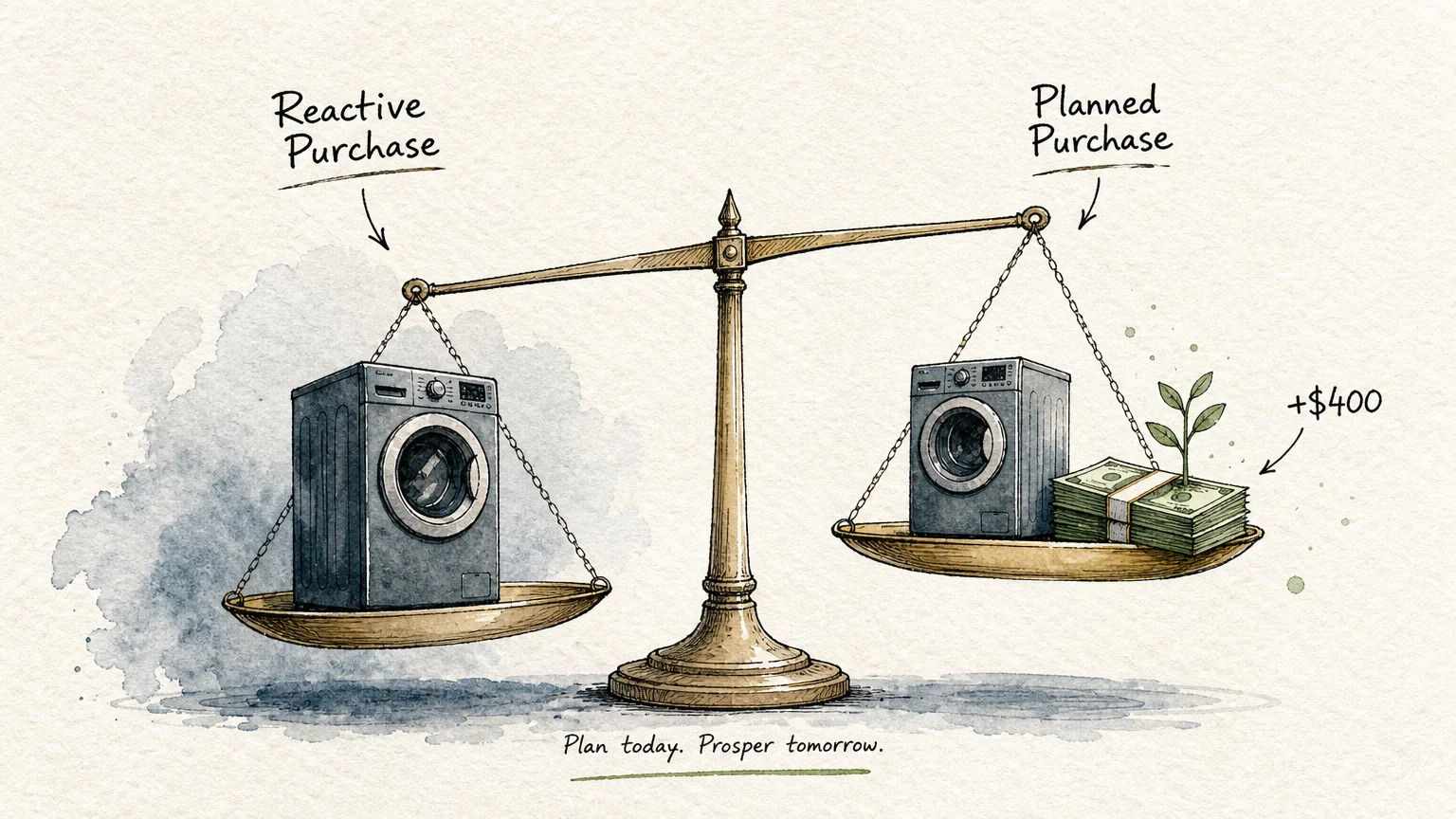

Monitoring the Federal Reserve annual reports on household economic well-being reveals a powerful insight: families who anticipate and meticulously plan for major expenses experience significantly less financial anxiety than those who purchase reactively. By saving twenty percent on a two-thousand-dollar household appliance simply by waiting for the right month, you effectively earn four hundred dollars completely tax-free. When you aggregate these strategically timed savings across appliances, electronics, and vehicles over a decade of retirement, you create a powerful, silent income stream that actively fortifies your long-term financial security.

Strategy Pillars: The Science of Seasonal Buying

Pillar One: Mastering the Appliance and Furniture Cycles

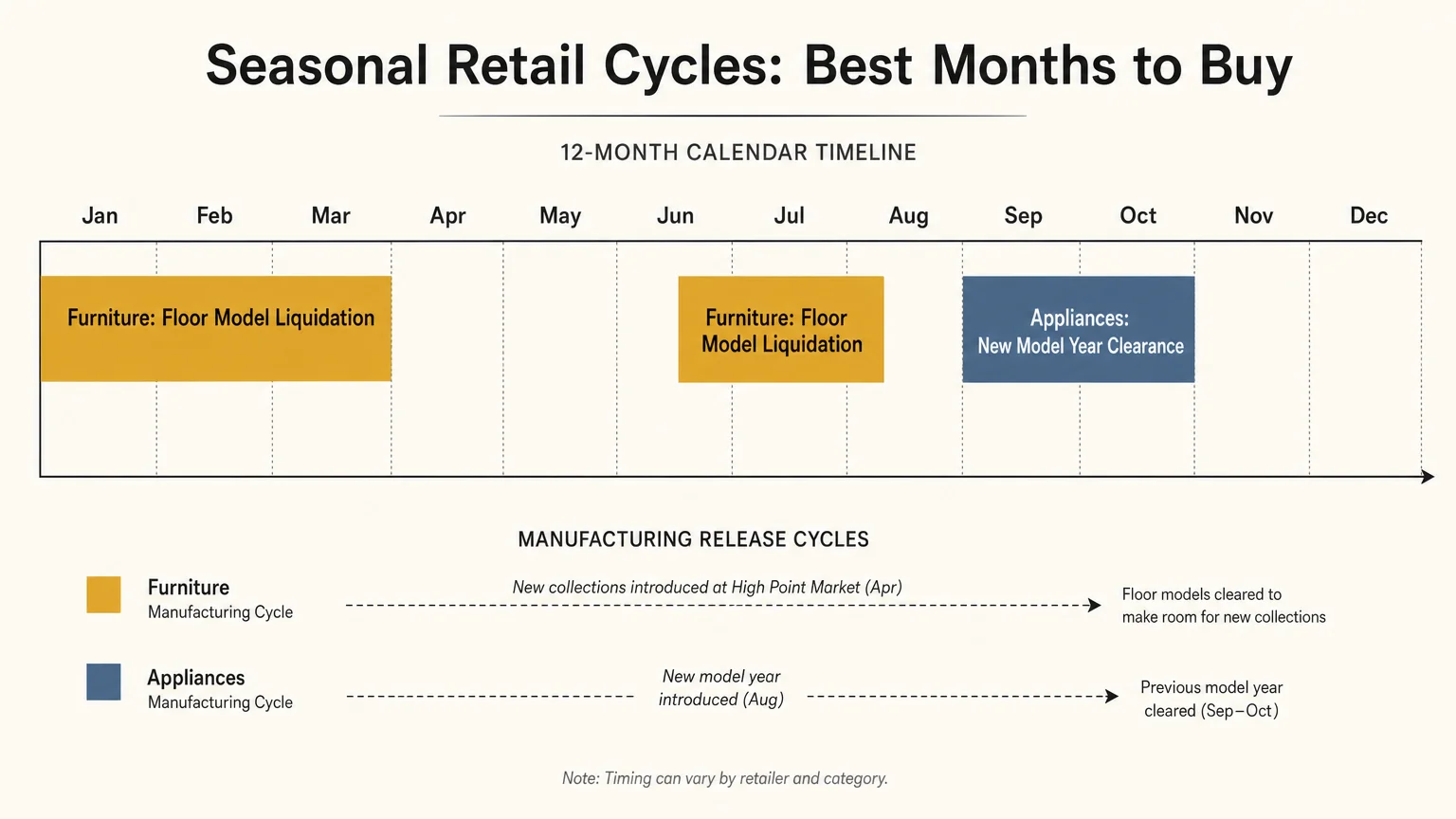

When you set out to replace a major household appliance, understanding the manufacturing calendar provides a distinct advantage over the average consumer. Most major appliance manufacturers roll out their latest models in the early fall, specifically throughout September and October. In preparation for this influx of new inventory, big-box retailers face immense pressure to clear out the previous year’s models. They simply do not have the warehouse capacity or the showroom floor space to hold both generations of products simultaneously. This logistical bottleneck is your primary opportunity to strike. You can frequently secure steep discounts on high-end washing machines, dryers, and ranges simply because the retailer desperately needs the square footage. The older models are typically identical in core functionality to the new releases, allowing you to keep perfectly good capital in your bank account while upgrading your home with premium machinery.

The indoor furniture market follows a reliable biannual rhythm that you can easily track and exploit for massive savings. New furniture designs and collections debut at industry trade shows in the spring and fall, meaning retail stores receive their new inventory shipments in February and August. Consequently, January and July stand out as the absolute best months to purchase new sofas, dining sets, and ergonomic bedroom furniture. Store managers are highly motivated to liquidate their existing floor models during these two transitional months. As a retiree, you possess a distinct advantage when negotiating for these floor models; you can walk into a furniture showroom on a quiet Thursday morning, engage directly with a sales manager who is eager to hit their mid-week metrics, and respectfully offer to take a floor model off their hands for a substantial discount.

Pillar Two: Optimizing Big-Ticket Electronics and Tech

Electronics and home entertainment systems represent another significant drain on a fixed income if purchased at the wrong time of year. Television prices follow a uniquely predictable trajectory centered around major sporting events. If you want to upgrade your living room display to something larger or clearer for aging eyes, late January and early February offer the most aggressive pricing of the year. Retailers slash prices on large-screen televisions in the weeks immediately preceding the Super Bowl to capture the attention of sports fans. Conversely, personal computers and laptops operate on an entirely different timeline dictated by the academic calendar. Even though your school days are behind you, the back-to-school rush in August is your best friend when it comes to upgrading digital devices. Manufacturers flood the market with competitive pricing designed to attract college students, allowing you to secure a fast, reliable laptop for managing your investment portfolio at a fraction of the usual cost.

Digital cameras, smart home devices, and audio equipment see their most significant price reductions during the Black Friday and Cyber Monday shopping extravaganzas in late November. However, navigating these events requires ironclad discipline and a strict adherence to your established budget. Retailers often manufacture derivative models specifically for Black Friday—devices that look identical to premium models but feature cheaper internal components designed to hit a low promotional price point. To avoid this trap, you must identify the exact model number of the premium device you want in October. When the November sales arrive, verify that the discounted item matches your target model number character for character, guaranteeing a genuine discount on high-quality hardware.

Pillar Three: Timing the Automotive Market

Purchasing a reliable vehicle is perhaps the most intimidating transaction you will face in retirement, but the automotive industry operates on strict dealer quotas that you can easily use to your advantage. Dealerships function on monthly, quarterly, and annual sales targets. If you walk onto a dealership lot on the final days of the month—especially if that day falls at the end of a fiscal quarter or the end of December—you will encounter a sales team highly motivated to negotiate. The manufacturer frequently offers the dealership substantial financial bonuses for hitting specific volume targets. A salesperson might be willing to sell you a vehicle at or even slightly below their invoice cost simply because your transaction triggers a lucrative volume bonus for the entire dealership network.

Even if you have the liquid cash available to purchase a vehicle outright, understanding the nuances of automotive financing can still work to your benefit. Familiarizing yourself with Consumer Financial Protection Bureau guidelines on automotive financing allows you to evaluate promotional loan offers accurately and spot predatory terms. Occasionally, automakers will offer zero-percent or incredibly low-interest financing to move stale inventory before the next model year arrives. By accepting this promotional financing, you can keep your lump sum of cash invested in a certificate of deposit, allowing your money to generate guaranteed interest while you pay off the depreciating asset with effectively free money.

Real-World Voices: What Financial Experts Recommend

Financial experts universally agree that the transition from accumulating wealth during your working years to systematically spending it in retirement represents one of the most significant psychological hurdles you will face. You spend four decades meticulously saving every spare dollar, investing wisely, and delaying gratification. Suddenly, the paychecks stop, and you must comfortably release those accumulated funds to maintain your home and lifestyle. This fundamental shift in financial mechanics often leads to extreme behavior; some retirees adopt a level of severe frugality that diminishes their hard-earned quality of life, while others engage in impulsive panic-buying when an old item finally breaks down because they lack a structured replacement plan.

Behavioral economists and certified financial planners suggest that building a forward-looking calendar for major expenditures actively neutralizes this spending anxiety. When you decide in March that you will replace your aging sedan in December, you give yourself nine months of psychological runway to accept the upcoming outflow of cash. You also create a generous window to monitor prices and wait for the most advantageous seasonal transition. Recent data from major banking institutions analyzing fixed-income budgeting highlights that retirees who implement structured, forward-looking purchasing calendars report significantly lower levels of financial stress compared to their peers who shop reactively.

Action Lab: A Month-by-Month Purchasing Strategy

To truly understand the power of strategic timing, let us walk through a practical scenario detailing how a proactive retiree manages multiple major purchases without jeopardizing their cash flow. Imagine you have evaluated your household needs and determined that over the next twelve months, you must replace your failing dishwasher, upgrade your uncomfortable primary mattress, and purchase a reliable used vehicle. If you simply walked into retail stores and dealerships tomorrow to purchase all three items simultaneously, you would pay premium sticker prices, drain a massive chunk of your liquid reserves at once, and likely experience a severe bout of buyer’s remorse. Instead, you audit your current liquid assets and place the total projected budget for all three items into a dedicated high-yield savings account to gather interest while you wait for the retail calendar to work in your favor.

In January, you execute the first phase of your plan by targeting the retail industry’s famous white sales, securing a fantastic deal on a high-quality mattress and negotiating free delivery. You wait until the late spring to address the kitchen appliance, visiting a home improvement center on a Wednesday morning during the Memorial Day sales events to secure a heavily marked-down dishwasher. Finally, you exercise profound patience and wait until the final week of December to purchase the vehicle, visiting a dealership that is desperate to hit their annual volume bonuses. By spreading these purchases out and targeting specific retail windows, you drastically reduce your total expenditure, utilize the interest earned throughout the year to cover peripheral fees, and fiercely protect your financial peace of mind.

Guardrails & Pitfalls: Mistakes to Avoid on Fixed Incomes

While strategic timing provides immense financial leverage, the retail environment is still fraught with psychological traps designed to separate you from your retirement savings. The most common pitfall retirees face is the illusion of the good deal. Retailers spend billions of dollars on marketing designed to create a false sense of urgency. If you purchase a heavily discounted appliance or electronic device that you do not actually need simply because it is fifty percent off, you have not saved fifty percent; you have wasted one hundred percent of the money spent. You must ruthlessly separate your actual household requirements from the artificial desires manufactured by flashy clearance signs and limited-time email promotions.

You must also remain vigilant against predatory financing schemes disguised as helpful payment plans. Furniture and appliance retailers frequently advertise zero-percent interest promotions to entice buyers who might be hesitant to part with a large lump sum of cash. While these deferred interest promotions can be useful if managed perfectly, they contain highly punitive clauses. Paying close attention to Consumer Financial Protection Bureau warnings on deferred interest promotions will help you understand that if you miss a single payment by one day, or fail to pay off the entire balance before the promotional period ends, the retailer will retroactively apply exorbitant interest charges dating back to the original purchase date. If you cannot afford to pay cash for the item today, a deferred interest plan is a risk you cannot afford to take.

Frequently Asked Questions

Question: Do senior discounts stack with holiday promotional sales?

In most commercial retail environments, businesses implement strict policies against stacking multiple discounts on a single transaction. If an appliance is already marked down forty percent for a Labor Day clearance event, the store register will typically reject any additional percentage off from a senior discount program. However, you should always politely ask the store manager if they can honor both. Even if they cannot reduce the sticker price further, a savvy manager will often throw in peripheral benefits—such as free hauling of your old appliance, waived installation fees, or upgraded delivery options—to keep your business while staying within the confines of their corporate policy.

Question: Should I use my retirement savings for a sudden major expense?

Tapping directly into a tax-advantaged account like a traditional IRA or 401(k) for an unbudgeted major purchase can trigger severe and unintended financial consequences. Every dollar you withdraw from a traditional retirement account is taxed as ordinary income, meaning a sudden ten-thousand-dollar withdrawal for a new roof could potentially push you into a higher tax bracket and negatively impact your Medicare premiums for the year. Whenever possible, you should fund major purchases from a standard, easily accessible liquid savings account to avoid these tax complications.

Question: Is Black Friday actually the best time for big household appliances?

While Black Friday benefits from aggressive marketing campaigns and flashy doorbuster advertisements, the actual savings on major household appliances are frequently outmatched by earlier autumn clearance events. Because manufacturers roll out new large appliance models in September and October, the deepest clearance markdowns on premium goods happen long before Thanksgiving. The items heavily promoted on Black Friday are often derivative models specifically manufactured with cheaper components for the holiday rush. If you are shopping for a durable washing machine or a refrigerator, your time is much better spent scouring home improvement stores in early autumn.

Question: How do I negotiate when the price is already marked down?

When an item hits the clearance floor, the retailer has typically reached the absolute floor of their pricing power for the physical product. At this stage, your negotiation strategy must shift from the sticker price to the costly peripheral services associated with the purchase. You can confidently approach the floor manager and offer to buy the clearance item immediately if they agree to waive the hefty delivery and installation fees, which often run into the hundreds of dollars. Additionally, you can ask for bundled accessories at no extra cost, ensuring you extract the maximum possible value from the transaction.

Your Next Strategic Move

Mastering the retail calendar transforms the way you interact with the modern consumer economy. You no longer have to view replacing a failing appliance or an aging vehicle as an unavoidable financial disaster; instead, these moments become opportunities to exercise your leverage and maximize the value of your hard-earned retirement funds. The time flexibility you have earned over decades of hard work is now one of your most valuable financial assets. Use it unapologetically to sidestep the frantic weekend crowds, bypass the artificial urgency of flashy marketing campaigns, and secure the premium goods you deserve at prices that genuinely respect your fixed income.

Tonight, take thirty minutes to walk through your home and genuinely assess the health of your major assets. Check the age of your water heater, evaluate the tread on your vehicle’s tires, and listen to the hum of your refrigerator. Write down any item that will likely need replacement within the next two years, and map those items to their respective optimal purchasing months. By building this proactive calendar today, you insulate your savings from sudden shocks and ensure that your money continues to work exactly as hard as you did to earn it.